PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797879

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1797879

North America Circuit Breaker Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

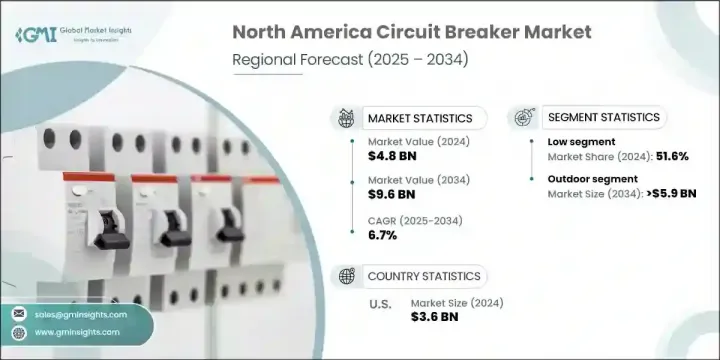

North America Circuit Breaker Market was valued at USD 4.8 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 9.6 billion by 2034. A major factor fueling market expansion is the region's aggressive push toward modernizing its electrical infrastructure to support renewable energy and digital technologies. As the power grid undergoes upgrades, there is a growing demand for advanced circuit protection systems that can handle fault isolation and dynamic load balancing with precision. These developments are reshaping the circuit breaker landscape as utilities prioritize grid resilience and smart technology adoption.

Mexico's ongoing transmission network expansion is contributing significantly to regional growth. With a national plan involving over 50 transmission projects, demand for modern protection equipment is accelerating. Meanwhile, the rise of Industry 4.0 across North America has created a surge in the adoption of intelligent circuit breakers. Automated manufacturing lines and connected equipment require immediate fault detection and remote diagnostics, boosting demand in sectors such as automotive and electronics. The expanding electric vehicle charging network is another key growth vector. With federal backing for the installation of hundreds of thousands of charging stations, the need for high-performance circuit protection in both residential and public infrastructure is stronger than ever.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.8 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 6.7% |

The low voltage circuit breakers segment held 51.6% share, and is anticipated to grow at a CAGR of 6.9% through 2034. Their adoption is rising alongside the popularity of smart homes, solar-powered systems, and energy-efficient appliances. These breakers provide safety and performance while accommodating greater power densities. In urban areas, rising installations of residential battery systems and EV chargers are prompting the need for advanced breakers that support fast switching and integrated monitoring features.

The outdoor circuit breaker installations segment accounted for a 64.4% share in 2024 and is forecasted to reach USD 5.9 billion by 2034. Their usage is widespread in utility-scale infrastructure, including transmission substations and renewable energy installations. These systems are engineered to operate reliably under harsh environmental conditions while protecting vital high-voltage components. As utility providers extend their networks into remote and rural regions, demand for durable outdoor units continues to grow.

US Circuit Breaker Market generated USD 3.6 billion in 2024 and held a 75.8% share in 2024. The transition toward a smarter and more resilient power grid is accelerating across the US, driving large-scale investments in protective devices. The integration of renewable power sources and upgrades to aging systems is fueling demand for high-performance circuit breakers to support the nation's evolving energy infrastructure.

Prominent companies in the North America Circuit Breaker Market include Hager Group, Rockwell Automation, Mitsubishi Electric Corporation, Eaton Corporation, HD Hyundai, Powell Industries, Schneider Electric, General Electric, Sensata Technologies, CG Power & Industrial Solutions, Hitachi Energy, alfanar Group, NABCO, Hubbell, Weidmuller, WEG, Toshiba International Corporation, Siemens Energy, Kirloskar Electric Company, ABB, and LS ELECTRIC. Market players are advancing their product offerings by incorporating digital intelligence, real-time monitoring, and modular designs that align with smart grid standards. Strategic collaborations with energy utilities and infrastructure developers are helping companies secure long-term supply contracts and gain access to large-scale projects. In addition, major firms are expanding their regional manufacturing and distribution capabilities to enhance customer responsiveness and supply chain agility. Innovation remains a core focus, with investments channeled into R&D for developing compact, energy-efficient, and remotely operable circuit breakers tailored to various voltage classes.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data Collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculations

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.1.1 Business trends

- 2.1.2 Voltage trends

- 2.1.3 Rated voltage trends

- 2.1.4 Rated current trends

- 2.1.5 Installation trends

- 2.1.6 End use trends

- 2.1.7 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Supply chain resilience and risk assessment

- 3.3.1 Raw material sourcing challenges

- 3.3.2 Manufacturing capacity analysis

- 3.3.3 Logistics and distribution networks

- 3.3.4 Geopolitical risk factors

- 3.4 Import export trade analysis

- 3.4.1 Key importing countries

- 3.4.2 Key exporting countries

- 3.5 Price trend analysis, (USD/Unit)

- 3.5.1 By voltage

- 3.6 Industry impact forces

- 3.6.1 Growth drivers

- 3.6.2 Industry pitfalls & challenges

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.8.1 Bargaining power of suppliers

- 3.8.2 Bargaining power of buyers

- 3.8.3 Threat of new entrants

- 3.8.4 Threat of substitutes

- 3.9 PESTEL analysis

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2024

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Voltage, 2021 - 2034 (‘000 Units & USD Million)

- 5.1 Key trends

- 5.2 Low

- 5.2.1 ACB

- 5.2.2 MCB

- 5.2.3 MCCB

- 5.2.4 Others

- 5.3 Medium

- 5.3.1 ACB

- 5.3.2 VCB

- 5.3.3 GCB

- 5.3.4 Others

- 5.4 High

- 5.4.1 ACB

- 5.4.2 GCB

- 5.4.3 VCB

- 5.4.4 OCB

Chapter 6 Market Size and Forecast, By Rated Voltage, 2021 - 2034 (‘000 Units & USD Million)

- 6.1 Key trends

- 6.2 < 500 V

- 6.3 500 V to 1 kV

- 6.4 1 to 15 kV

- 6.5 15 to 50 kV

- 6.6 50 to 70 kV

- 6.7 70 kV to 145 kV

- 6.8 145 kV to 300 kV

- 6.9 300 kV to 550 kV

- 6.10 550 kV to 800 kV

- 6.11 > 800 kV

Chapter 7 Market Size and Forecast, By Rated Current, 2021 - 2034 (‘000 Units & USD Million)

- 7.1 Key trends

- 7.2 < 500 A

- 7.3 500 to 1,500 A

- 7.4 1,500 to 2,500 A

- 7.5 2,500 to 4,500 A

- 7.6 > 4,500 A

Chapter 8 Market Size and Forecast, By Installation, 2021 - 2034 (‘000 Units & USD Million)

- 8.1 Key trends

- 8.2 Indoor

- 8.3 Outdoor

Chapter 9 Market Size and Forecast, By Application, 2021 - 2034 (‘000 Units & USD Million)

- 9.1 Key trends

- 9.2 Power distribution

- 9.3 Power transmission

Chapter 10 Market Size and Forecast, By End Use, 2021 - 2034 (‘000 Units & USD Million)

- 10.1 Key trends

- 10.2 Residential

- 10.3 Commercial

- 10.4 Industrial

- 10.5 Utility

Chapter 11 Market Size and Forecast, By Country, 2021 - 2034 (‘000 Units & USD Million)

- 11.1 Key trends

- 11.2 U.S.

- 11.3 Canada

- 11.4 Mexico

Chapter 12 Company Profiles

- 12.1 alfanar Group

- 12.2 ABB

- 12.3 CG Power & Industrial Solutions

- 12.4 Eaton Corporation

- 12.5 General Electric

- 12.6 Hager Group

- 12.7 HD Hyundai

- 12.8 Hitachi Energy

- 12.9 Hubbell

- 12.10 Kirloskar Electric Company

- 12.11 LS ELECTRIC

- 12.12 Mitsubishi Electric Corporation

- 12.13 NABCO

- 12.14 Powell Industries

- 12.15 Rockwell Automation

- 12.16 Siemens Energy

- 12.17 Sensata Technologies

- 12.18 Schneider Electric

- 12.19 Toshiba International Corporation

- 12.20 Weidmuller

- 12.21 WEG