PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773458

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1773458

RF Test Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

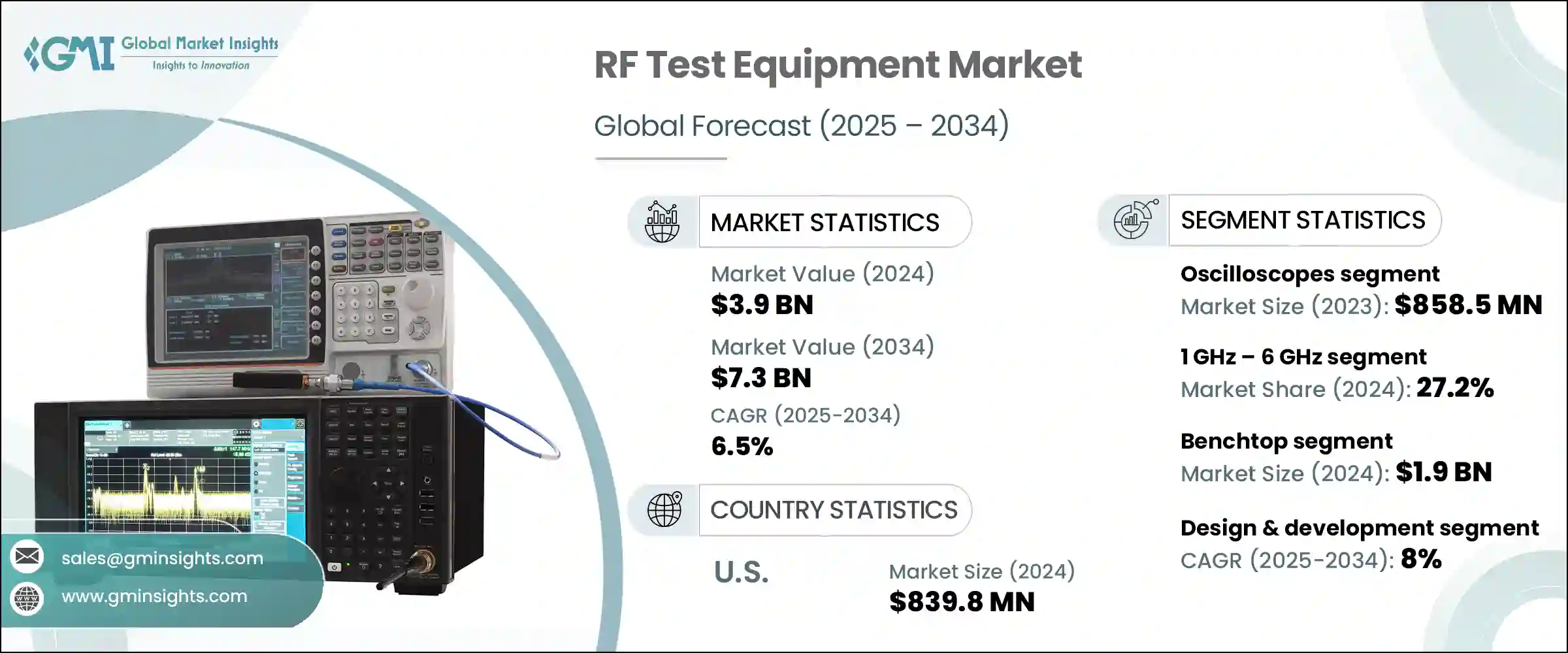

The Global RF Test Equipment Market was valued at USD 3.9 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 7.3 billion by 2034. Growth in this sector is being heavily influenced by the rising complexity of modern wireless communication technologies. As industries increasingly shift to 5G, mmWave applications, and the Internet of Things (IoT), the demand for accurate, multi-band testing solutions continues to surge. Regulatory compliance, performance validation, and interoperability verification are now considered non-negotiable requirements across telecommunications, defense, automotive, and industrial automation sectors.

As more devices become wirelessly connected and operate across crowded RF environments, the need for precise test equipment becomes essential for quality assurance, spectrum efficiency, and safety compliance. RF test solutions are also evolving to accommodate ultrahigh-frequency testing, driving demand across R&D labs and mission-critical engineering environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.9 Billion |

| Forecast Value | $7.3 Billion |

| CAGR | 6.5% |

Geopolitical developments have played a notable role in shaping the global RF test equipment landscape. Trade policies and tariffs, particularly those imposed during recent US administrations, have significantly impacted production costs and global supply chains by increasing import costs on key components and equipment.

The rapid advancement of 5G infrastructure has become one of the most powerful accelerators for RF test equipment demand. These next-generation communication systems utilize highly complex technologies like beamforming, massive MIMO, and mmWave transmissions, all of which require intricate validation. Precise RF testing is necessary to measure performance metrics, verify standard compliance, and guarantee compatibility across global bands and equipment suppliers.

Furthermore, as the 5G ecosystem expands into new domains like smart cities, autonomous mobility, and telemedicine, RF test equipment remains foundational to ensuring functionality across increasingly dense wireless environments. The proliferation of IoT solutions across healthcare, manufacturing, automotive, and smart homes has added another layer of complexity to RF testing. Devices operating on Wi-Fi, LoRa, Zigbee, and Bluetooth need to be validated not only for protocol compliance but also for coexistence and interference resilience in bandwidth-congested environments.

In 2023, the oscilloscope segment generated USD 858.5 million. These instruments are essential for visualizing and analyzing electrical signals in real-time. The rising intricacy of digital circuits, radio-frequency systems, and power electronics has made oscilloscopes indispensable in applications that require fine time-domain measurement. Industries such as R&D, automotive design, and wireless communication rely on these tools for diagnosing electrical behavior, troubleshooting systems, and validating design integrity with high levels of precision.

Test equipment designed for frequencies above the 40 GHz segment is anticipated to contribute a 24.8% share in 2024. These ultrahigh-frequency tools are primarily used in cutting-edge domains including 5G mmWave networks, advanced radar systems, space exploration, and early-stage terahertz experimentation. Engineers in high-stakes R&D environments demand low-noise, high-resolution instrumentation that can support next-generation connectivity and sensing applications. Though still an emerging segment, this category is gaining strong traction with research institutions and innovation labs pushing the frontiers of high-frequency technology.

Germany RF Test Equipment Market is forecasted to hit USD 352.9 million by 2034. The country's reputation for engineering excellence and industrial precision fuels the demand for advanced testing tools. The rise of Industry 4.0, including precision robotics and smart factories, requires reliable RF testing for seamless automation. Germany's rigorous manufacturing regulations, coupled with its focus on high-efficiency electronics, make it an ideal hub for continuous investment in RF testing infrastructure. The presence of strong domestic manufacturers and extensive R&D operations further reinforces Germany's importance in the global testing equipment landscape.

Key players in the RF Test Equipment Market include B&K Precision Corporation, Anritsu Corporation, and AR RF/Microwave Instrumentation, all of whom are actively shaping the future of RF validation technologies. Companies in the RF test equipment market are adopting several strategies to build market strength and adapt to evolving industry needs. A major focus has been on enhancing product portfolios by integrating support for higher frequencies, wider bandwidths, and multi-protocol environments to keep pace with 5G, satellite, and IoT advancements.

Strategic R&D investments are driving innovation in AI-enabled testing, automation, and cloud integration. Companies are also strengthening partnerships with telecom and aerospace manufacturers to co-develop solutions tailored to emerging applications. Geographic expansion into high-growth regions and localization of production are being pursued to reduce tariff impacts and supply chain risks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 5G network deployment

- 3.7.1.2 Proliferation of IoT devices

- 3.7.1.3 Advancements in automotive and aerospace technologies

- 3.7.1.4 Integration of AI and machine learning

- 3.7.1.5 Emergence of software-defined test equipment

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High cost of advanced RF test equipment

- 3.7.2.2 Complexity and rapid technological changes

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Oscilloscopes

- 5.3 Signal generators

- 5.4 Spectrum analyzers

- 5.5 Network analyzers

- 5.6 RF power meters

- 5.7 RF synthesizers

- 5.8 Others

Chapter 6 Market Estimates & Forecast, By Frequency Range, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Less than 1 GHz

- 6.3 1 GHz – 6 GHz

- 6.4 6 GHz – 18 GHz

- 6.5 18 GHz – 40 GHz

- 6.6 Above 40 GHz

Chapter 7 Market Estimates & Forecast, By Form Factor, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Benchtop

- 7.3 Portable/Handheld

- 7.4 Modular

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Design & development

- 8.3 Manufacturing

- 8.4 Installation & maintenance

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Telecommunications

- 9.3 Consumer electronics

- 9.4 Automotive & transportation

- 9.5 Aerospace & defense

- 9.6 Industrial

- 9.7 Medical

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Anritsu Corporation

- 11.2 AR RF/Microwave Instrumentation

- 11.3 B&K Precision Corporation

- 11.4 Berkeley Nucleonics Corporation

- 11.5 Bird Technologies

- 11.6 Copper Mountain Technologies

- 11.7 Giga-tronics Incorporated

- 11.8 Keysight Technologies

- 11.9 National Instruments (NI)

- 11.10 Qorvo

- 11.11 Rigol Technologies

- 11.12 Rohde & Schwarz

- 11.13 Saelig Company, Inc.

- 11.14 Signal Hound

- 11.15 Teledyne LeCroy

- 11.16 Teledyne Technologies Incorporated

- 11.17 Thorlabs, Inc.

- 11.18 Vaunix Technology Corporation

- 11.19 Yokogawa Electric Corporation