PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782126

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1782126

Duodenal Ulcer Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

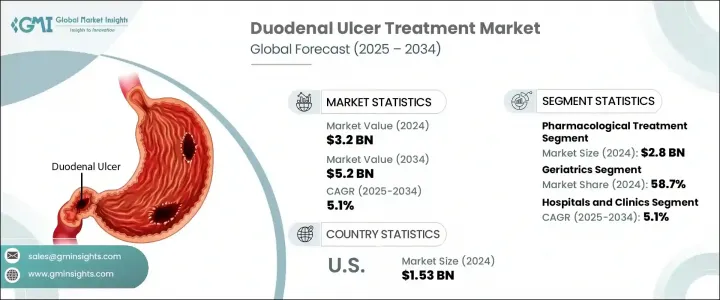

The Global Duodenal Ulcer Treatment Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 5.2 billion by 2034. This growth is largely fueled by rising cases of duodenal ulcers worldwide, often linked to poor nutrition, alcohol intake, and smoking habits. An aging population also contributes to increased demand for treatment solutions, as older individuals are more susceptible to gastrointestinal complications. Medications such as H2 receptor blockers and proton pump inhibitors (PPIs) are seeing heightened usage due to their reliable acid-suppressing abilities and favorable safety profiles.

In many treatment plans, these are now used in conjunction with antibiotics that target Helicobacter pylori infections- a leading cause of duodenal ulcers. Additionally, agents like sucralfate and misoprostol are gaining traction for their protective effects on the gastric lining. The integration of AI diagnostics, mobile health tools, and telemedicine is reshaping how ulcer care is delivered, with a focus on accessibility and patient-centered treatment. As more healthcare systems adopt digital health models and preventive strategies, the demand for reliable duodenal ulcer treatments continues to grow across all regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.1% |

The pharmacological therapies segment generated USD 2.8 billion in 2024. This dominance stems from the effectiveness of drug classes like PPIs and H2 blockers in providing quick symptom relief and consistent acid control. These medications are widely preferred for their ease of use, oral delivery, and overall convenience, which support home-based care and long-term patient adherence. Their ability to manage symptoms effectively without invasive procedures makes them the first choice for both healthcare providers and patients, pushing growth in this treatment category.

The geriatrics segment held a 58.7% share in 2024. Age-related declines in gastrointestinal protection increase vulnerability to ulcer formation among older adults, making them the primary consumer group for treatment options. Additionally, chronic use of non-steroidal anti-inflammatory drugs (NSAIDs) to manage other age-related conditions significantly raises the risk of duodenal ulcers in this demographic. This persistent exposure to ulcerogenic triggers calls for long-term and preventive care approaches tailored to senior patients.

United States Duodenal Ulcer Treatment Market was valued at USD 1.53 billion in 2025. The American market continues to grow due to the increasing prevalence of Helicobacter pylori infections, frequent NSAID use, and dietary risk factors. The country's emphasis on early detection and robust treatment protocols supports timely diagnosis and intervention. Strong infrastructure in healthcare delivery, along with extensive awareness campaigns and access to cutting-edge diagnostic services, ensures high treatment adoption. Ongoing investments in therapeutic research and innovation also bolster the country's role in shaping the global duodenal ulcer treatment landscape.

Key industry players in this market include Takeda Pharmaceutical, Abbott Laboratories, Boehringer Ingelheim, Cipla, Eisai, GlaxoSmithKline, Pfizer, Merck, Lupin, Novartis, Ferozsons Laboratories, Sun Pharma, Sanofi, and AstraZeneca. To strengthen their market position, companies operating in the duodenal ulcer treatment space are embracing various strategic initiatives. Investment in advanced drug development targeting both symptom management and root causes, such as Helicobacter pylori, is a key focus.

Many firms are enhancing their global reach through partnerships, local manufacturing, and regional marketing strategies. Digital health integration, such as smart monitoring and telehealth-enabled treatment, is being explored to boost patient engagement and adherence. Additionally, firms are diversifying portfolios to include combination therapies, aiming to improve efficacy and compliance. Strategic pricing, patient assistance programs, and physician education campaigns also support broader market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Treatment type

- 2.2.3 Age group

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of helicobacter pylori infections

- 3.2.1.2 Expansion of telemedicine and digital diagnostics

- 3.2.1.3 Growing awareness of gastrointestinal health

- 3.2.1.4 Technological advancements in acid-suppressing therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of endoscopic and pH monitoring procedures

- 3.2.2.2 Adverse effects

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding healthcare in developing regions

- 3.2.3.2 Growing public-private partnerships for affordable drug access

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Future market trends

- 3.6 Technology and innovation landscape

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmacological treatment

- 5.2.1 Drug class

- 5.2.1.1 Proton pump inhibitors

- 5.2.1.2 H2 antagonists

- 5.2.1.3 Antibiotics

- 5.2.1.4 Other drug classes

- 5.2.2 Medication type

- 5.2.2.1 Branded Treatment

- 5.2.2.2 Generics

- 5.2.3 Route of administration

- 5.2.3.1 Oral

- 5.2.3.2 Parenteral

- 5.2.1 Drug class

- 5.3 Surgery

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adults

- 6.3 Geriatrics

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Homecare settings

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AstraZeneca

- 9.3 Boehringer Ingelheim

- 9.4 Cipla

- 9.5 Eisai

- 9.6 Ferozsons Laboratories

- 9.7 GlaxoSmithKline

- 9.8 Lupin

- 9.9 Merck

- 9.10 Novartis

- 9.11 Pfizer

- 9.12 Sanofi

- 9.13 Sun Pharma

- 9.14 Takeda Pharmaceutical