PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801877

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1801877

Energy Dense Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

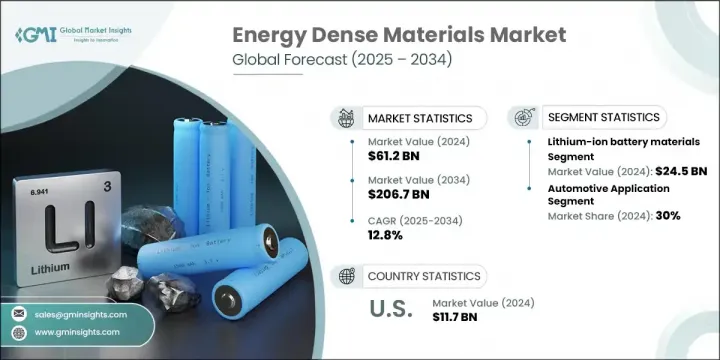

The Global Energy Dense Materials Market was valued at USD 61.2 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 206.7 billion by 2034. This market is experiencing strong momentum due to the increasing urgency around carbon reduction and the shift toward more sustainable, electrified energy systems. As renewable energy continues to gain traction in power generation, the demand for compact and highly efficient energy storage solutions is becoming more critical. Energy dense materials support this transition by ensuring grid stability, balancing supply during peak demand, and improving the consistency of power delivery from intermittent sources. Their importance is rising across various sectors as the global appetite for efficient, lightweight, and high-capacity energy storage continues to grow.

The rise of electric mobility is one of the primary contributors to market growth. As electric vehicles scale quickly across global markets, the need for batteries that deliver longer range, faster charging, and reduced weight becomes vital. Energy dense materials also serve an important role in aerospace propulsion systems for electric aircraft and drones, where maximizing energy per unit of mass results in longer flight duration and greater payload capabilities, ultimately driving innovation across air transport technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $61.2 Billion |

| Forecast Value | $206.7 Billion |

| CAGR | 12.8% |

In 2024, the lithium-ion battery materials segment generated USD 24.5 billion. Their widespread use is driven by their superior energy density relative to other options such as fuel cell materials, supercapacitors, and solid-state batteries. Lithium-ion batteries store significant energy in compact, lightweight formats, making them the go-to solution for portable electronics, electric vehicles, and large-scale energy storage systems. Their strong power output, extended cycle life, and stable performance have made them a foundational technology in modern energy storage and have supported fast adoption across industries ranging from consumer electronics to utility-scale grid storage.

The automotive applications segment held the largest share in 2024, accounting for 30% share. These applications are at the heart of energy dense material innovation, driven by the rising need for vehicles that can travel further, charge quicker, and match traditional engine performance. Battery technologies delivering greater energy density per unit of space and weight help address consumer range concerns and support widespread EV adoption. As the automotive industry continues to expand, it remains a key force behind the market's growth.

U.S. Energy Dense Materials Market reached USD 11.7 billion in 2024 and is forecasted to grow at a CAGR of 13% through 2034. With steady economic expansion, increased energy needs, and industrial growth, the U.S. has seen rising demand for efficient batteries, magnets, and fuel cell components. Energy dense materials are helping industries optimize energy use, reduce costs, and improve overall system performance. Their role in energy storage and conversion across sectors continues to make them essential for building a more resilient and efficient energy infrastructure.

Key companies operating in the Global Energy Dense Materials Market include LG Energy Solution, Panasonic Corporation, Samsung SDI Co., Ltd., Tesla, Inc., and Contemporary Amperex Technology Co. Limited (CATL). To strengthen their foothold in the global energy dense materials landscape, leading companies are focusing on several strategic priorities. These include aggressive investment in R&D for advanced chemistries that improve energy density, safety, and lifecycle. Companies are also scaling up production capacities to meet rising EV and grid demand, particularly in key growth regions. Strategic alliances with automakers and energy providers are helping secure long-term contracts. Additionally, firms are diversifying product portfolios to include next-gen materials like solid-state and lithium-sulfur technologies, while optimizing their global supply chains for cost efficiency and stability.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material type

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.2.5 Technology

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Million) (Tons)

- 5.1 Key trends

- 5.2 Lithium-ion battery materials

- 5.2.1 Cathode materials (LFP, NMC, NCA, LCO)

- 5.2.2 Anode materials (graphite, silicon, lithium metal)

- 5.2.3 Electrolyte materials

- 5.2.4 Separator materials

- 5.3 Solid-state battery materials

- 5.3.1 Solid electrolytes (oxide, sulfide, polymer)

- 5.3.2 Interface materials

- 5.3.3 Advanced electrode materials

- 5.4 Supercapacitor materials

- 5.4.1 Electrode materials (carbon-based, metal oxides)

- 5.4.2 Electrolyte solutions

- 5.4.3 Separator materials

- 5.5 Advanced carbon materials

- 5.5.1 Graphene and derivatives

- 5.5.2 Carbon nanotubes

- 5.5.3 Carbon fiber composites

- 5.6 Energetic materials

- 5.6.1 High energy density compounds

- 5.6.2 Propellant materials

- 5.6.3 Explosive materials

- 5.7 Fuel cell materials

- 5.7.1 Catalyst materials

- 5.7.2 Membrane materials

- 5.7.3 Electrode materials

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Million) (Tons)

- 6.1 Key trends

- 6.2 Automotive applications

- 6.2.1 Electric vehicles (BEV, PHEV, HEV)

- 6.2.2 Automotive electronics

- 6.2.3 Start-stop systems

- 6.3 Consumer electronics

- 6.3.1 Smartphones and tablets

- 6.3.2 Laptops and wearables

- 6.3.3 Power banks and portable devices

- 6.4 Energy storage systems

- 6.4.1 Grid-scale storage

- 6.4.2 Residential energy storage

- 6.4.3 Commercial and industrial storage

- 6.5 Aerospace and defense

- 6.5.1 Aircraft and spacecraft applications

- 6.5.2 Military and defense systems

- 6.5.3 Unmanned vehicles and drones

- 6.6 Industrial applications

- 6.6.1 Material handling equipment

- 6.6.2 Backup power systems

- 6.6.3 Telecommunications infrastructure

- 6.7 Medical and healthcare

- 6.7.1 Implantable devices

- 6.7.2 Portable medical equipment

- 6.7.3 Emergency medical systems

Chapter 7 Market Size and Forecast, By Technology, 2021-2034 (USD Million) (Tons)

- 7.1 Key trends

- 7.2 Battery technologies

- 7.2.1 Lithium-ion batteries

- 7.2.2 Solid-state batteries

- 7.2.3 Sodium-ion batteries

- 7.2.4 Metal-air batteries

- 7.3 Capacitor technologies

- 7.3.1 Supercapacitors/ultracapacitors

- 7.3.2 Hybrid capacitors

- 7.3.3 Ceramic capacitors

- 7.4 Fuel cell technologies

- 7.4.1 Proton exchange membrane (PEM)

- 7.4.2 Solid oxide fuel cells (SOFC)

- 7.4.3 Alkaline fuel cells

- 7.5 Energy harvesting technologies

- 7.5.1 Thermoelectric materials

- 7.5.2 Piezoelectric materials

- 7.5.3 Photovoltaic materials

Chapter 8 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Million) (Tons)

- 8.1 Key trends

- 8.2 Automotive industry

- 8.3 Electronics and semiconductors

- 8.4 Energy and utilities

- 8.5 Aerospace and defense

- 8.6 Healthcare and medical devices

- 8.7 Industrial manufacturing

- 8.8 Telecommunications

- 8.9 Marine and transportation

Chapter 9 Market Size and Forecast, By Region, 2021-2034 (USD Million) (Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Tesla

- 10.2 Panasonic Corporation

- 10.3 Samsung SDI

- 10.4 LG Energy Solution

- 10.5 Contemporary Amperex Technology

- 10.6 BYD Company Limited

- 10.7 QuantumScape Corporation

- 10.8 Solid Power

- 10.9 Sila Nanotechnologies

- 10.10 Group14 Technologies

- 10.11 Wildcat Discovery Technologies

- 10.12 Amprius Technologies

- 10.13 Enovix Corporation

- 10.14 Ion Storage Systems

- 10.15 Ampcera

- 10.16 Sion Power Corporation

- 10.17 Oxis Energy