PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797817

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797817

Asia Pacific Less-Than-Container Load Shipping Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

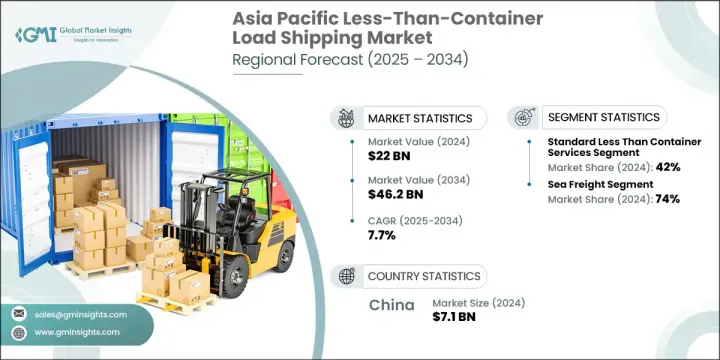

Asia Pacific Less-Than-Container Load Shipping Market was valued at USD 22 billion in 2024 and is estimated to grow at a CAGR of 7.7% to reach USD 46.2 billion by 2034. The region is experiencing significant growth in international shipping volumes, driven by increasing exports and manufacturing activity. The need for cost-effective, flexible, and frequent shipments is rising as businesses shift from bulk to smaller volume, just-in-time deliveries. This trend is helping LCL shipping gain traction, offering better agility in supply chain management. Rapid e-commerce growth, especially among small and mid-sized businesses, is further accelerating the demand for LCL logistics. With supply chains being increasingly optimized to manage dynamic market conditions, LCL services are enabling companies to maintain operational flexibility and reduce excess inventory. Regional supply networks are being transformed through improved infrastructure and policy frameworks. Development efforts are enhancing port operations, streamlining intermodal routes, and boosting overall logistics efficiency, contributing to faster and more reliable shipping. These dynamics are creating strong momentum for LCL services, which now play a vital role in the shifting trade patterns and evolving shipping needs across Asia Pacific's diverse economies.

Ongoing growth in the manufacturing and export sectors across nations such as Vietnam, China, and India is intensifying the need for smaller, more frequent international shipments. LCL shipping has emerged as a practical solution, offering flexibility and cost benefits that suit fluctuating demand cycles. As export volumes increase, companies are finding value in LCL logistics, which allow them to avoid the risks of overstocking and respond more effectively to market changes. Much of the market's momentum comes from the surge in e-commerce and the rising participation of SMEs in global trade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22 Billion |

| Forecast Value | $46.2 Billion |

| CAGR | 7.7% |

The standard LCL services segment held a 42% share in 2024 and is projected to grow at a CAGR of 5% through 2034. Their popularity lies in their cost efficiency and adaptability for various industries. This option suits companies shipping moderate volumes without time-sensitive constraints. For SMEs and exporters, it remains an accessible and affordable solution, particularly in industries where shipment size varies or timing is less critical.

The sea freight segment held a 74% share in 2024 and is expected to grow at a CAGR of 6% from 2025 to 2034. The presence of major trade routes and vast coastlines, along with the region's strong position in global manufacturing, has made sea freight the preferred mode for LCL shipping. Major regional ports now support mature and efficient LCL operations, contributing to faster handling times and greater shipping capacity for small consignments.

China Less-Than-Container Load Shipping Market held a 32% share in 2024, generating USD 7.1 billion. Its position as a top global manufacturing hub, coupled with a highly efficient logistics infrastructure, strengthens its hold on the market. China's expansive export activity and robust trade connections make it a critical player in this space, particularly with the rise of new industries and rapid digitalization across shipping processes.

Key companies driving the Asia Pacific Less-Than-Container Load Shipping Market include Expeditors International of Washington, DSV, DHL Global Forwarding, Kerry Logistics Network, Kuehne+Nagel International, C.H. Robinson Worldwide, and Dimerco Express. Market leaders in Asia Pacific's LCL shipping space are scaling their presence by investing in digital transformation, automation, and data-driven logistics platforms. These enhancements support real-time tracking, cost estimation, and demand forecasting, making LCL services more efficient and appealing. To strengthen their regional footprint, companies are expanding their warehousing and consolidation centers near major ports and trade corridors. Strategic alliances and long-term service agreements with regional carriers are also helping secure capacity and ensure timely deliveries.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service

- 2.2.3 Mode of transport

- 2.2.4 Shipper

- 2.2.5 Destination

- 2.2.6 Commodity

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of SME

- 3.2.1.2 Rising E-commerce and cross-border trade

- 3.2.1.3 Infrastructure development and port modernization

- 3.2.1.4 Increased focus on supply chain flexibility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Longer transit times compared to full container load

- 3.2.2.2 Higher risk of cargo damage or misplacement

- 3.2.3 Market opportunities

- 3.2.3.1 Digitalization of freight booking and tracking systems

- 3.2.3.2 Growth in intra-Asia trade routes and partnerships

- 3.2.3.3 Rise of D2C brands and global micro-exporters

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 China

- 3.4.2 Japan

- 3.4.3 South Korea

- 3.4.4 Singapore

- 3.4.5 Hong Kong

- 3.4.6 Australia

- 3.4.7 India

- 3.4.8 Thailand

- 3.4.9 Malaysia

- 3.4.10 Indonesia

- 3.4.11 Vietnam

- 3.4.12 Philippines

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Digital freight platforms and marketplaces

- 3.7.1.2 Automated consolidation systems

- 3.7.1.3 IoT-enabled cargo tracking

- 3.7.1.4 AI-powered route optimization

- 3.7.1.5 Blockchain for documentation

- 3.7.1.6 Predictive analytics for demand forecasting

- 3.7.2 Emerging technologies

- 3.7.1 Current technological trends

- 3.8 LCL vs FCL comparative analysis

- 3.8.1 Cost benefit

- 3.8.2 Customer preference

- 3.8.3 Transit time

- 3.8.4 Container size

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By mode of transport

- 3.10 Shipping logistics statistics

- 3.10.1 Major ports and corridors

- 3.10.1.1 Singapore hub

- 3.10.1.2 Hong Kong hub

- 3.10.1.3 Shanghai hub

- 3.10.1.4 Busan hub

- 3.10.1.5 Tokyo/Yokohama Hub

- 3.10.1.6 Others

- 3.10.2 Top exporting and importing countries

- 3.10.3 Major commodities

- 3.10.1 Major ports and corridors

- 3.11 Cost breakdown analysis

- 3.12 Patent analysis

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 China

- 4.2.2 Japan

- 4.2.3 South Korea

- 4.2.4 Singapore

- 4.2.5 Hong Kong

- 4.2.6 Australia

- 4.2.7 India

- 4.2.8 Thailand

- 4.2.9 Malaysia

- 4.2.10 Indonesia

- 4.2.11 Vietnam

- 4.2.12 Philippines

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Standard less than container services

- 5.3 Express less than container services

- 5.4 Temperature-controlled less than container

- 5.5 Hazardous cargo less than container

- 5.6 Project and break-bulk less than container

- 5.7 Door-to-door less than container services

Chapter 6 Market Estimates & Forecast, By Mode of Transport, 2021 - 2034 ($Bn, TEU)

- 6.1 Key trends

- 6.2 Sea freight

- 6.3 Air freight

- 6.4 Land freight

Chapter 7 Market Estimates & Forecast, By Shipper, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 SME

- 7.3 Large enterprises

Chapter 8 Market Estimates & Forecast, By Destination, 2021 - 2034 ($Bn, TEU)

- 8.1 Key trends

- 8.2 Domestic less than container shipping

- 8.3 International less than container shipping

Chapter 9 Market Estimates & Forecast, By Commodity, 2021 - 2034 ($Bn, TEU)

- 9.1 Key trends

- 9.2 Electronics and high-tech products

- 9.3 Textiles and apparel

- 9.4 Machinery and industrial equipment

- 9.5 Automotive parts and components

- 9.6 Consumer goods and retail products

- 9.7 Food and beverages

- 9.8 Medical equipment and pharmaceuticals

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, TEU)

- 10.1 Key trends

- 10.2 China

- 10.3 Japan

- 10.4 South Korea

- 10.5 Singapore

- 10.6 Hong Kong

- 10.7 Australia

- 10.8 India

- 10.9 Thailand

- 10.10 Malaysia

- 10.11 Indonesia

- 10.12 Vietnam

- 10.13 Philippines

- 10.14 Rest of APAC

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 BDP International

- 11.1.2 C.H. Robinson

- 11.1.3 DHL Global Forwarding

- 11.1.4 DB Schenker

- 11.1.5 DSV

- 11.1.6 Expeditors International of Washington

- 11.1.7 Kuehne+Nagel International

- 11.1.8 Kintetsu World Express

- 11.1.9 Nippon Express Holdings

- 11.1.10 Yusen Logistics

- 11.2 Regional players

- 11.2.1 Agility Public Warehousing

- 11.2.2 APL Logistics

- 11.2.3 Cargo Smart

- 11.2.4 CJ Logistics Corporation

- 11.2.5 Dimerco Express

- 11.2.6 Hellmann Worldwide Logistics

- 11.2.7 Kerry Logistics Network

- 11.2.8 Pacific Tycoon Group

- 11.2.9 PIL Logistics

- 11.2.10 Samudera Shipping Line Ltd

- 11.2.11 Shippit Pty

- 11.2.12 TGL - Team Global Logistics

- 11.2.13 Toll Group

- 11.2.14 Transworld Group

- 11.2.15 Yang Ming Marine Transport

- 11.3 Emerging players

- 11.3.1 Emirates Logistics India

- 11.3.2 Flexport

- 11.3.3 Freightos

- 11.3.4 Orient Overseas Container Line

- 11.3.5 S.F. Express