PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801858

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801858

Europe Class 6 Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

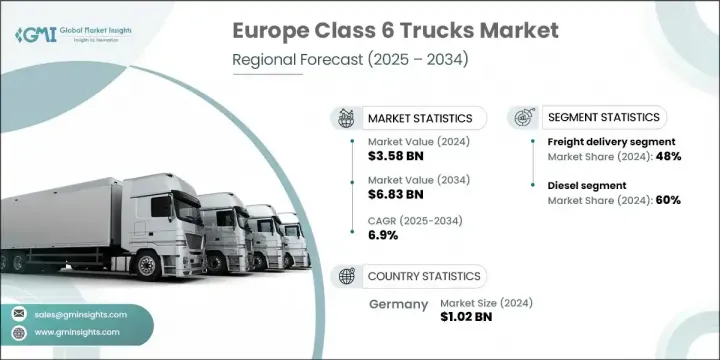

Europe Class 6 Trucks Market was valued at USD 3.58 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 6.83 billion by 2034. The market has gained traction due to growing demand for efficient regional logistics, particularly in urban zones with low-emission restrictions. While smaller light-duty vehicles offered less value and payload efficiency, the rise of e-commerce-especially following 2015-has encouraged fleet operators to shift toward mid-sized trucks. The surge in last-mile delivery during pandemic years significantly pushed adoption of Class 6 vehicles, especially in congested city centers. Demand continues to climb in suburban and urban areas where cargo needs and sustainability targets are expanding in parallel.

Regulatory enforcement has steadily increased since the introduction of Euro VI emissions standards in 2014, although early progress was slow due to minimal penalties and unclear rules. However, fleet modernization gained momentum after financial support initiatives in the post-2009 recovery phase and pandemic-related stimulus post-2020. Environmental funding and automatic emissions compliance systems are now accelerating fleet replacements across the region. Demand has also increased since 2010 from sectors like municipal services and construction, although earlier momentum had been held back due to economic slowdown and limited infrastructure investment. Today, investment in urban development and freight innovation is spurring Class 6 vehicle use in various industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.58 Billion |

| Forecast Value | $6.83 Billion |

| CAGR | 6.9% |

The diesel segment held 60% share and is forecasted to grow at a CAGR of 6% through 2034. Diesel-powered Class 6 trucks continue to lead due to favorable fuel efficiency, higher torque output, and widespread availability of service infrastructure across urban and rural locations. In areas where electric and hydrogen refueling networks are underdeveloped, diesel options remain the most viable for daily operations and heavy-duty use.

The freight delivery segment held 48% share and will grow at a CAGR of 7% between 2025 and 2034. This segment benefits from expanding demand for regional cargo logistics and same-day delivery, fueled by rapid growth in digital commerce. Class 6 trucks offer an optimal balance of maneuverability, load capacity, and fuel economy, which makes them ideal for short-haul freight operations across cities and regional corridors.

Germany Class 6 Trucks Market generated USD 1.02 billion in 2024 and held 28% share. Its leadership stems from a mature freight network, a strong logistics sector, and government initiatives promoting cleaner and more efficient transport fleets. The country also incentivizes green upgrades in medium-duty municipal and construction fleets, creating further demand for modern Class 6 vehicles that align with sustainable transport goals and urban planning objectives.

Top manufacturers active in the Europe Class 6 Trucks Market include Hyundai Motors, PACCAR, Volvo Group, Ashok Leyland, Isuzu, Ford Otosan / Ford Trucks, Scania, MAN Truck & Bus, IVECO, and Daimler Truck. Companies in the Europe Class 6 trucks market are emphasizing fleet electrification, emissions compliance, and digital integration to enhance their competitiveness. Many manufacturers are investing in R&D for hybrid and Class 6 electric platforms that meet evolving environmental standards. Strategic partnerships with local governments and logistics providers help them align with fleet modernization incentives. Expanding after-sales networks and developing modular vehicle designs are helping brands improve maintenance efficiency and customization options. Players are also leveraging telematics and predictive maintenance technologies to boost vehicle uptime for fleet operators. Additionally, some manufacturers are localizing production to meet demand fluctuations more efficiently while tapping into region-specific infrastructure support, training programs, and regulatory approvals across European markets.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fuel

- 2.2.3 Body

- 2.2.4 Horsepower

- 2.2.5 Axle

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Urban logistics expansion

- 3.2.1.2 Infrastructure modernization initiatives

- 3.2.1.3 Stricter emission regulations (Euro VI & upcoming Euro VII)

- 3.2.1.4 Public procurement reforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront cost of electric trucks

- 3.2.2.2 Limited charging and refuelling infrastructure

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of urban micro-warehousing and last-mile delivery networks

- 3.2.3.2 Advancements in battery and hydrogen fuel technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Europe

- 3.4.1.1 Emissions standards across Europe

- 3.4.1.1.1 Euro VI standards enforcement

- 3.4.1.1.2 Upcoming Euro VII regulations

- 3.4.1.1.3 Country-specific implementation timelines

- 3.4.1.1.4 CO2 emissions targets and penalties

- 3.4.1.2 Safety and vehicle standards

- 3.4.1.2.1 EU vehicle type approval procedures

- 3.4.1.2.2 Enhanced safety requirements under GSR (General Safety Regulation)

- 3.4.1.2.3 Crash testing and advanced driver assistance systems (ADAS) mandates

- 3.4.1.3 Government incentives and policies

- 3.4.1.3.1 Electrification incentives and grants

- 3.4.1.3.2 Subsidies for fleet modernization and scrappage programs

- 3.4.1.3.3 Cross-border emissions and trade regulations

- 3.4.1.1 Emissions standards across Europe

- 3.4.1 Europe

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electrification trends and adoption

- 3.7.1.1.1 BEV development

- 3.7.1.1.2 HEV solutions

- 3.7.1.1.3 Charging infrastructure developments

- 3.7.1.2 Alternative fuel technologies

- 3.7.1.2.1 Compressed natural gas (CNG) and liquefied natural gas (LNG)

- 3.7.1.2.2 Hydrogen fuel cell technology

- 3.7.1.3 Autonomous and Connected Vehicle Features

- 3.7.1.3.1 Advanced driver assistance systems (ADAS)

- 3.7.1.3.2 Fleet management and telematics

- 3.7.1.3.3 Predictive maintenance technologies

- 3.7.1.4 Emissions control and environmental technologies

- 3.7.1.4.1 Diesel particulate filter (DPF) technologies

- 3.7.1.4.2 Selective catalytic reduction (SCR) systems

- 3.7.1.1 Electrification trends and adoption

- 3.7.2 Emerging technologies

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.9.3.1 Europe statistics by country

- 3.9.3.2 Import dependency analysis

- 3.9.3.3 Trade balance assessment

- 3.9.3.4 Key export destinations outside Europe

- 3.9.3.5 Intra-regional trade flow

- 3.10 Cost breakdown analysis

- 3.10.1 Manufacturing cost components

- 3.10.1.1 Raw materials and components

- 3.10.1.2 Labor costs

- 3.10.1.3 Research and development

- 3.10.1.4 Marketing and distribution

- 3.10.1.5 Overhead and administrative

- 3.10.2 Total cost of ownership (TCO) analysis

- 3.10.3 Operating cost comparison by fuel

- 3.10.4 Maintenance and service cost analysis

- 3.10.1 Manufacturing cost components

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Market penetration and adoption rates

- 3.13.1 Market penetration by country

- 3.13.2 Electric vehicle adoption rates

- 3.13.3 Technology adoption curves

- 3.13.4 Fleet modernization trends

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Western Europe

- 4.2.2 Eastern Europe

- 4.2.3 Northern Europe

- 4.2.4 Southern Europe

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, units)

- 5.1 Key trends

- 5.2 Diesel

- 5.3 Natural gas

- 5.4 Hybrid electric

- 5.5 Zero-emission vehicles

Chapter 6 Market Estimates & Forecast, By Body, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Box

- 6.3 Dump

- 6.4 Beverage

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Horsepower, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 200-300 HP

- 7.3 300-400 HP

Chapter 8 Market Estimates & Forecast, By Axle, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 4X2

- 8.3 6X4

- 8.4 6X6

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Freight delivery

- 9.3 Utility services

- 9.4 Construction & mining

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Western Europe

- 10.2.1 Austria

- 10.2.2 Belgium

- 10.2.3 France

- 10.2.4 Germany

- 10.2.5 Ireland

- 10.2.6 Luxembourg

- 10.2.7 Monaco

- 10.2.8 Netherlands

- 10.2.9 Switzerland

- 10.2.10 United Kingdom

- 10.3 Eastern Europe

- 10.3.1 Bulgaria

- 10.3.2 Croatia

- 10.3.3 Czech Republic

- 10.3.4 Hungary

- 10.3.5 Poland

- 10.3.6 Romania

- 10.3.7 Serbia

- 10.3.8 Slovakia

- 10.3.9 Slovenia

- 10.3.10 Ukraine

- 10.4 Northern Europe

- 10.4.1 Denmark

- 10.4.2 Estonia

- 10.4.3 Finland

- 10.4.4 Iceland

- 10.4.5 Latvia

- 10.4.6 Lithuania

- 10.4.7 Norway

- 10.4.8 Sweden

- 10.5 Southern Europe

- 10.5.1 Albania

- 10.5.2 Greece

- 10.5.3 Italy

- 10.5.4 Portugal

- 10.5.5 Spain

- 10.5.6 Turkey

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Allison Transmission

- 11.1.2 Ashok Leyland

- 11.1.3 Bosch Mobility

- 11.1.4 Bucher Municipal

- 11.1.5 Cargotec Corporation

- 11.1.6 Daimler Truck

- 11.1.7 Ford Otosan / Ford Trucks

- 11.1.8 FUSO

- 11.1.9 Hyundai Motor

- 11.1.10 Isuzu

- 11.1.11 IVECO

- 11.1.12 Knorr-Bremse AG / WABCO

- 11.1.13 MAN Truck & Bus

- 11.1.14 Nikola

- 11.1.15 Nissan

- 11.1.16 PACCAR

- 11.1.17 Scania

- 11.1.18 Tata Motors

- 11.1.19 Volvo Group

- 11.1.20 ZF Friedrichshafen

- 11.2 Regional players

- 11.2.1 FAUN Umwelt Technik GmbH

- 11.2.2 GAZ Group

- 11.2.3 Kamaz

- 11.2.4 Meiller-Kipper GmbH

- 11.2.5 Hyundai Motors

- 11.2.6 Schwarz muller Group

- 11.2.7 Terberg Group

- 11.2.8 Tevva Motors

- 11.2.9 TVS Interfleet