PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833662

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1833662

Railway Signaling System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

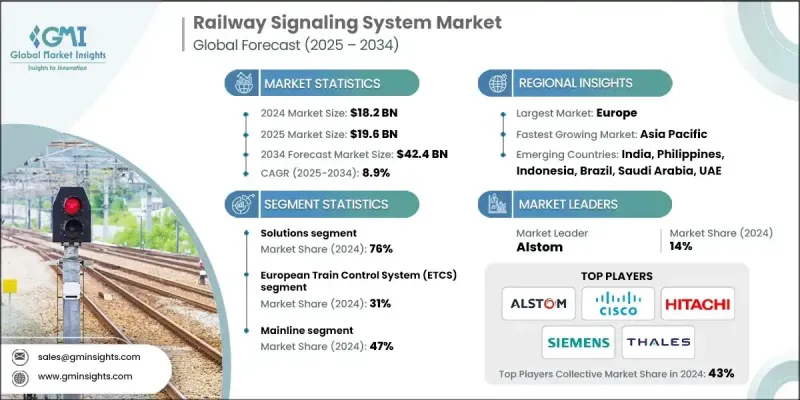

The Global Railway Signaling System Market was valued at USD 18.2 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 42.4 billion by 2034.

Governments and private operators worldwide are investing heavily in upgrading aging rail networks. This includes the deployment of modern signaling systems to improve safety, operational efficiency, and capacity across both passenger and freight corridors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $18.2 Billion |

| Forecast Value | $42.4 Billion |

| CAGR | 8.9% |

Rising Demand for Solutions Segment

The solutions segment held a significant share in 2024, driven by the growing need for real-time control, automation, and system-wide safety upgrades. These solutions typically include interlocking systems, centralized traffic control, and communication-based train control (CBTC) software, which enable operators to manage traffic flows efficiently and securely.

European Train Control System (ETCS) to Gain Traction

European train control system (ETCS) segment held a sizeable share in 2024. As part of the broader ERTMS (European Rail Traffic Management System), ETCS enables standardized signaling and control systems across member states, improving safety, speed regulation, and operational efficiency. The segment is gaining momentum with widespread adoption under EU mandates, especially in high-speed rail and international freight corridors.

Increasing Adoption in Mainline

The mainline segment witnessed noticeable growth in 2024, backed by high-speed, long-distance, and intercity rail operations. These systems require robust signaling infrastructure to handle large volumes of traffic, variable train speeds, and long track lengths. As countries across Europe upgrade their core rail networks, the demand for advanced mainline signaling solutions such as centralized traffic control and remote diagnostics continues to rise.

Europe to Emerge as a Propelling Region

Europe railway signaling system market is poised to grow at a notable CAGR during 2025-2034. Driven by the European Union's push for interoperable, sustainable rail networks, the region is witnessing accelerated investments in high-speed rail, smart mobility, and cross-border freight corridors. Market growth is supported by government grants, digital rail initiatives, and strong public-private collaboration. Leading companies are pursuing localization strategies, partnering with national rail authorities, and developing region-specific solutions that align with EU regulations.

Major players involved in the railway signaling system market are GEAR International, Thales, Nokia, Cisco Systems, Hitachi, Alstom, Huawei Technologies, General Electric, Siemens, and Belden.

To maintain a competitive edge in the railway signaling system market, leading companies are prioritizing technology innovation, strategic partnerships, and geographic expansion. Many are heavily investing in R&D to develop digital signaling platforms, including cloud-based control systems, predictive maintenance tools, and AI-enabled automation. Collaborations with national rail operators, transport ministries, and infrastructure developers are helping firms secure large-scale public contracts, especially for high-speed rail and metro projects. By focusing on modular designs and next-generation technologies like digital twins and automated signaling platforms, these players are reinforcing their foothold across both Western and Eastern Europe.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Offering

- 2.2.3 Technology

- 2.2.4 Train

- 2.2.5 Deployment mode

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Enhanced safety and operational efficiency through advanced signaling systems.

- 3.2.1.2 Government investments in railway infrastructure modernization.

- 3.2.1.3 Adoption of cutting-edge technologies like ETCS and CBTC.

- 3.2.1.4 Increasing urbanization and rail traffic demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment and deployment costs.

- 3.2.2.2 Shortage of skilled workforce for implementation and maintenance

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with growing rail networks.

- 3.2.3.2 Integration with smart city and urban mobility initiatives.

- 3.2.3.3 Implementation of predictive maintenance using data analytics.

- 3.2.3.4 Strategic partnerships between governments, tech providers, and developers

- 3.2.1 Growth drivers

- 3.3 Regulatory landscape

- 3.3.1 North America

- 3.3.2 Europe

- 3.3.3 Asia Pacific

- 3.3.4 Latin America

- 3.3.5 Middle East & Africa

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Business Case & ROI Analysis

- 3.8.1 Total cost of ownership (TCO) modeling by technology type

- 3.8.2 Implementation cost benchmarking & budget planning

- 3.8.3 Operational savings & efficiency gains quantification

- 3.8.4 Safety ROI & risk reduction value assessment

- 3.8.5 Payback period analysis by application segment

- 3.8.6 Financing models & public-private partnership strategies

- 3.8.7 Insurance premium impact & liability considerations

- 3.8.8 Regulatory compliance cost-benefit analysis

- 3.9 Technology migration & implementation strategy

- 3.9.1 Legacy-to-digital migration pathways

- 3.9.2 Phased implementation & rollout strategies

- 3.9.3 System integration methodologies & best practices

- 3.9.4 Risk assessment & mitigation framework

- 3.9.5 Vendor selection & procurement guidelines

- 3.9.6 Project management & timeline optimization

- 3.9.7 Performance KPIs & success metrics

- 3.9.8 Quality assurance & testing protocols

- 3.9.9 Change management & stakeholder engagement

- 3.10 Cybersecurity & digital risk management

- 3.10.1 Railway signaling cybersecurity threat landscape

- 3.10.2 Attack vector analysis & vulnerability assessment

- 3.10.3 Cybersecurity framework & protection strategies

- 3.10.4 Incident response & recovery protocols

- 3.10.5 Compliance & regulatory requirements

- 3.10.6 Cybersecurity investment & budget planning

- 3.10.7 Third-party risk management

- 3.10.8 Emerging threats & future preparedness

- 3.11 Best-case scenario

- 3.12 Sustainability and environmental impact analysis

- 3.12.1 Lifecycle assessment and environmental modeling

- 3.12.2 Sustainable design and optimization

- 3.12.3 Environmental compliance and reporting

- 3.12.4 Green technology and innovation

- 3.13 Risk assessment & mitigation strategies

- 3.13.1 Technology risk analysis & management

- 3.13.2 Cybersecurity risk framework

- 3.13.3 Regulatory & compliance risk assessment

- 3.13.4 Financial & market risk evaluation

- 3.13.5 Operational risk management

- 3.13.6 Supply chain risk & resilience planning

- 3.13.7 Project implementation risk mitigation

- 3.13.8 Insurance & liability risk management

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.1.1 Solutions

- 5.1.2 Services

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Automatic Block Signaling (ABS)

- 6.3 European Train Control System (ETCS)

- 6.4 Positive Train Control (PTC)

- 6.5 Automatic Train Control (ATC)

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Train, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 High-speed rail

- 8.3 Light rail & metros

- 8.4 Freight trains

- 8.5 Conventional passenger trains

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Mainline

- 9.3 Urban

- 9.4 Freight

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Philippines

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Alstom

- 11.1.2 Bombardier Transportation

- 11.1.3 CAF

- 11.1.4 Cisco Systems

- 11.1.5 CRRC

- 11.1.6 General Electric

- 11.1.7 Hitachi

- 11.1.8 IBM

- 11.1.9 Mitsubishi Electric

- 11.1.10 Nokia

- 11.1.11 Siemens

- 11.1.12 Stadler Rail

- 11.1.13 Thales

- 11.1.14 Wabtec

- 11.2 Regional Players

- 11.2.1 Angelo

- 11.2.2 Frequentis

- 11.2.3 Indra Sistemas

- 11.2.4 Kyosan Electric Manufacturing

- 11.2.5 Straffic

- 11.3 Emerging Players

- 11.3.1 ADLINK Technology

- 11.3.2 Cylus

- 11.3.3 Fidrox

- 11.3.4 GEAR International

- 11.3.5 Huawei Technologies

- 11.3.6 Humatics

- 11.3.7 Kontron Transportation