PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782122

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782122

Artificial Intelligence Generated Content (AIGC) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

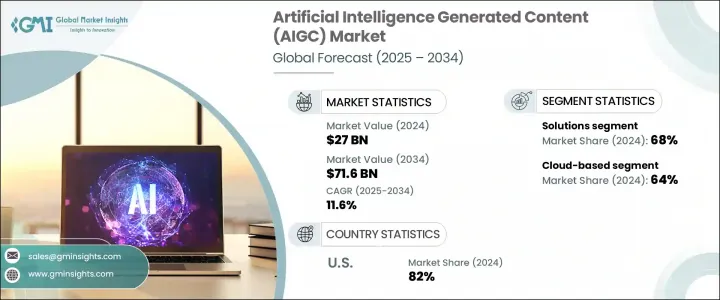

The Global Artificial Intelligence Generated Content Market was valued at USD 27 billion in 2024 and is estimated to grow at a CAGR of 11.6% to reach USD 71.6 billion by 2034. Traditional content creation, once a labor-intensive task, is now transforming into a streamlined, automated process powered by advanced AI technologies. As AI models become more sophisticated, content production is no longer confined to niche creative teams-it is becoming a core enterprise function. Organizations across sectors are prioritizing the development of AI-literate teams that can effectively navigate prompt engineering, ethical content use, and workflow optimization. This trend is turning AIGC upskilling into a critical element of digital transformation strategies.

Market expansion is being further fueled by a growing focus on skill development through collaborations between public agencies and private sector innovators. Various institutions are working together to create structured learning frameworks and credentialing systems to prepare the workforce for the demands of AI-driven content creation. Simultaneously, AIGC solution providers are integrating training modules into their platforms, ensuring users-from creatives to enterprise professionals-have access to scalable education resources. These efforts are accelerating adoption across industries ranging from marketing and entertainment to education and e-commerce.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27 Billion |

| Forecast Value | $71.6 Billion |

| CAGR | 11.6% |

The market is segmented by components into solutions and services. In 2024, solutions represented the largest share, accounting for nearly 68% of total revenue. This segment is expected to grow at a CAGR of over 12% between 2025 and 2034. AIGC solutions include AI-based platforms that generate text, images, videos, audio, and even code, providing businesses with tools for dynamic content development. These technologies support automation, real-time personalization, and creative agility, which are crucial in industries that rely on frequent content updates and brand engagement. Businesses are increasingly relying on these platforms to streamline marketing campaigns, enhance customer communication, and build immersive digital experiences.

By deployment, the AIGC market is categorized into cloud-based and on-premises models. Cloud-based solutions led the market with a 64% share in 2024 and are anticipated to register a CAGR of more than 13% through the forecast period. The preference for cloud-based tools is driven by their scalability, ease of integration, and real-time accessibility. Cloud infrastructure allows users to generate content via APIs and software-as-a-service (SaaS) models, promoting faster iterations and continuous workflow improvements. These tools eliminate infrastructure constraints and allow businesses to expand creative output across multiple platforms, making them especially popular in dynamic sectors like digital marketing, education, and e-commerce.

Based on technology, the market is segmented into several key innovations, including natural language processing (NLP), generative adversarial networks (GANs), transformer models, text-to-image models, text-to-video/3D, and speech-to-text or text-to-speech systems. Among these, transformer models held the dominant position in 2024. These models, known for their large-scale processing capabilities, are the foundation of many leading AIGC applications. Their ability to understand context, generate human-like responses, and synthesize information across formats makes them essential to powering multi-modal AI platforms. As transformer architectures continue to advance, they are enabling increasingly nuanced and adaptable content creation systems.

Regionally, the United States emerged as the leading market within North America, commanding around 82% of the regional share and generating approximately USD 7.6 billion in revenue in 2024. The country's dominance is driven by its strong innovation ecosystem, robust investment in AI research, and early enterprise adoption of AI technologies. A well-established digital economy and a dense concentration of AI technology providers continue to propel growth. The integration of AIGC tools into enterprise software stacks is driving high adoption across sectors such as media, education, advertising, and business services.

The AIGC landscape is shaped by a competitive environment, with key companies developing tools that support scalable content generation. These companies are focused on improving platform performance, enhancing user experiences, and supporting enterprise-grade applications to meet growing market demand. As the technology matures, AIGC is expected to become a foundational element of the global digital economy, influencing how content is imagined, created, and consumed.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment Mode

- 2.2.4 Technology

- 2.2.5 Content

- 2.2.6 Enterprise Size

- 2.2.7 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Explosive growth in digital content demand

- 3.2.1.2 Integration of AIGC into business apps

- 3.2.1.3 Advancements in foundation models

- 3.2.1.4 Need for localization & personalization

- 3.2.1.5 Rise of the creator economy

- 3.2.1.6 Cloud-based delivery models

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Intellectual property & copyright risks

- 3.2.2.2 Limited awareness among non-tech professionals

- 3.2.2.3 High computing resource requirements

- 3.2.2.4 Lack of content authenticity detection

- 3.2.3 Market opportunities

- 3.2.3.1 Industry-specific AIGC tools

- 3.2.3.2 Synthetic data generation

- 3.2.3.3 Multilingual and low-resource model development

- 3.2.3.4 Collaborative AI-human workflows

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software development & licensing cost

- 3.8.2 Deployment & integration cost

- 3.8.3 Maintenance & support cost

- 3.8.4 Cybersecurity & compliance cost

- 3.8.5 Training & change management cost

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Text generation tools

- 5.2.2 Image generation platforms

- 5.2.3 Video and animation generators

- 5.2.4 Audio and speech synthesis tools

- 5.2.5 Code generation platforms

- 5.3 Services

- 5.3.1 Consulting & strategy

- 5.3.2 Integration & deployment

- 5.3.3 Support & maintenance

- 5.3.4 Custom content development services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 On-premises

- 6.3 Cloud-based

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Natural Language Processing (NLP)

- 7.3 Generative Adversarial Networks (GAN)

- 7.4 Transformer models

- 7.5 Text-to-image models

- 7.6 Text-to-video/3D

- 7.7 Text-to-Speech (TTS)

- 7.8 Speech-to-Text (STT)

Chapter 8 Market Estimates & Forecast, By Content, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Text content

- 8.2.1 Blogs and articles

- 8.2.2 Marketing copy (ads, emails)

- 8.2.3 Scripts and dialogues

- 8.2.4 Product descriptions

- 8.3 Image Content

- 8.3.1 Digital art & illustrations

- 8.3.2 Product visuals

- 8.3.3 Marketing & social media graphics

- 8.4 Video Content

- 8.4.1 Explainer videos

- 8.4.2 Virtual presenters

- 8.4.3 Synthetic actors/avatars

- 8.5 Audio Content

- 8.5.1 Voiceovers

- 8.5.2 Podcasts

- 8.5.3 Audiobooks

- 8.6 Code Content

- 8.6.1 Web development scripts

- 8.6.2 Game development code

- 8.6.3 Automation scripts

Chapter 9 Market Estimates & Forecast, By Enterprise Size, 2021- 2034 ($Bn)

- 9.1 Key trends

- 9.2 Small enterprises

- 9.3 Medium enterprises

- 9.4 Large enterprises

Chapter 10 Market Estimates & Forecast, By Application, 2021- 2034 ($Bn)

- 10.1 Key trends

- 10.2 Marketing & advertising

- 10.3 Media & entertainment

- 10.4 E-commerce & retail

- 10.5 Education & training

- 10.6 Customer service & virtual assistance

- 10.7 Software & game development

- 10.8 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Indonesia

- 11.4.7 Philippines

- 11.4.8 Singapore

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Adobe

- 12.2 Alibaba Cloud

- 12.3 Amazon Web Services (AWS)

- 12.4 Anthropic

- 12.5 Baidu

- 12.6 Canva

- 12.7 Copy.ai

- 12.8 Descript

- 12.9 Google DeepMind

- 12.10 IBM

- 12.11 Jasper AI

- 12.12 Meta (Facebook AI)

- 12.13 Microsoft

- 12.14 NVIDIA

- 12.15 OpenAI

- 12.16 Pika Labs

- 12.17 Rephrase.ai

- 12.18 Runway

- 12.19 Stability AI

- 12.20 Synthesia