PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885867

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885867

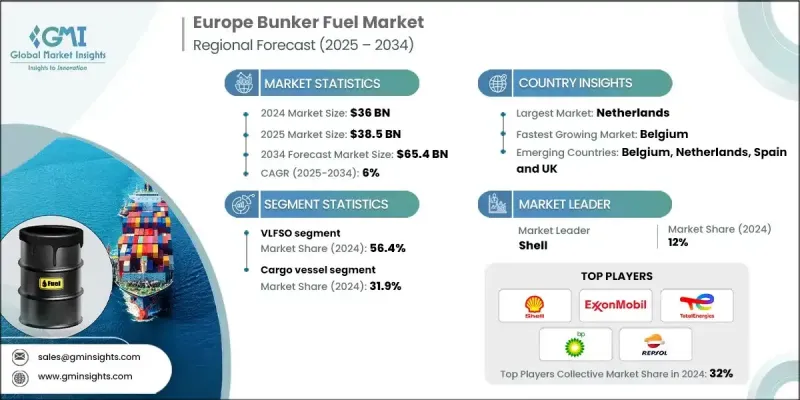

Europe Bunker Fuel Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

Europe Bunker Fuel Market was valued at USD 36 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 65.4 billion by 2034.

Growth in marine trade, stringent environmental regulations, and the ongoing shift toward cleaner fuels are shaping the market landscape. The region's extensive network of ports, shipping routes, and fleet modernization initiatives is boosting demand for high-quality bunker fuels. Governments are enforcing low-sulfur fuel mandates, prompting refiners and suppliers to develop compliant fuel blends without compromising performance. Investments in storage, blending, and bunkering infrastructure are increasing to support rising demand. Ship operators are aligning fuel procurement strategies with sustainability targets and carbon reduction objectives, while ports and energy providers are establishing reliable supply chains for alternative fuels, ensuring market stability. The combination of regulatory pressure, environmental responsibility, and fleet efficiency is driving innovation and diversification in Europe's bunker fuel sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $36 Billion |

| Forecast Value | $65.4 Billion |

| CAGR | 6% |

In 2024, the VLSFO segment held a 56.4% share and is expected to grow at a CAGR of 7% through 2034. The demand for very low sulfur fuel oil is fueled by global efforts to reduce sulfur emissions, improve air quality, and maintain compatibility with existing marine engines. Shipowners and operators are increasingly focused on complying with international regulations while adopting fuel efficiency measures. Investments in digital bunkering platforms are streamlining VLSFO procurement, delivery, and inventory management, further boosting market adoption.

The cargo vessel segment accounted for a 31.9% share in 2024 and is projected to grow at a CAGR of 5.4% through 2034. Bulk carriers, general cargo ships, and specialized freight vessels are core drivers of bunker fuel consumption due to long-haul operations and retrofitting initiatives. Modernization of fleets to meet emission regulations, coupled with LNG-ready designs and fuel efficiency enhancements, is increasing fuel demand, influencing overall market dynamics in Europe.

Germany Bunker Fuel Market held 6% share in 2024, generating USD 2.1 billion. Rising demand for bunker fuel, combined with port infrastructure expansion along major shipping routes, is driving growth. German ship operators are gradually transitioning to low-emission fuels, prompting refiners and distributors to upgrade production facilities, storage systems, and distribution networks, thereby supporting industry expansion.

Key players in the Europe bunker fuel industry include Chevron Corporation, Vitol Bunkers, Shell, TotalEnergies, BP p.l.c., SHV Energy, BUNKER HOLDING, Axpo Holding AG, Innospec, Ganor, Dan-Bunkering, Exxon Mobil, GAC, Hans Rinck Brennstoffe GmbH & Co. KG, Malik Energy, Gasum Ltd, Minerva Bunkering, Petrobras, Repsol, Stena Metall, and TFG Marine Pte. Ltd. Companies in the Europe Bunker Fuel Market are adopting multiple strategies to strengthen their market position. They are investing in cleaner fuel technologies, including LNG and low-sulfur blends, to comply with strict environmental regulations. Strategic partnerships with ports and shipping operators ensure a consistent supply and broaden customer reach. Firms are also expanding storage, blending, and distribution infrastructure to improve operational efficiency. Integration of digital platforms enhances fuel procurement, inventory tracking, and delivery management. Marketing campaigns emphasize environmental compliance and fuel quality.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Vessel type trends

- 2.5 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digital transformation with IoT technologies

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2024

- 4.2.1 Germany

- 4.2.2 UK

- 4.2.3 Netherlands

- 4.2.4 Spain

- 4.2.5 Belgium

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034, (USD Billion)

- 5.1 Key trends

- 5.2 HSFO

- 5.3 VLSFO

- 5.4 MGO

- 5.5 LNG

- 5.6 Others

Chapter 6 Market Size and Forecast, By Vessel Type, 2021 - 2034, (USD Billion)

- 6.1 Key trends

- 6.2 Container ships

- 6.3 Tankers

- 6.4 Cargo vessels

- 6.5 Cruise ships

- 6.6 Others

Chapter 7 Market Size and Forecast, By Country, 2021 - 2034, (USD Billion)

- 7.1 Key trends

- 7.2 Germany

- 7.3 UK

- 7.4 Netherlands

- 7.5 Spain

- 7.6 Belgium

Chapter 8 Company Profiles

- 8.1 Axpo Holding AG

- 8.2 BP p.l.c.

- 8.3 BUNKER HOLDING

- 8.4 Chevron Corporation

- 8.5 Dan-Bunkering

- 8.6 Exxon Mobil

- 8.7 GAC

- 8.8 Ganor

- 8.9 Gasum Ltd

- 8.10 Hans Rinck Brennstoffe GmbH &. Co. KG

- 8.11 Innospec

- 8.12 Malik Energy

- 8.13 Minerva Bunkering

- 8.14 Petrobras

- 8.15 Repsol

- 8.16 Shell

- 8.17 SHV Energy

- 8.18 Stena Metall

- 8.19 TFG Marine Pte. Ltd.

- 8.20 TotalEnergies

- 8.21 Vitol Bunkers