PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755285

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755285

Mobile Robots Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

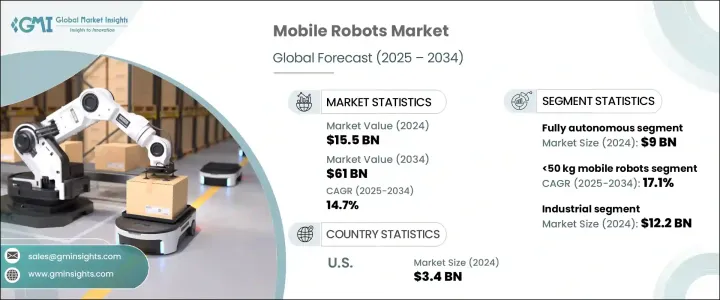

The Global Mobile Robots Market was valued at USD 15.5 billion in 2024 and is estimated to grow at a CAGR of 14.7% to reach USD 61 billion by 2034, driven by the global shortage of skilled labor, especially in manufacturing and logistics. This shortage encourages businesses to adopt robotic solutions for handling repetitive tasks, order fulfillment, and material handling. The imposition of tariffs on robotic components during the Trump administration led to a spike in manufacturing costs for U.S. companies, which slowed the adoption of autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) in small and medium-sized enterprises (SMEs).

As a result, manufacturers diversified their supply chains, shifted production to other regions, and restored manufacturing activities. In the long run, these strategies helped strengthen supply chain resilience by establishing regional hubs to mitigate trade risks. The adoption of mobile robots is further bolstered by rising minimum wages in developed economies, justifying the return on investment for robotic solutions. Industries like e-commerce, which experience seasonal demand surges, rely on mobile robots for scalability, a trend seen particularly in aging societies like Japan and Germany, where the labor gap is a growing concern.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.5 Billion |

| Forecast Value | $61 Billion |

| CAGR | 14.7% |

The fully autonomous mobile robot segment was valued at USD 9 billion in 2024 and remains a dominant segment. These robots, which leverage AI and machine learning, can make real-time decisions without human input, making them ideal for dynamic environments like warehouses and hospitals. They navigate complex spaces using advanced sensors and SLAM (Simultaneous Localization and Mapping) technology. The rise of fully automated facilities, known as lights-out warehouses, accelerated the adoption of AMRs, particularly in Asia-Pacific and North America. However, challenges remain in applications requiring human-like dexterity, driving investments in advanced technologies like computer vision and adaptive grippers.

The mobile robots market with a payload capacity of 50-500 kg segment was valued at USD 7.4 billion in 2024, reflecting their widespread application in various industries. These robots are essential for material handling in warehouses, facilitating the transport of heavy components in manufacturing environments, and moving large equipment in hospitals. The versatility of these robots in handling mid-range payloads makes them a critical link between lightweight robots used for smaller tasks and heavy-duty robots designed for more industrial-scale operations. As automation continues to expand in industrial sectors, this category of mobile robots is playing an increasingly vital role in streamlining operations and improving efficiency.

United States Mobile Robot Market reached USD 3.4 billion in 2024, driven by a combination of labor shortages, rising minimum wages, and growing interest in automation technologies across sectors such as logistics, healthcare, and retail. With high labor costs and an increasing need for operational efficiency, industries use mobile robots to optimize their supply chain and material handling processes. The U.S. market has also benefited from government initiatives and policies that foster innovation in robotics, helping companies improve productivity and reduce reliance on human labor.

Some leading players in the Global Mobile Robots Industry include KUKA AG, ABB, Hikrobot Co., Ltd., Teradyne Inc., and Geek+. To strengthen their market position, companies in the mobile robots industry are focusing on several strategies. One key approach is expanding their product portfolio by integrating cutting-edge technologies such as AI, machine learning, and advanced sensors into their robotic solutions. Companies are also increasingly localizing their manufacturing operations to mitigate trade risks and reduce reliance on international supply chains. Additionally, many partners with industry leaders in logistics, e-commerce, and manufacturing to tailor their robots to specific industry needs. Investment in R&D is another essential strategy, enabling companies to stay ahead of the curve with innovations in autonomous navigation, dexterity, and human-robot interaction.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Labor shortages and rising workforce costs

- 3.3.1.2 E-commerce growth and warehouse automation

- 3.3.1.3 Advancements in AI and sensor technologies

- 3.3.1.4 Regulatory support and industry 4.0 initiatives

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High initial investment costs

- 3.3.2.2 Lack of skilled operators

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Automation Level, 2021 - 2034 (USD Billion & Thousand Units)

- 5.1 Key trends

- 5.2 Fully autonomous

- 5.3 Semi-autonomous

- 5.4 Manual (remotely operated vehicle)

Chapter 6 Market Estimates & Forecast, By Payload Capacity, 2021 - 2034 (USD Billion & Thousand Units)

- 6.1 Key trends

- 6.2 <50 kg

- 6.3 50–500 kg

- 6.4 500–1000 kg

- 6.5 >1000 kg

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion & Thousand Units)

- 7.1 Key trends

- 7.2 Residential/domestic

- 7.3 Commercial places

- 7.4 Industrial

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 KUKA AG

- 9.3 Boston Dynamics

- 9.4 OMRON Corporation

- 9.5 Yaskawa America, Inc.

- 9.6 Universal Robots A/S

- 9.7 Seiko Epson Corporation

- 9.8 FANUC America Corporation

- 9.9 Teradyne Inc.

- 9.10 Geek+

- 9.11 Hikrobot Co., Ltd.

- 9.12 Locus Robotics

- 9.13 Ocado Group plc.

- 9.14 Rockwell Automation, Inc.

- 9.15 Vecna Robotics

- 9.16 Agility Robotics