PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876564

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1876564

China Molecular Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

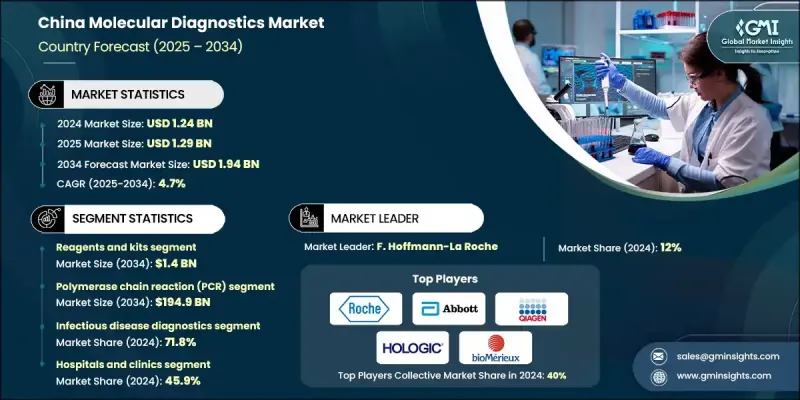

China Molecular Diagnostics Market was valued at USD 1.24 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 1.94 billion by 2034.

This consistent growth is driven by several factors, including the rising incidence of infectious and chronic diseases, increasing adoption of precision and personalized healthcare solutions, enhanced government support and healthcare expenditure, and an expanding elderly population. Molecular diagnostics involves analyzing biomarkers in the genome and proteome, such as DNA, RNA, and proteins, to detect and monitor diseases accurately. It is extensively applied for diagnosing genetic disorders, infectious conditions, and cancer due to its precision and effectiveness. Government programs promoting early disease detection and personalized treatment are accelerating the adoption of advanced diagnostic technologies. Increased healthcare funding supports hospitals and laboratories in investing in high-throughput diagnostic platforms and training skilled personnel, further boosting the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.24 Billion |

| Forecast Value | $1.94 Billion |

| CAGR | 4.7% |

The polymerase chain reaction (PCR) segment held 70.4% share in 2024. PCR is a fundamental molecular diagnostic technique that amplifies small DNA or RNA sequences, allowing highly sensitive and specific detection of genetic material from pathogens or biomarkers. Variants such as conventional PCR, real-time PCR, and digital PCR provide various levels of accuracy and precision.

The infectious disease diagnostics segment held the largest share at 71.8% in 2024. This segment focuses on detecting pathogens using molecular techniques like PCR, next-generation sequencing (NGS), and microarrays, identifying genetic material responsible for a wide range of infections. High disease prevalence in densely populated regions of China contributes to this segment's dominance.

The hospitals and clinics segment held a 45.9% share in 2024. Hospitals play a critical role due to their advanced infrastructure, skilled workforce, and access to cutting-edge diagnostic equipment. Their ability to handle complex, high-throughput diagnostic procedures makes them ideal for implementing molecular diagnostic technologies, particularly with increasing rates of chronic diseases and cancer driving patient admissions.

Key players in China Molecular Diagnostics Market include Abbott Laboratories, Biomerieux, Bio-Rad Laboratories, Illumina, Hologic, Qiagen, Sysmex Corporation, Thermo Fisher Scientific, Becton Dickinson and Company, Agilent Technologies, Siemens Healthineers, F. Hoffmann-La Roche, QuidelOrtho Corporation, Biocartis, Pilot Gene, and Rainsure Bio. Companies operating in China Molecular Diagnostics Market are focusing on strategic initiatives to strengthen their presence. They are investing in advanced diagnostic technologies and expanding their product portfolios to meet rising clinical demands. Collaborations and partnerships with local laboratories and hospitals are common to improve market penetration. Firms are also enhancing distribution networks and providing comprehensive training programs for healthcare professionals to ensure efficient adoption of molecular diagnostic tools.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of infectious and chronic diseases

- 3.2.1.2 Growing adoption of precision and personalized medicine

- 3.2.1.3 Government initiatives and healthcare spending

- 3.2.1.4 Increasing geriatric population base

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost and limited accessibility

- 3.2.2.2 Complex regulatory landscape

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of genomic research and biobanking

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Instruments

- 5.3 Reagents and kits

Chapter 6 Market Estimates and Forecast, By Technology, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Polymerase chain reaction (PCR)

- 6.3 Hybridization

- 6.4 Sequencing

- 6.5 Isothermal nucleic acid amplification technology (INAAT)

- 6.6 Microarrays

- 6.7 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Infectious disease diagnostics

- 7.2.1 COVID-19

- 7.2.2 Flu

- 7.2.3 Respiratory syncytial virus (RSV)

- 7.2.4 Tuberculosis

- 7.2.5 CT/NG

- 7.2.6 HIV

- 7.2.7 Hepatitis C

- 7.2.8 Hepatitis B

- 7.2.9 Other infectious disease diagnostics

- 7.3 Genetic disease testing

- 7.4 Oncology testing

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals and clinics

- 8.3 Diagnostic Laboratories

- 8.4 Other end use

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Agilent Technologies

- 9.3 Becton, Dickinson, and Company

- 9.4 Biocartis

- 9.5 Biomerieux

- 9.6 Bio-Rad Laboratories

- 9.7 Danaher Corporation

- 9.8 F. Hoffmann-La Roche

- 9.9 Hologic

- 9.10 Illumina

- 9.11 Qiagen

- 9.12 QuidelOrtho Corporation

- 9.13 Siemens Healthineers

- 9.14 Sysmex Corporation

- 9.15 Thermo Fisher Scientific

- 9.16 Rainsure Bio

- 9.17 Pilot Gene