PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885808

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885808

Solid-State Battery for Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

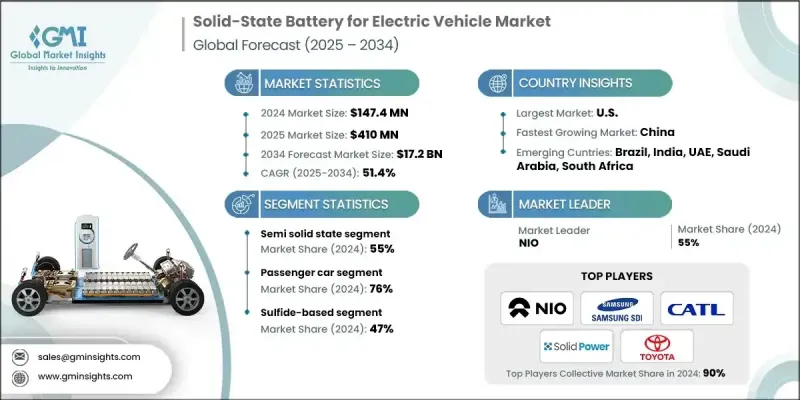

The Global Solid-State Battery for Electric Vehicle Market was valued at USD 147.4 million in 2024 and is estimated to grow at a CAGR of 51.4% to reach USD 17.2 billion by 2034.

Concerns over thermal runaway, fire hazards, and the inherent limitations of conventional liquid-electrolyte lithium-ion batteries are pushing automakers to explore safer, more stable battery chemistries. Solid-state batteries eliminate flammable electrolytes, offer superior thermal stability, and perform reliably under extreme temperatures. With governments tightening battery safety regulations and manufacturers focusing on risk mitigation, the demand for robust, crash-resistant battery packs is surging. Automakers are investing heavily in advanced battery technologies to extend driving range without adding extra weight to vehicles. Solid-state batteries provide higher energy density, thinner cell structures, and faster charging, driving pilot production lines and strategic supply partnerships. The push toward lightweight, long-range EVs is accelerating commercialization, while governments in the US, Europe, China, Japan, and South Korea are investing billions in research, development, and production, providing incentives that reduce risks for startups and established manufacturers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $147.4 Million |

| Forecast Value | $17.2 Billion |

| CAGR | 51.4% |

The semi-solid-state segment held a 55% share in 2024 and is projected to grow at a 50% CAGR from 2025 to 2034. Semi-solid-state batteries bridge conventional liquid-electrolyte lithium-ion cells with fully solid-state designs, enhancing safety and energy density while remaining compatible with current manufacturing infrastructure. This approach reduces production costs, shortens timelines, and allows automakers to introduce next-generation battery performance faster, accelerating adoption in mid-range and premium EVs.

The passenger cars segment held a 76% share in 2024 and is expected to grow at a CAGR of 51% from 2025 to 2034. Customers increasingly expect EVs to deliver extended ranges without frequent charging. Solid-state batteries enable ranges exceeding 700 to 1,000 km per charge, alleviating range anxiety and boosting consumer adoption of compact, mid-size, and premium EVs equipped with these advanced battery systems.

US Solid-State Battery for Electric Vehicle Market held an 86% share, generating USD 49.7 million in 2024. Government initiatives like the IRA and ARPA-E are driving investment in electric vehicle adoption and battery innovation, supporting large-scale research, development, and manufacturing of solid-state batteries. These programs are enabling a swift transition to safer, higher-performance EV battery technologies.

Key players in the Solid-State Battery for Electric Vehicle Market include NIO, LG Energy Solution, Solid Power, BYD, CATL, Toyota, Gotion High-Tech, Enovix, Samsung SDI, and Nissan. Companies in the Solid-State Battery for Electric Vehicle Market are strengthening their position by investing in advanced R&D to enhance energy density, durability, and safety. They are forming strategic collaborations with automakers and material suppliers, establishing pilot production lines, and scaling manufacturing capacity to meet growing demand. Geographic expansion, securing critical raw materials, and leveraging government incentives are also central strategies. Additionally, firms focus on improving battery performance through innovative designs, faster charging solutions, and compact architectures to solidify their competitive advantage in the rapidly evolving EV battery landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Material

- 2.2.3 Propulsion

- 2.2.4 Vehicle

- 2.2.5 Application Stage

- 2.2.6 Technology

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook

- 2.6 Strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Breakthroughs in high-energy-density solid electrolytes

- 3.2.1.2 Rising global demand for safer EV battery technologies

- 3.2.1.3 Heavy OEM & government investments in pilot lines

- 3.2.1.4 Shift toward long-range EVs with ultra-fast charging

- 3.2.1.5 Strategic partnerships & material innovations

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs & complex processing

- 3.2.2.2 Scalability & yield issues in gigafactories

- 3.2.2.3 Limited supply chain maturity

- 3.2.2.4 Durability issues during fast charging

- 3.2.3 Market opportunities

- 3.2.3.1 Growing global EV penetration

- 3.2.3.2 Advances in lithium-metal & silicon-anode design

- 3.2.3.3 Premium & performance EV commercialization

- 3.2.3.4 Recycling & circular economy pathways

- 3.2.4 Market Challenges

- 3.2.4.1 Technology validation & field testing requirements

- 3.2.4.2 Competing next-generation technologies

- 3.2.4.3 Oem risk aversion & conservative adoption timelines

- 3.2.4.4 Standardization & interoperability issues

- 3.2.4.5 Skilled workforce shortage for ssb manufacturing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and disruptions

- 3.5 Future market trends

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current Technologies

- 3.9.1.1 Advanced anode and cathode materials

- 3.9.1.2 Thermal management systems for heat control

- 3.9.1.3 High-energy density cells

- 3.9.1.4 Scalable manufacturing processes

- 3.9.2 Emerging Technologies

- 3.9.2.1 AI-enabled battery design & manufacturing

- 3.9.2.2 Self-forming anode technologies

- 3.9.2.3 Dual-power & multi-chemistry architectures

- 3.9.2.4 Digital twin & smart manufacturing

- 3.9.1 Current Technologies

- 3.10 Patent analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Price trends

- 3.12.1 By region

- 3.12.2 By propulsion

- 3.13 Pricing analysis and value chain economics

- 3.13.1 SSB pricing trends by material segment

- 3.13.2 Cost structure breakdown

- 3.13.3 Regional price sensitivity

- 3.14 Cost breakdown analysis

- 3.14.1 Material costs

- 3.14.2 Manufacturing & processing costs

- 3.14.3 Quality control & testing costs

- 3.14.4 Packaging & transportation costs

- 3.15 Sustainability and environmental aspects

- 3.15.1 Sustainable practices

- 3.15.2 Waste reduction strategies

- 3.15.3 Energy efficiency in production

- 3.15.4 Eco-friendly initiatives

- 3.15.5 Carbon footprint considerations

- 3.16 Global trade and import/export analysis

- 3.16.1 Import dependencies by region

- 3.16.2 Trade regulations and tariff impact

- 3.17 Product lifecycle analysis

- 3.17.1 Expected cycle life

- 3.17.2 Calendar life & degradation patterns

- 3.17.3 Performance retention over time

- 3.17.4 End-of-life performance thresholds

- 3.18 Critical industry gaps & company response strategies

- 3.18.1 Technology gaps

- 3.18.2 Manufacturing & scalability gaps

- 3.18.3 Supply chain gaps

- 3.18.4 Standardization & interoperability gaps

- 3.18.5 Market adoption gaps

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Material, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Polymer-based

- 5.3 Sulfide-based

- 5.4 Oxide-based

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 BEV

- 6.3 PHEV

- 6.4 HEV

Chapter 7 Market Estimates & Forecast, By Application Stage, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Prototype / R&D

- 7.3 Pilot-scale deployment

- 7.4 Commercial production

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units, Fleet Size)

- 8.1 Key trends

- 8.2 Semi-solid state

- 8.3 Solid state

Chapter 9 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 Hatchback

- 9.2.2 Sedan

- 9.2.3 SUV

- 9.3 Commercial vehicles

- 9.3.1 Light duty

- 9.3.2 Medium duty

- 9.3.3 Heavy duty

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Singapore

- 10.4.7 Vietnam

- 10.4.8 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 BYD Company Limited

- 11.1.2 CATL

- 11.1.3 Factorial Energy

- 11.1.4 Ganfeng Lithium

- 11.1.5 General Motors

- 11.1.6 Ilika plc

- 11.1.7 LG Energy

- 11.1.8 Panasonic Corporation

- 11.1.9 PolyPlus Battery Company

- 11.1.10 QuantumScape Corporation

- 11.1.11 SAFT

- 11.1.12 Samsung SDI

- 11.1.13 SK Innovation

- 11.1.14 Solid Power

- 11.1.15 Toyota Motor Corporation

- 11.1.16 Volkswagen Group

- 11.2 Regional players

- 11.2.1.1 Blue Solutions

- 11.2.1.2 CALB

- 11.2.1.3 EVE Energy

- 11.2.1.4 Farasis Energy

- 11.2.1.5 Gotion High-Tech

- 11.2.1.6 Hyundai Motor Group

- 11.2.1.7 Narada Power Source

- 11.2.1.8 Nissan Motor

- 11.2.1.9 ProLogium Technology

- 11.2.1.10 Sakuu Corporation

- 11.2.1.11 Sunwoda Electronic

- 11.2.1.12 Svolt Energy Technology

- 11.2.1.13 WeLion New Energy Technology

- 11.3 Emerging Players

- 11.3.1 Factorial Energy

- 11.3.2 Ilika plc

- 11.3.3 InoBat

- 11.3.4 PolyPlus Battery Company

- 11.3.5 Sakuu Corporation

- 11.3.6 WeLion New Energy Technology