PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773370

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773370

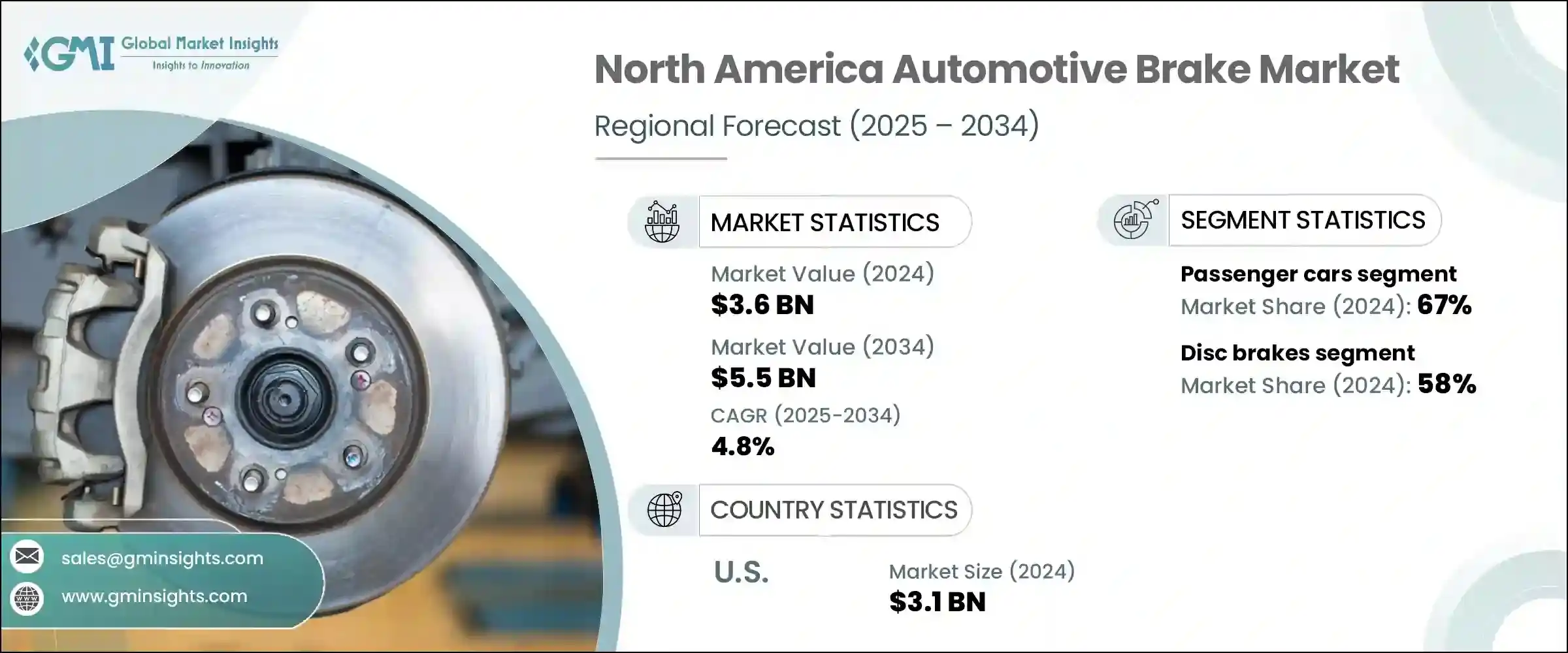

North America Automotive Brake Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

North America Automotive Brake Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 5.5 billion by 2034. This growth is being driven by increasing commercial vehicle production, expansion of logistics fleets due to e-commerce, rising deployment of ADAS and autonomous technologies, and continuous innovation in brake system design. The region is witnessing a rapid transformation in its automotive brake sector, shaped by evolving mobility needs and tighter safety regulations. As the demand for advanced braking technologies grows, manufacturers are prioritizing performance, safety, and durability.

Developments in vehicle connectivity and automation are accelerating the shift toward intelligent braking solutions, while OEMs are aligning product strategies with the changing infrastructure and safety landscape. With freight activity on the rise and a high volume of private vehicle ownership, especially in suburban regions, North America remains a critical market for high-precision, low-maintenance braking systems. The industry's progress is further supported by a strong regulatory push for safer vehicles, encouraging the adoption of integrated electronic and regenerative braking solutions. These trends collectively position the automotive brake industry in North America on a trajectory of sustained and diversified expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $5.5 Billion |

| CAGR | 4.8% |

With the continued rise of long-haul transportation and expanding freight routes, modern commercial vehicles now require braking systems that go far beyond basic mechanical performance. Heavy-duty trucks and trailers are expected to perform under varied loads and long distances, which has led to increased adoption of advanced air disc brakes. These brakes offer superior heat management, quicker actuation, and lower maintenance cycles, making them ideal for demanding logistics operations. Their efficiency in high-frequency and cross-border transit is helping optimize fleet reliability. As uptime and safety become strategic advantages in freight movement, manufacturers are concentrating on innovative systems tailored to modern logistics frameworks.

The passenger car segment led the market in 2024, accounting for 67% share, and is projected to grow at a CAGR of 5.6% through 2034. Consistent demand for sedans, SUVs, and crossovers has reinforced the dominance of this segment. Private vehicle ownership in suburban and growing metro areas remains high, which has created consistent demand for responsive, durable braking systems. Automotive manufacturers are advancing brake technologies with features such as regenerative braking, ABS, and ESC to meet rising consumer expectations for safety, comfort, and personalized vehicle performance. These brake systems are increasingly being engineered for smarter functionality and better ride experience.

The disc brakes segment held the top position in 2024, capturing 58% share, and is projected to grow at 5.8% CAGR from 2025 to 2034. Their popularity is driven by superior stopping ability, thermal efficiency, and dependability in various weather and road environments. These systems have become the go-to choice for manufacturers looking to provide optimal braking performance in personal and commercial vehicles alike. Their synergy with advanced driver assistance systems enhances both vehicle safety and driver confidence, further solidifying their role in modern braking architecture.

U.S. Automotive Brake Market held an 85% share and generated USD 3.1 billion in 2024. The country's dominance is supported by an extensive vehicle base, widespread use of technologically advanced brakes, and strong enforcement of safety regulations. U.S. is at the forefront of brake innovation, driven by consistent investments from OEMs and Tier 1 suppliers. These investments have resulted in systems that combine mechanical reliability with advanced digital integration. Brake solutions in the U.S. now include electronic control systems, predictive diagnostics, and features aligned with connected vehicle ecosystems.

Key companies shaping the North America Automotive Brake Market include Robert Bosch, Continental, Aisin Corporation, Woco Industrietechnik, Brembo, Denso Corporation, Valeo, MAHLE, Rochling Group, and Akebono Brake Industry. Leading players in the North American brake market are focused on expanding product portfolios with smart and sustainable braking solutions. These companies are investing in R&D to develop systems compatible with electric, hybrid, and autonomous vehicles, emphasizing lightweight construction and digital integration.

Strategic collaborations with OEMs help ensure early access to new vehicle platforms and long-term supply partnerships. In addition, manufacturers are enhancing their regional production capabilities and supply chains to meet just-in-time delivery standards. Many are incorporating predictive maintenance features and sensor-based monitoring into brake systems, aligning with the shift toward connected and data-driven automotive ecosystems.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Brake

- 2.2.4 Component

- 2.2.5 Technology

- 2.2.6 Propulsion

- 2.2.7 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising commercial vehicle production

- 3.2.1.2 Fleet expansion in e-commerce logistics

- 3.2.1.3 Growth in autonomous and ADAS-enabled vehicles

- 3.2.1.4 Technological advancements in automotive brake

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High R&D and integration costs

- 3.2.2.2 Competition from low-cost imports

- 3.2.3 Market opportunities

- 3.2.3.1 Increased penetration of EVs and hybrids

- 3.2.3.2 Remanufacturing and circular economy models

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By Brake, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Disc brakes

- 6.3 Drum brakes

Chapter 7 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Brake calipers

- 7.3 Brake pads/shoes

- 7.4 Brake rotors/discs

- 7.5 Brake drums

- 7.6 Master cylinder

- 7.7 Brake lines & hoses

- 7.8 Brake boosters

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Hydraulic braking system

- 8.3 Electromechanical braking system

- 8.4 Pneumatic braking system

Chapter 9 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 Electric

- 9.3.1 PHEV

- 9.3.2 HEV

- 9.3.3 FCEV

- 9.3.4 BEV

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 OEMs

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 11.1 Key trends

- 11.2 U.S.

- 11.2.1 Alabama

- 11.2.2 Alaska

- 11.2.3 Arizona

- 11.2.4 Arkansas

- 11.2.5 California

- 11.2.6 Colorado

- 11.2.7 Connecticut

- 11.2.8 Delaware

- 11.2.9 Florida

- 11.2.10 Georgia

- 11.2.11 Hawaii

- 11.2.12 Idaho

- 11.2.13 Illinois

- 11.2.14 Indiana

- 11.2.15 Iowa

- 11.2.16 Kansas

- 11.2.17 Kentucky

- 11.2.18 Louisiana

- 11.2.19 Maine

- 11.2.20 Maryland

- 11.2.21 Massachusetts

- 11.2.22 Michigan

- 11.2.23 Minnesota

- 11.2.24 Mississippi

- 11.2.25 Missouri

- 11.2.26 Montana

- 11.2.27 Nebraska

- 11.2.28 Nevada

- 11.2.29 New Hampshire

- 11.2.30 New Jersey

- 11.2.31 New Mexico

- 11.2.32 New York

- 11.2.33 North Carolina

- 11.2.34 North Dakota

- 11.2.35 Ohio

- 11.2.36 Oklahoma

- 11.2.37 Oregon

- 11.2.38 Pennsylvania

- 11.2.39 Rhode Island

- 11.2.40 South Carolina

- 11.2.41 South Dakota

- 11.2.42 Tennessee

- 11.2.43 Texas

- 11.2.44 Utah

- 11.2.45 Vermont

- 11.2.46 Virginia

- 11.2.47 Washington

- 11.2.48 West Virginia

- 11.2.49 Wisconsin

- 11.2.50 Wyoming

- 11.3 Canada

- 11.3.1 Alberta

- 11.3.2 British Columbia

- 11.3.3 Manitoba

- 11.3.4 New Brunswick

- 11.3.5 Newfoundland and Labrador

- 11.3.6 Nova Scotia

- 11.3.7 Ontario

- 11.3.8 Prince Edward Island

- 11.3.9 Quebec

- 11.3.10 Saskatchewan

- 11.3.11 Northwest Territories

- 11.3.12 Nunavut

- 11.3.13 Yukon

Chapter 12 Company Profiles

- 12.1 Aisin Corporation

- 12.2 Akebono Brake Industry

- 12.3 Autoliv

- 12.4 BorgWarner

- 12.5 Brembo

- 12.6 Continental

- 12.7 Denso Corporation

- 12.8 Federal-Mogul / Tenneco

- 12.9 Haldex AB

- 12.10 Hitachi Astemo

- 12.11 Knorr-Bremse

- 12.12 MAHLE

- 12.13 Mando Corporation

- 12.14 Nissin Kogyo

- 12.15 Robert Bosch

- 12.16 Rochling Group

- 12.17 Valeo

- 12.18 Wabco

- 12.19 Woco Industrietechnik

- 12.20 ZF Friedrichshafen