PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797719

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797719

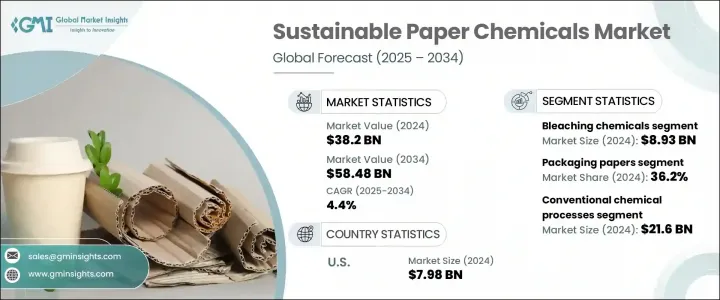

Sustainable Paper Chemicals Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

The Global Sustainable Paper Chemicals Market was valued at USD 38.2 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 58.48 billion by 2034. The increasing global preference for environmentally responsible solutions continues to elevate demand for sustainable alternatives in paper manufacturing. Chemicals derived from renewable sources that support lower water consumption and energy efficiency are aligning well with global efforts toward cleaner production. Rising awareness of ecological challenges, stricter environmental mandates, and a growing push toward circular economy models are reinforcing the switch to sustainable formulations.

The market is expected to experience continuous expansion as manufacturers shift away from conventional paper-making additives in favor of biodegradable, recyclable, and non-toxic substitutes. These advancements are not only improving the ecological impact of paper production but are also boosting the functional capabilities of paper products in terms of durability, print quality, and recyclability. Governments around the world are also channeling investments into research for green chemical alternatives and functional additives, further strengthening the paper sector's commitment to sustainable transformation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $38.2 Billion |

| Forecast Value | $58.48 Billion |

| CAGR | 4.4% |

In 2024, the packaging paper segment represented a 36.2% share. This segment has witnessed rapid growth as demand accelerates for eco-friendly coatings, barrier agents, and strength enhancers that maintain package performance while supporting recyclability and compostability. The rise of online retail and food delivery services has only intensified the need for paper packaging that is both functional and compliant with sustainability goals. Brands are increasingly leaning toward bio-based chemical inputs that reduce their environmental footprint while still meeting performance expectations for moisture resistance, durability, and printability.

The conventional chemical processing segment generated USD 21.6 billion in 2024. These well-established methods remain dominant due to their scalability, cost advantages, and ease of integration into existing paper mill operations. While rooted in tradition, these systems are evolving under the influence of regulatory reforms that demand cleaner, more resource-efficient practices. Innovations-such as biotechnology, nanotechnology, and AI-driven production monitoring-are being applied to further optimize the use of chemicals in the manufacturing cycle. As a result, conventional methods are gradually adapted to meet sustainability metrics without disrupting operational continuity.

United States Sustainable Paper Chemicals Market generated USD 7.98 billion in 2024, driven by the sustainable paper chemicals market. The country's position stems from its well-developed production infrastructure, emphasis on regulatory compliance, and growing consumer preference for environmentally safe paper and packaging products. Demand is being further driven by large-scale adoption of green chemistry across printing, packaging, and publishing segments. Meanwhile, Canada is experiencing steady progress as regional programs promote cleaner technologies and circular practices, encouraging local paper producers to transition toward safer, renewable chemical inputs.

Key companies shaping the competitive landscape of the Sustainable Paper Chemicals Market include Dow Inc., Solenis LLC, SNF Group, Buckman Laboratories International, Inc., Kemira Oyj, Ashland Global Holdings Inc., Nouryon, Ecolab Inc., Clariant AG, and BASF SE. Leading players in the sustainable paper chemicals market are adopting multi-pronged strategies to build a strong global presence. These companies are heavily investing in R&D to develop advanced bio-based and biodegradable chemicals that align with evolving regulatory standards and sustainability benchmarks. Expanding production capacities and forming regional partnerships allow them to improve distribution networks and access emerging markets. Strategic acquisitions and joint ventures are also being used to integrate green chemistry solutions into broader portfolios.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 Technology trends

- 2.2.4 End use industry trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Units)

- 5.1 Key trends

- 5.2 Bleaching chemicals

- 5.2.1 Chlorine dioxide

- 5.2.2 Hydrogen peroxide

- 5.2.3 Oxygen-based bleaching agents

- 5.2.4 Enzyme-based bleaching systems

- 5.3 Coating chemicals

- 5.3.1 Starch-based coatings

- 5.3.2 Latex coatings

- 5.3.3 Barrier coatings

- 5.3.4 Bio-based coating solutions

- 5.4 Process chemicals

- 5.4.1 Pulping chemicals

- 5.4.2 Deinking chemicals

- 5.4.3 Flotation chemicals

- 5.4.4 Cleaning chemicals

- 5.5 Functional chemicals

- 5.5.1 Wet strength agents

- 5.5.2 Dry strength agents

- 5.5.3 Retention and drainage aids

- 5.5.4 Sizing agents

- 5.6 Specialty additives

- 5.6.1 Defoamers

- 5.6.2 Biocides

- 5.6.3 Corrosion inhibitors

- 5.6.4 Ph control agents

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Units)

- 6.1 Key trends

- 6.2 Packaging papers

- 6.2.1 Corrugated packaging

- 6.2.2 Folding cartons

- 6.2.3 Food packaging

- 6.2.4 Industrial packaging

- 6.3 Tissue and hygiene products

- 6.3.1 Facial tissue

- 6.3.2 Toilet paper

- 6.3.3 Paper towels

- 6.3.4 Napkins

- 6.4 Printing and writing papers

- 6.4.1 Coated papers

- 6.4.2 Uncoated papers

- 6.4.3 Newsprint

- 6.4.4 Book papers

- 6.5 Specialty papers

- 6.5.1 Security papers

- 6.5.2 Filter papers

- 6.5.3 Decorative papers

- 6.5.4 Technical papers

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million) (Units)

- 7.1 Key trends

- 7.2 Conventional chemical processes

- 7.2.1 Kraft pulping

- 7.2.2 Sulfite pulping

- 7.2.3 Mechanical pulping

- 7.3 Sustainable chemical processes

- 7.3.1 Enzymatic processes

- 7.3.2 Bio-based chemical processes

- 7.3.3 Green Chemistry applications

- 7.3.4 Closed-loop systems

- 7.4 Emerging technologies

- 7.4.1 Nanotechnology applications

- 7.4.2 Biotechnology solutions

- 7.4.3 Digital process control

- 7.4.4 Artificial intelligence integration

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million) (Units)

- 8.1 Key trends

- 8.2 Food and beverage industry

- 8.2.1 Food packaging

- 8.2.2 Beverage packaging

- 8.2.3 Quick service restaurants

- 8.3 Healthcare and pharmaceuticals

- 8.3.1 Medical packaging

- 8.3.2 Pharmaceutical packaging

- 8.3.3 Healthcare hygiene products

- 8.4 Consumer Goods

- 8.4.1 Personal care products

- 8.4.2 Household products

- 8.4.3 E-commerce packaging

- 8.5 Industrial applications

- 8.5.1 Automotive industry

- 8.5.2 Electronics industry

- 8.5.3 Construction industry

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Kemira Oyj

- 10.2 BASF SE

- 10.3 Solenis LLC

- 10.4 Nouryon (formerly AkzoNobel Specialty Chemicals)

- 10.5 Ecolab Inc.

- 10.6 SNF Group

- 10.7 Ashland Global Holdings Inc.

- 10.8 Clariant AG

- 10.9 Dow Inc.

- 10.10 Buckman Laboratories International, Inc.