PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885806

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885806

AI Data Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

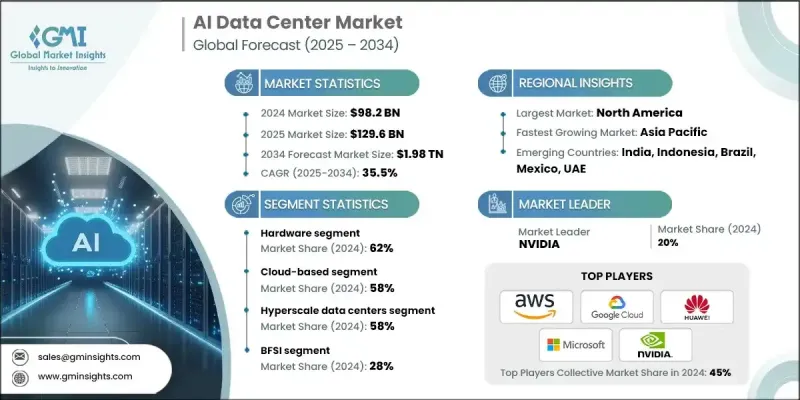

The Global AI Data Center Market was valued at USD 98.2 billion in 2024 and is estimated to grow at a CAGR of 35.5% to reach USD 1.98 trillion by 2034.

Growing adoption of generative AI and machine learning tools requires extraordinary processing power and storage capabilities, increasing reliance on data centers specifically optimized for AI workloads. These environments depend on advanced GPUs, scalable system architecture, and ultra-low-latency networking to support complex model training and inference across industries such as finance, healthcare, and retail. Big data analytics is also accelerating demand, as organizations handle massive streams of structured and unstructured information that must be processed rapidly. AI-focused facilities enable high-performance computing for real-time workloads, strengthening their role as essential infrastructure for global digital transformation. The rapid expansion of cloud computing, along with the rising number of hyperscale facilities, continues to amplify the need for AI-ready infrastructures. Providers are investing in advanced AI data platforms that offer scalable services to enterprises and developers, further increasing market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $98.2 Billion |

| Forecast Value | $1.98 Trillion |

| CAGR | 35.5% |

The hardware segment accounted for USD 61.1 billion in 2024. Growth is driven by expanding use of AI chips, GPU accelerators, advanced cooling technologies, high-density server systems, and optical networking solutions. Rising GPU energy requirements, the shift toward rack densities between 30-120 kW, and large-scale deployment strategies introduced by leading technology companies are shaping long-term capital allocation in the sector.

The cloud-based category held a 58% share in 2024 and is projected to grow at a CAGR of 35.2% from 2025 through 2034. This segment leads due to its unmatched scalability, flexible consumption options, and access to the latest AI-accelerated computing hardware without upfront investment. Hyperscale providers are making multi-billion-dollar commitments to strengthen global AI infrastructures, propelling adoption of AI-driven services and increasing demand for GPUs, TPUs, and specialized processors.

US AI Data Center Market generated USD 33.2 billion in 2024. The country maintains a leading position supported by prominent hyperscale operators and substantial investments in GPU clusters, liquid cooling, and large-scale AI-aligned builds. Federal incentives, regional tax advantages, and infrastructure funding have further solidified the United States as the most capacity-rich region for AI computing.

Key participants in the AI Data Center Market include Huawei, AWS, NVIDIA, HPE, Digital Realty, Google, Lenovo, Microsoft, Equinix, and Dell Technologies. Companies expanding their foothold in the AI data center market are focusing on infrastructure modernization, large-scale GPU deployments, and energy-efficient system design. Many firms are investing in high-density racks, integrated liquid cooling, and next-generation networking to support advanced AI workloads. Strategic partnerships with chipmakers, cloud providers, and colocation operators help accelerate capacity expansion and ensure access to cutting-edge AI hardware. Providers are also scaling global data center footprints, enhancing automation capabilities, and optimizing power utilization through renewable-energy integration. Long-term contracts with enterprises, AI-as-a-service offerings, and the buildout of specialized AI clusters further reinforce competitive positioning and market dominance.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment mode

- 2.2.4 Data center

- 2.2.5 Industry vertical

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Adoption of generative AI & machine learning

- 3.2.1.2 Growth in big data analytics

- 3.2.1.3 Cloud expansion & hyperscale deployments

- 3.2.1.4 Advancements in GPU & chip technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High capital & operational costs

- 3.2.2.2 Energy consumption & sustainability issues

- 3.2.3 Market opportunities

- 3.2.3.1 Edge AI data centers

- 3.2.3.2 Liquid cooling & green technologies

- 3.2.3.3 AI-as-a-service platforms

- 3.2.3.4 Emerging markets adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 GPU & accelerator technology evolution

- 3.7.1.2 Liquid cooling technology advancement

- 3.7.1.3 Power distribution innovation (48V Architecture, Modular UPS)

- 3.7.2 Emerging technologies

- 3.7.2.1 Software-defined infrastructure

- 3.7.2.2 Edge computing integration

- 3.7.1 Current technological trends

- 3.8 Pricing analysis

- 3.8.1 Colocation pricing trends (per kw, per rack)

- 3.8.2 Cloud AI compute pricing evolution

- 3.8.3 Energy cost impact on total cost of ownership

- 3.8.4 Cooling technology cost comparison

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.10.1 Cooling technology patents

- 3.10.2 AI chip architecture patents

- 3.10.3 Power management innovations

- 3.10.4 Data center design patents

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Carbon footprint considerations

- 3.13 Use cases

- 3.14 Best case scenario

- 3.15 Interconnection & network infrastructure analysis

- 3.15.1 Data center interconnection architecture

- 3.15.2 High-speed fabric requirements

- 3.15.3 Submarine cable investments by hyperscalers

- 3.15.4 Internet exchange point proximity & peering

- 3.15.5 Fiber backhaul availability by region

- 3.15.6. 5 g & edge network integration

- 3.15.7 Software-defined networking adoption

- 3.16 Investment & funding analysis

- 3.16.1 Hyperscale capital expenditure trends

- 3.16.2 Private equity & infrastructure fund activity

- 3.16.3 Government investment programs

- 3.16.4 Venture capital in AI infrastructure startups

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 New capacity & site announcements

- 4.8 Vendor selection criteria

- 4.9 Product & service benchmarking

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Servers

- 5.2.2 GPUs

- 5.2.3 Storage

- 5.2.4 Networking equipment

- 5.3 Software

- 5.3.1 AI frameworks

- 5.3.2 Orchestration tools

- 5.3.3 Management platforms

- 5.4 Services

- 5.4.1 Professional services

- 5.4.1.1 Deployment & Integration

- 5.4.1.2 Consulting

- 5.4.1.3 Support & maintenance

- 5.4.2 Managed services

- 5.4.1 Professional services

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Cloud-based

- 6.3 On-premises

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Hyperscale data centers

- 7.3 Enterprise data centers

- 7.4 Colocation data centers

- 7.5 Edge data centers

Chapter 8 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Government

- 8.4 Healthcare

- 8.5 IT & telecom

- 8.6 Automotive

- 8.7 Media & entertainment

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Vietnam

- 9.4.7 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global companies

- 10.1.1 AWS

- 10.1.2 Dell Technologies

- 10.1.3 Digital Realty

- 10.1.4 Equinix

- 10.1.5 Google Cloud

- 10.1.6 HPE

- 10.1.7 Huawei

- 10.1.8 Lenovo

- 10.1.9 Microsoft

- 10.1.10 NVIDIA

- 10.2 Regional players

- 10.2.1 Ascenty (Digital Realty/Brookfield)

- 10.2.2 China Telecom

- 10.2.3 Cirion Technologies

- 10.2.4 Elea Data Centers

- 10.2.5 ST Telemedia Global Data Centres (STT GDC)

- 10.2.6 Telehouse (KDDI)

- 10.2.7 TierPoint

- 10.3 Emerging players

- 10.3.1 Applied Digital

- 10.3.2 CoreWeave

- 10.3.3 Crusoe Energy

- 10.3.4 Lambda Labs

- 10.3.5 Nebius AI