PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755375

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755375

Hip Replacement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

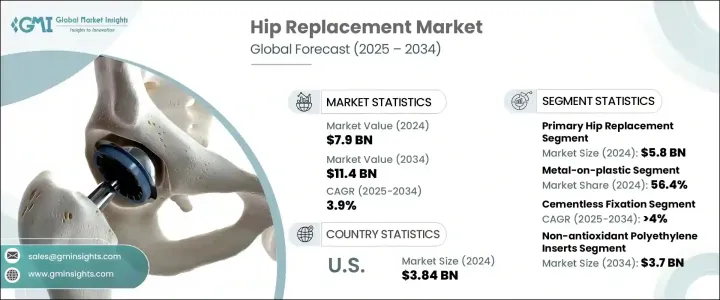

The Global Hip Replacement Market was valued at USD 7.9 billion in 2024 and is estimated to grow at a CAGR of 3.9% to reach USD 11.4 billion by 2034. The market is experiencing growth due to a combination of technological innovation, increased surgical volume, and rising incidences of joint-related disorders. A growing elderly population, particularly those affected by degenerative joint diseases, continues to be a primary demographic undergoing hip replacement procedures. Moreover, the integration of robotics and minimally invasive surgical methods has significantly enhanced clinical outcomes. These advancements have led to shorter hospital stays, reduced recovery periods, and improved patient satisfaction, ultimately contributing to a higher adoption rate of hip replacement procedures globally.

Implant surgeries are increasingly common among older adults experiencing progressive joint deterioration. These procedures are more successful and widely accepted today, thanks to ongoing developments in surgical techniques and materials. In addition, improved healthcare infrastructure and better patient education regarding treatment outcomes have supported market expansion. The rising number of trauma cases and orthopedic injuries, along with favorable healthcare reimbursement, has also boosted the frequency of hip replacement surgeries. Innovations in implant design, compatibility, and durability further enable orthopedic surgeons to deliver effective, patient-specific solutions. The market continues to evolve with the increasing demand for enhanced mobility solutions and long-term performance among active aging populations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.9 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 3.9% |

In terms of product segmentation, primary hip replacement devices dominated the global market in 2024, with a recorded value of USD 5.8 billion. These devices remain the most commonly used implants due to their broad application across various surgical procedures. Their widespread use is attributed to their compatibility with multiple hip disorders and their ability to provide reliable, long-term results. An increasing number of hip implant procedures-driven by factors such as bone fractures and aging-related joint wear-has ensured continued growth for this product category.

Based on material type, metal-on-plastic implants led the market with a 56.4% share in 2024. This material combination remains a preferred choice due to its excellent wear resistance, affordability, and mechanical stability. The metal component effectively absorbs pressure, while the plastic liner reduces joint friction, leading to improved mobility and reduced wear over time. These implants are commonly used worldwide due to their effectiveness, surgeon familiarity, and lower revision rates, making them a go-to choice for both healthcare professionals and patients.

When analyzed by fixation method, cementless fixation systems emerged as the leading category in 2024 and are forecasted to grow at a CAGR of 4% through 2034. This segment has gained traction due to the long-term biological stability it offers. Unlike cemented fixation, which relies on synthetic adhesives, cementless implants promote natural bone growth around the implant surface. This biological integration offers increased longevity and reduces the chances of implant loosening over time. Younger patients, in particular, benefit from this fixation method due to its higher success rate over extended periods. Improved surface designs and material coatings have further driven demand for this approach, especially in minimally invasive and outpatient surgical settings.

The inserts segment of the market is also experiencing notable trends. Non-antioxidant polyethylene inserts are gaining attention and are projected to reach USD 3.7 billion by 2034. These inserts are known to reduce oxidative wear, which helps enhance implant longevity-a vital consideration for more active and younger individuals. Their growing usage is supported by their reliable clinical performance, broader availability, and simplified manufacturing processes. Healthcare professionals favor these inserts due to consistent procedural success and strong historical data supporting their long-term effectiveness.

Among end-use categories, hospitals and clinics held the dominant revenue share in 2024 and are anticipated to witness substantial growth over the coming years. These facilities are equipped to handle complex orthopedic surgeries, including hip replacements, and offer integrated care that spans pre-surgical consultation through post-surgical rehabilitation. They also benefit from increased access to advanced surgical technologies, including robotic assistance and imaging systems, which enhance procedural accuracy. The rising number of minimally invasive surgeries performed in these clinical environments further supports market growth.

North America accounted for 50.6% of the global market share in 2024, largely due to the presence of well-established healthcare infrastructure and a growing elderly population. Within the region, the United States registered a market value of USD 3.84 billion in 2024. Higher rates of osteoporosis, arthritis, and obesity are increasing the demand for hip replacement procedures. Public awareness campaigns and improved access to surgical options have also contributed to rising procedure volumes.

Industry players continue to enhance their product lines by investing in next-generation implants and digital technologies. Strategic collaborations and technological innovations, including 3D-printed implants and robotic surgical systems, are helping manufacturers stay competitive and better serve evolving patient needs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Forecast model

- 1.6 Primary research and validation

- 1.6.1 Primary sources

- 1.7 Forecast model

- 1.8 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Fixation material

- 2.2.5 Inserts

- 2.2.6 End use

- 2.3 CXO Perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in number of trauma cases

- 3.2.1.2 Increasing prevalence of hip arthritis and osteoporosis

- 3.2.1.3 Recent technological advancements

- 3.2.1.4 Growing demand for personalized hip implants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with implants and surgery

- 3.2.2.2 Stringent regulatory guidelines

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.8.1 Impact of reimbursement policies on market growth

- 3.9 Patent landscape

- 3.10 Pipeline analysis

- 3.11 Consumer behaviour analysis

- 3.12 Number of hip replacement procedures for key countries

- 3.13 Hip replacement treatment scenario

- 3.14 Porter's analysis

- 3.15 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.2.5 Latin America

- 4.2.6 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Primary hip replacement devices

- 5.3 Partial hip replacement devices

- 5.4 Revision hip replacement devices

- 5.5 Hip resurfacing devices

Chapter 6 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn and Units)

- 6.1 Key trends

- 6.2 Metal-on-plastic

- 6.3 Ceramic-on-metal

- 6.4 Ceramic-on-plastic

- 6.5 Ceramic-on-ceramic

Chapter 7 Market Estimates and Forecast, By Fixation Material, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Cementless fixation

- 7.3 Hybrid fixation

- 7.4 Cemented fixation

Chapter 8 Market Estimates and Forecast, By Inserts, 2021 - 2034 ($ Mn and Units)

- 8.1 Key trends

- 8.2 Non-antioxidant polyethylene inserts

- 8.3 Cross-linked polyethylene inserts

- 8.4 Antioxidant polyethylene inserts

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospitals and clinics

- 9.3 Ambulatory surgical centers

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn and Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 B Braun

- 11.2 CONFIRMIS

- 11.3 Corin

- 11.4 DePuy Synthes (Johnson & Johnson)

- 11.5 enovis

- 11.6 ExaTech Inc

- 11.7 KyOCERA

- 11.8 Link

- 11.9 Medacta International

- 11.10 MicroPort Orthopedics

- 11.11 ORTHO DEVELOPMENT

- 11.12 Smith+Nephew

- 11.13 stryker

- 11.14 ZIMMER BIOMET