PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833423

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833423

U.S. Point-of-care CT Imaging Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

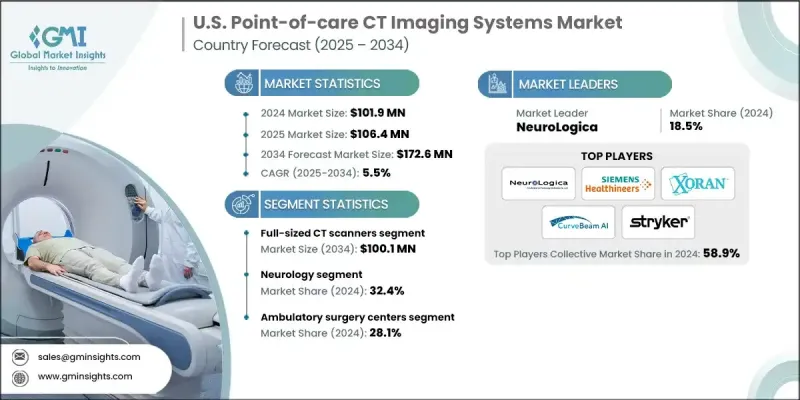

The U.S. Point-of-care CT Imaging Systems Market was valued at USD 101.9 million in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 172.6 million by 2034.

Healthcare professionals are under growing pressure to make timely clinical decisions, especially in emergency departments, intensive care units (ICUs), and trauma centers, where every second counts. Traditional imaging workflows often involve transporting patients to centralized radiology departments, which can delay diagnosis and treatment, particularly for critically ill or unstable patients.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $101.9 Million |

| Forecast Value | $172.6 Million |

| CAGR | 5.5% |

Rising Demand for Full-Sized CT Scanners

The full-sized CT scanners segment held a significant share in 2024, as point-of-care (PoC) technologies continue to evolve. While PoC CT systems are gaining traction for their mobility and immediacy, full-sized scanners still dominate when high-resolution, multi-slice imaging is required for complex diagnostics. Hospitals and large imaging centers rely on these machines for comprehensive body scans, detailed soft tissue analysis, and advanced contrast studies.

Growing Adoption in Neurology

The neurology segment generated a substantial share in 2024, as rapid brain imaging becomes critical in emergencies and intensive care settings. Neurological emergencies such as stroke, traumatic brain injury, and hemorrhage require immediate imaging to guide treatment decisions. PoC CT systems are particularly valuable here, allowing for bedside scans that eliminate delays associated with patient transport to radiology departments. This capability significantly reduces door-to-scan times, improving clinical outcomes and supporting time-sensitive protocols.

Ambulatory Surgery Centers to Gain Traction

The ambulatory surgery centers (ASCs) segment held a robust share in 2024, driven by the ongoing shift from inpatient to outpatient care. ASCs prioritize efficiency, cost control, and quick patient turnaround-making compact, easy-to-deploy imaging solutions particularly attractive. Unlike hospitals, these centers often have limited space and staff, which makes full-sized CT systems less practical. PoC CT devices offer the flexibility to perform on-site imaging without major facility modifications or operational disruptions.

Major players in the U.S. Point-of-care CT imaging systems market are SOREDEX, NeuroLogica, CurveBeam, Siemens Healthineers, Xoran Technologies, Epica International, Carestream Dental, and Stryker.

To strengthen their foothold in the U.S. point-of-care CT imaging systems market, leading companies are pursuing innovation-driven strategies focused on miniaturization, automation, and connectivity. R&D investment is being funneled into developing systems that offer diagnostic-grade imaging with smaller footprints, lower radiation doses, and user-friendly interfaces. Companies form partnerships with hospitals and academic institutions to validate clinical applications and accelerate adoption. Beyond product design, expansion of after-sales service networks and operator training programs is helping boost confidence among care providers.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing number of chronic health issues

- 3.2.1.2 Rising aging population

- 3.2.1.3 Increasing emphasis on early diagnosis and treatment

- 3.2.1.4 Technological advancements in imaging system

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High equipment cost

- 3.2.2.2 Regulatory and reimbursement barriers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into rural and remote areas

- 3.2.3.2 Integration with AI and telemedicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Compact CT scanners

- 5.3 Full-sized CT scanners

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Neurology

- 6.3 Respiratory

- 6.4 Musculoskeletal

- 6.5 ENT

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgery centers

- 7.4 Clinics

- 7.5 Other end use

Chapter 8 Company Profiles

- 8.1 Carestream Dental

- 8.2 CurveBeam

- 8.3 Epica International

- 8.4 NeuroLogica

- 8.5 Siemens Healthineers

- 8.6 SOREDEX

- 8.7 Stryker

- 8.8 Xoran Technologies