PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797812

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797812

Automotive Optical Sensor IC Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

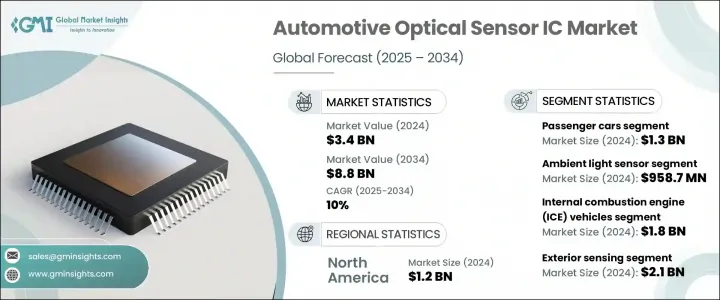

The Global Automotive Optical Sensor IC Market was valued at USD 3.4 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 8.8 billion by 2034. The growth is driven by rapid technological advancement, increased demand for driver assistance systems, and the evolution of autonomous vehicles. The demand is primarily being fueled by the expanding adoption of optical sensors in automobiles for safety, comfort, and performance enhancements. Automakers are under increasing pressure to meet evolving regulatory safety mandates, which is contributing to the integration of sophisticated sensing components in modern vehicles.

The automotive sector is increasingly turning to optical sensor ICs due to their role in enhancing advanced driver assistance systems (ADAS). Features such as adaptive cruise control, lane keeping, and blind spot monitoring rely heavily on these sensors. The growing complexity of automotive systems and rising consumer expectations for smarter, safer, and more intuitive driving experiences have significantly increased the need for precise and high-performance sensor technologies. Optical sensors, in particular, are highly valued for their speed, accuracy, and ability to function effectively under diverse lighting and environmental conditions. As more OEMs aim to meet stringent safety benchmarks and offer premium vehicle experiences, the use of optical sensor ICs is rapidly expanding.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 Billion |

| Forecast Value | $8.8 Billion |

| CAGR | 10% |

In terms of vehicle type, the passenger cars segment led the global market and was valued at USD 1.3 billion in 2024. The increasing demand for high-end features in this segment, including enhanced safety, comfort, and interior aesthetics, is encouraging automakers to integrate more optical sensor-based systems. Sensor ICs are being embedded to support applications ranging from automated headlights to cabin light adjustments, aligning with the growing push towards smart mobility solutions. As electric and autonomous passenger cars continue to gain traction, the reliance on optical sensor ICs is anticipated to grow substantially.

When categorized by sensor type, ambient light sensors commanded the largest market share, reaching USD 958.7 million in 2024. These sensors are vital for adjusting both internal and external vehicle lighting in real-time, thereby improving visibility, reducing distractions, and enhancing overall driving comfort. The rising demand for user-friendly lighting systems that adapt to changing environments is fostering the continued adoption of ambient light sensors across various vehicle models.

By application, the automotive optical sensor IC market is divided into interior and exterior sensing. Among these, the exterior sensing segment dominated with a market value of USD 2.1 billion in 2024. Exterior sensing technologies are used to monitor surroundings, detect nearby objects, and respond dynamically to road conditions. These functions are crucial for supporting systems such as pedestrian detection, emergency braking, and blind spot recognition. Optical sensors, including LiDAR, infrared, and camera modules, are at the core of these capabilities. The need for robust, water-resistant, and accurate sensors for external applications continues to rise, especially as vehicle manufacturers prioritize high-performance driver assistance features to comply with global safety standards and New Car Assessment Programs (NCAP).

Regionally, North America stood out as the dominant market, accounting for USD 1.2 billion in 2024. The region benefits from a strong regulatory framework supporting vehicle safety and an advanced ecosystem for the development of autonomous and electric vehicles. In the United States, the market reached a valuation of USD 910.4 million in 2024, growing at a CAGR of 10.5%. Policy initiatives to support domestic semiconductor production are expected to significantly impact the availability and cost-efficiency of automotive sensor components in the coming years, further bolstering market expansion.

Key companies operating in the automotive optical sensor IC market include Panasonic Corporation, ON Semiconductor Corporation, Melexis NV, Autoliv Inc., Analog Devices, Inc., STMicroelectronics N.V., Omnivision Technologies, Inc., Broadcom Inc., NVIDIA Corporation, Infineon Technologies AG, Robert Bosch GmbH, Microchip Technology Inc., Continental AG, Aptiv PLC, ams-OSRAM AG, LeddarTech Inc., Texas Instruments Incorporated, NXP Semiconductors N.V., Hamamatsu Photonics K.K., and Denso Corporation. These players are focusing on innovations in sensing technology, improved chip performance, and partnerships with automotive OEMs to stay competitive in the evolving landscape.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Sensor type trends

- 2.2.2 Vehicle type trends

- 2.2.3 Propulsion type trends

- 2.2.4 Application trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing adoption of advanced driver assistance systems (ADAS)

- 3.2.1.2 Growth of autonomous vehicle development

- 3.2.1.3 Increasing road safety regulatory mandates

- 3.2.1.4 Consumer demand for enhanced in-vehicle experiences

- 3.2.1.5 Growing demand for advancements in sensor technology

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High development and implementation costs

- 3.2.2.2 Integration complexity with existing systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Sustainability measures

- 3.11 Consumer sentiment analysis

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, by Sensor Type, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Ambient light sensors

- 5.3 Infrared (IR) sensors

- 5.4 Lidar sensors

- 5.5 Proximity sensors

- 5.6 Rain and sunlight sensors

- 5.7 Others

Chapter 6 Market estimates and forecast, by Vehicle Type, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.3 Light commercial vehicle (LCV)

- 6.4 Medium commercial vehicle (MCV)

- 6.5 Heavy commercial vehicle (HCV)

Chapter 7 Market estimates and forecast, by Propulsion Type, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 Electric vehicles (EVs)

- 7.3 Internal combustion engine (ICE) vehicles

Chapter 8 Market estimates and forecast, by Application, 2021 - 2034 (USD Billion)

- 8.1 Key trends

- 8.2 Interior sensing

- 8.3 Exterior sensing

Chapter 9 Market estimates and forecast, by region, 2021 - 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 Uk

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company profiles

- 10.1 AMS-OSRAM AG

- 10.2 Analog Devices, Inc.

- 10.3 Aptiv PLC

- 10.4 Autoliv Inc.

- 10.5 Broadcom Inc.

- 10.6 Continental AG

- 10.7 Denso Corporation

- 10.8 Hamamatsu Photonics K.K.

- 10.9 Infineon Technologies AG

- 10.10 LeddarTech Inc.

- 10.11 Melexis NV

- 10.12 Microchip Technology Inc.

- 10.13 NVIDIA Corporation

- 10.14 NXP Semiconductors N.V.

- 10.15 ON Semiconductor Corporation

- 10.16 Omnivision Technologies, Inc.

- 10.17 Panasonic Corporation

- 10.18 Robert Bosch GmbH

- 10.19 STMicroelectronics N.V.

- 10.20 Texas Instruments Incorporated