PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755382

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1755382

Insulated Concrete Form (ICF) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

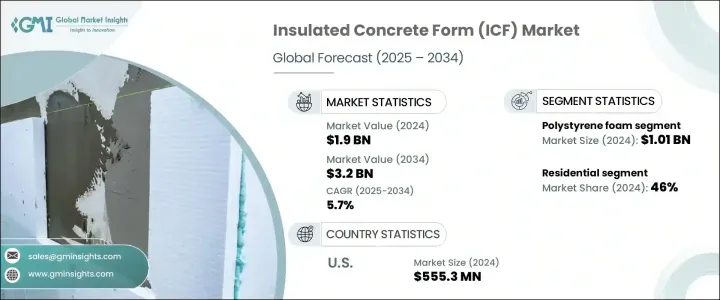

The Global Insulated Concrete Form Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 3.2 billion by 2034. This momentum is largely attributed to the increasing pace of urbanization and the growing demand for durable, energy-efficient residential and commercial structures. As cities expand and infrastructure projects scale up to meet rising population needs, the construction sector is prioritizing solutions that offer better energy efficiency, soundproofing, and sustainability. Insulated concrete forms are gaining recognition across various regions due to their high performance in thermal insulation and structural strength.

Governments and regulatory bodies are playing a crucial role by promoting energy-saving construction practices. These initiatives are encouraging developers and contractors to switch to advanced building techniques that support long-term energy savings and environmental responsibility. Global energy policies are progressively pushing for near-zero energy buildings, driving a notable shift toward modern construction materials like ICFs. The surge in eco-consciousness, especially among homeowners and developers, is leading to increased adoption of ICF systems, which are considered superior alternatives to conventional building methods. The push for sustainable building codes, stricter energy regulations, and green certification programs continues to fuel the widespread acceptance of ICF-based construction.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 5.7% |

In terms of material, the polystyrene foam segment led the market with a revenue of approximately USD 1.01 billion in 2024 and is projected to expand at a CAGR of 6.3% over the forecast period. The growth of this segment stems from its excellent thermal insulation properties and cost-effectiveness. Its lightweight and durable nature makes it highly manageable on construction sites, reducing both time and labor expenses. The flexibility to shape and cut these materials during on-site construction activities adds to their growing preference. Polystyrene foam products are aligned with modern building standards that emphasize sustainability, thermal performance, and ease of application. This compatibility makes them ideal for a broad range of construction projects, from small-scale homes to large institutional and commercial developments. Their adaptability across different structural systems and concrete applications ensures consistent demand over the forecast timeline.

Application-wise, the residential segment emerged as the frontrunner in 2024, accounting for 46% of the total market revenue, and is anticipated to register a CAGR of over 6% through 2034. The residential sector continues to favor ICF systems due to their soundproofing capabilities, energy efficiency, and resilience in extreme weather conditions. As energy costs rise and consumers become more aware of the benefits of sustainable living, there is a significant push toward adopting green construction practices in home building. This trend is amplified by policy-level support that incentivizes sustainable housing solutions. Builders are recognizing the long-term value offered by ICFs, particularly in regions with fluctuating or harsh climates. The growing interest in eco-friendly housing solutions and the increasing implementation of stringent energy codes are expected to keep residential construction as the dominant application area for ICFs over the coming years.

Regionally, the United States led the North American market with an estimated valuation of USD 555.3 million in 2024 and is set to witness a CAGR of 6% between 2025 and 2034. The market expansion is driven by a combination of advanced building practices, high energy-efficiency standards, and rising investments in both residential and commercial construction. The demand for buildings that meet or exceed modern energy performance expectations is intensifying, prompting developers to adopt ICFs at a growing rate. The country's diverse climate zones also play a significant role in this trend, as they necessitate high-performance insulation systems to reduce energy consumption throughout the year. The growing number of energy-conscious consumers, combined with the push for certifications that reward sustainable construction practices, has cemented ICFs as a key material in U.S. building projects.

Key players contributing to the global insulated concrete form market include BecoWallform, Amvic, Buildblock Building System, Fox Blocks, Foam Holdings, Liteform Technologies, Nexcem, Neopar, PFB Corporation, Quad-Lock Building Systems, Polysteel Warmer Wall, Rastra Holding, Standard ICF, and Superform Products. These companies are actively engaged in strategic partnerships, product innovation, and regional expansions to strengthen their market positions and cater to the growing global demand for insulated concrete forms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast parameters

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.1.7 Retailers

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Trade impact

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (Cost to customers)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook & future considerations

- 3.2.1 Trade impact

- 3.3 Impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Urbanization and infrastructure development

- 3.3.1.2 Government initiatives promoting energy efficiency

- 3.3.1.3 Increasing demand for disaster-resistant structures

- 3.3.2 Industry pitfalls & challenges

- 3.3.2.1 Higher initial costs compared to traditional materials

- 3.3.2.2 Limited awareness and skilled workforce

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Pricing analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.1.1 Industry structure and concentration

- 4.1.2 Competitive intensity assessment

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.3.1 Product positioning

- 4.3.2 Price-performance positioning

- 4.3.3 Geographic presence

- 4.3.4 Innovation capabilities

- 4.4 Strategic dashboard

- 4.4.1 Competitive benchmarking

- 4.4.1.1 Manufacturing capabilities

- 4.4.1.2 Product portfolio strength

- 4.4.1.3 Distribution network

- 4.4.1.4 R&D investments

- 4.4.2 Strategic initiatives assessment

- 4.4.3 SWOT analysis of key players

- 4.4.1 Competitive benchmarking

- 4.5 Future competitive outlook

Chapter 5 Market Estimates & Forecast, By Material, 2021 – 2034, (USD Million) (Thousand Per Sq foot)

- 5.1 Key trends

- 5.2 Polystyrene foam

- 5.3 Polyurethane foam

- 5.4 Cement-bonded wood fiber

- 5.5 Cement-bonded polystyrene beads

- 5.6 Cellular concrete

Chapter 6 Market Estimates & Forecast, By Application, 2021 – 2034, (USD Million) (Thousand Per Sq foot)

- 6.1 Key trends

- 6.2 Commercial

- 6.3 Industrial

- 6.4 Infrastructure

- 6.5 Residential

Chapter 7 Market Estimates & Forecast, By Region, 2021 – 2034, (USD Million) (Thousand Per Sq foot)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.4.6 Indonesia

- 7.4.7 Malaysia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 South Africa

Chapter 8 Company Profiles

- 8.1 Amvic

- 8.2 BecoWallform

- 8.3 Buildblock Building System

- 8.4 Foam Holdings

- 8.5 Fox Blocks

- 8.6 Liteform Technologies

- 8.7 Logix Brands Ltd.

- 8.8 Neopar

- 8.9 Nexcem

- 8.10 PFB Corporation

- 8.11 Polysteel Warmer Wall

- 8.12 Quad-Lock Building Systems

- 8.13 Rastra Holding

- 8.14 Standard ICF

- 8.15 Superform Products