PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797742

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797742

Southeast Asia Box Truck Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

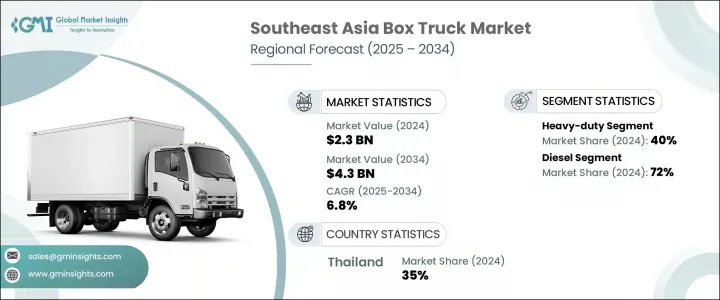

Southeast Asia Box Truck Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 4.3 billion by 2034. This growth is fueled by the rise in temperature-sensitive supply chains across the region, particularly for pharmaceuticals, vaccines, and fresh food. Increasing exports of pharma products and perishable goods from countries like Thailand, Malaysia, and Vietnam are accelerating the adoption of insulated and refrigerated box trucks. The expansion of organized cold chains, combined with the growth in urban grocery distribution and demand for temperature-controlled last-mile delivery, is encouraging businesses to invest in customized 5-ton box trucks. These trends are contributing to an uptick in fleet modernization and thermally efficient retrofitting across key logistics hubs.

To meet evolving delivery requirements, logistics operators are integrating AI-enabled telematics and route optimization tools in box trucks to enhance asset visibility, reduce fuel consumption, and minimize downtime. Systems such as geo-fencing, real-time heatmaps, and predictive fuel analytics are turning conventional trucks into smart logistics units. This shift from static transportation to intelligent freight orchestration is transforming box trucks into core components of digitally connected supply chains. Enhanced routing, performance tracking, and telematics integration are helping companies achieve higher payload efficiency while reducing operational costs and delivery delays.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.3 Billion |

| CAGR | 6.8% |

In 2024, heavy-duty box trucks accounted for a 40% share and are projected to grow at a CAGR of 6% through 2034. The strong performance of this segment is supported by the rising demand for robust, high-capacity vehicles with advanced safety features and compliance-ready platforms. Regional manufacturers are allocating more resources to R&D to meet evolving regulations. The introduction of intelligent braking systems, stability controls, and automated assistance features in next-generation trucks is reinforcing user trust in long-haul logistics operations and expanding their uptake across high-volume applications.

The diesel-powered segment held a 72% share in 2024 and is expected to maintain steady growth at over 6% CAGR during the forecast period. Diesel box trucks continue to lead due to their superior torque, load-pulling capacity, and fuel economy across long distances and challenging terrains. The widespread infrastructure supporting diesel refueling, coupled with lower running costs and the durability of diesel engines, is further supporting adoption. Additionally, the lack of spark plug systems reduces the need for frequent maintenance, adding operational value and keeping ownership costs down over time.

Thailand Southeast Asia Box Truck Market held a 35% share and generated USD 813.9 million in 2024. Growth in Thailand is supported by a solid presence of major automotive manufacturers and established commercial vehicle assembly facilities. Continued demand for intercity and cross-border freight movement is reinforcing the need for durable box trucks across industries. Government policies encouraging the adoption of autonomous and hybrid trucks are also making the region an ideal landscape for innovation and deployment. The country's regulatory and financial support for alternative energy vehicles is further creating momentum in the transition to next-generation transport solutions.

The leading players in the Southeast Asia Box Truck Market include Hino, Volvo, PACCAR, Daimler, MAN, Isuzu, and TATA. These companies are actively shaping the competitive landscape by leveraging innovation, partnerships, and regional production strengths. To strengthen their position in the Southeast Asia box truck market, companies are adopting a multi-pronged strategy. Many are localizing production and assembly to align with regional cost dynamics while improving supply chain responsiveness. Strategic investments are being made in vehicle electrification, hybrid powertrains, and telematics systems to cater to evolve regulations and sustainability goals. OEMs are also focusing on upgrading safety and automation features to gain a competitive edge. Collaborations with logistics companies and digital platform providers help truck manufacturers optimize vehicle platforms for real-time monitoring and last-mile delivery.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Fuel

- 2.2.4 Application

- 2.2.5 Body

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Cold chain expansion in pharma and food industries

- 3.2.1.2 Surge in urban e-commerce fulfilment

- 3.2.1.3 Increased demand for customized refrigerated and insulated box trucks

- 3.2.1.4 Government EV policies and urban vehicle electrification targets

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Inconsistent cold chain standards across ASEAN borders

- 3.2.2.2 Infrastructure and charging limitations outside Tier-I cities

- 3.2.3 Market opportunities

- 3.2.3.1 AI-enabled telematics and fleet orchestration tools

- 3.2.3.2 Cross-border refurbishing and resale of reefer trucks

- 3.2.3.3 Last-mile electric logistics with box trucks <3.5 tons

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Brunei

- 3.4.2 Cambodia

- 3.4.3 East Timor

- 3.4.4 Indonesia

- 3.4.5 Laos

- 3.4.6 Malaysia

- 3.4.7 Myanmar

- 3.4.8 Philippines

- 3.4.9 Singapore

- 3.4.10 Thailand

- 3.4.11 Vietnam

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 E-commerce and logistics industry integration

- 3.13.1 E-commerce growth impact on demand

- 3.13.2 Last-mile delivery requirements

- 3.13.3 Logistics service provider trends

- 3.13.4 Warehouse and distribution center development

- 3.13.5 Cross-border e-commerce logistics

- 3.13.6 Same-day and instant delivery trends

- 3.14 Fleet management and operational efficiency

- 3.14.1 Fleet optimization strategies

- 3.14.2 Route planning and optimization

- 3.14.3 Fuel management systems

- 3.14.4 Driver training and safety programs

- 3.14.5 Maintenance scheduling and management

- 3.14.6 Total cost of ownership analysis

- 3.15 Infrastructure development and urban planning

- 3.15.1 Road infrastructure development

- 3.15.2 Urban logistics planning

- 3.15.3 Loading and unloading facilities

- 3.15.4 Traffic management systems

- 3.15.5 Parking and storage facilities

- 3.15.6 Smart city initiatives impact

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Brunei

- 4.2.2 Cambodia

- 4.2.3 East Timor

- 4.2.4 Indonesia

- 4.2.5 Laos

- 4.2.6 Malaysia

- 4.2.7 Myanmar

- 4.2.8 Philippines

- 4.2.9 Singapore

- 4.2.10 Thailand

- 4.2.11 Vietnam

- 4.3 Strategic dashboard

- 4.3.1 Revenue performance comparison

- 4.3.2 Transaction volume analysis

- 4.3.3 Geographic presence mapping

- 4.3.4 Service portfolio breadth

- 4.3.5 Technology capability assessment

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.5.1 Digital natives vs traditional players

- 4.5.2 Full-service vs specialized platforms

- 4.5.3 Regional champions vs pan-ASEAN players

- 4.5.4 Premium vs mass market focus

- 4.6 Strategic outlook matrix

- 4.7 Key developments

- 4.7.1 Mergers & acquisitions

- 4.7.2 Partnerships & collaborations

- 4.7.3 New Product Launches

- 4.7.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Light duty

- 5.3 Medium duty

- 5.4 Heavy duty

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

- 6.4.1 BEV

- 6.4.2 HEV

- 6.4.3 PHEV

- 6.4.4 FCEV

- 6.5 Alternative fuel

- 6.5.1 CNG

- 6.5.2 LPG

- 6.5.3 Biodiesel

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Distribution & urban logistics

- 7.3 Retail

- 7.4 Food & Beverage

- 7.5 Construction

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Body, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Standard

- 8.3 Refrigerated

- 8.4 Insulated

- 8.5 Specialized

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 Brunei

- 9.3 Cambodia

- 9.4 East Timor

- 9.5 Indonesia

- 9.6 Laos

- 9.7 Malaysia

- 9.8 Myanmar

- 9.9 Philippines

- 9.10 Singapore

- 9.11 Thailand

- 9.12 Vietnam

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 Dongfeng

- 10.1.2 Ford

- 10.1.3 Foton

- 10.1.4 Fuso

- 10.1.5 Hino

- 10.1.6 Hyundai

- 10.1.7 Isuzu

- 10.1.8 JAC

- 10.1.9 Mahindra

- 10.1.10 Tata

- 10.2 Regional players

- 10.2.1 Ford Thailand

- 10.2.2 Hino Indonesia

- 10.2.3 Hyundai Vietnam

- 10.2.4 Isuzu Thailand

- 10.2.5 Mitsubishi Thailand

- 10.2.6 Tan Chong

- 10.2.7 THACO

- 10.2.8 Thonburi

- 10.3 Emerging players

- 10.3.1 BYD

- 10.3.2 Changan

- 10.3.3 Daimler

- 10.3.4 Geely

- 10.3.5 Great Wall

- 10.3.6 JMC

- 10.3.7 Maxus

- 10.3.8 SAIC

- 10.3.9 Scania

- 10.3.10 Volvo