PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885885

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1885885

Procurement Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

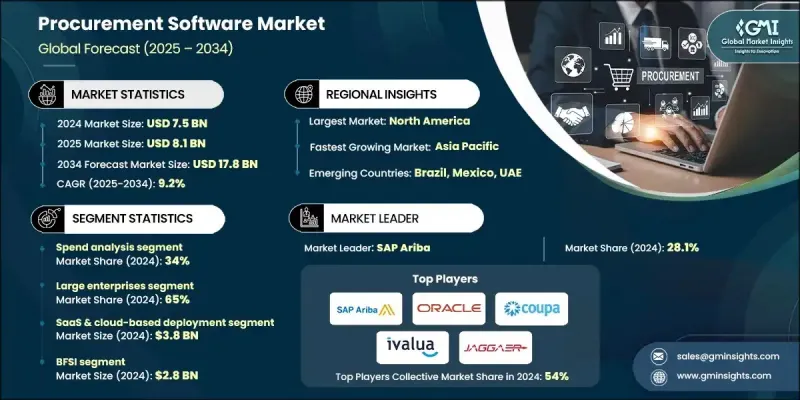

The Global Procurement Software Market was valued at USD 7.5 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 17.8 billion by 2034.

Demand for procurement technology continues to rise as organizations prioritize digital-first operations, stronger cost control, and improved supply chain transparency across sectors, including manufacturing, BFSI, healthcare, retail, and government. Enterprises are accelerating the adoption of cloud-based procurement ecosystems to streamline sourcing activities, strengthen compliance, and automate spend management. As operational efficiency and governance expectations increase, procurement teams are shifting toward integrated digital platforms that enhance collaboration with suppliers and optimize contract lifecycles. The market's expansion is also supported by the widespread need to reduce manual processes, centralize procurement data, and improve responsiveness in global supply networks.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $17.8 Billion |

| CAGR | 9.2% |

Advanced technologies are reshaping procurement workflows through AI-driven analytics, RPA-enabled automation, and IoT-based supply chain monitoring. These capabilities enable real-time spend insights, predictive forecasting, and automated risk evaluation across supplier networks. Machine learning models, digital twins, and dynamic supplier performance dashboards help organizations make faster, data-backed decisions while elevating cost savings and operational agility. Adoption of cloud e-sourcing solutions, digital contract management, and sophisticated supplier relationship management tools further strengthens accuracy, compliance, and workflow efficiency throughout procurement operations.

The spend analysis held a 34% share in 2024 and is anticipated to grow at a CAGR of 9% through 2034. This segment is critical for achieving financial transparency and analytical accuracy. Companies relying on AI-enhanced spend intelligence, structured data classification, and predictive cost modeling can reduce unmanaged spending and uncover new efficiency opportunities. These tools provide continuous visibility into procurement performance, surpassing the capabilities of manual reporting methods.

The large enterprises held a 65% share in 2024 and will grow at a CAGR of 9.5% during 2025-2034. Their leadership stems from the need for scalable, interconnected procurement systems that support global operations. These organizations depend on robust tools for enterprise-wide spend tracking, automated supplier assessments, and multi-region sourcing. Strong investment in AI-led procurement platforms and cloud-integrated suites continues to reinforce their dominant position.

United States Procurement Software Market held an 88% share and generated USD 2.2 billion in 2024. The country's strong technological foundation, large concentration of procurement software providers, and rapidly advancing digital adoption among enterprises support its leading share. U.S. organizations are increasingly relying on cloud-native platforms, AI-enabled supplier analyses, and workflow automation technologies to enhance sourcing accuracy and governance. Government-driven initiatives promoting secure digital procurement and enhanced transparency further boost adoption across public and private sectors.

Key Procurement Software Market participants include Workday, Synertrade, SAP Ariba, Coupa, Oracle, GEP, Basware, Jaggaer, Ivalua, and Zycus. Companies in the Procurement Software Market are executing several strategies to reinforce their market position. Many are expanding cloud-native architectures and deploying AI-driven analytics to enhance speed, accuracy, and decision intelligence across procurement cycles. Vendors are investing heavily in automation technologies, including RPA and machine learning, to streamline repetitive tasks and improve user efficiency. Strategic partnerships with ERP providers, financial software platforms, and supply chain technology firms help broaden integration capabilities and create unified digital ecosystems. Firms are also prioritizing enhanced data security, regulatory compliance features, and customizable procurement modules to meet diverse enterprise needs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Software module

- 2.2.3 Organization size

- 2.2.4 Deployment model

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Digital transformation in procurement

- 3.2.1.2 AI & analytics integration

- 3.2.1.3 Regulatory compliance & risk management

- 3.2.1.4 Cost optimization & efficiency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs & complexity

- 3.2.2.2 Data security & privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 SME adoption growth

- 3.2.3.2 Sustainable & green procurement

- 3.2.3.3 AI and machine learning integration

- 3.2.3.4 Supplier collaboration and risk management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Artificial intelligence & machine learning in procurement

- 3.4.2 Generative ai applications & transformational impact

- 3.4.3 Robotic process automation (RPA) integration

- 3.4.4 Blockchain for supplier verification & traceability

- 3.4.5 Internet of things (IOT) for inventory & asset tracking

- 3.4.6 Advanced analytics & predictive intelligence

- 3.4.7 Natural language processing (NLP) for contract analysis

- 3.4.8 Computer vision & OCR for invoice processing

- 3.4.9 Digital twins for supply chain simulation

- 3.4.10 Edge computing & distributed procurement

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Technology evolution timeline & milestones

- 3.7.2 Performance improvement projections by technology

- 3.7.3 Cost reduction roadmap & economic targets

- 3.7.4 Manufacturing scale-up timeline & capacity planning

- 3.7.5 Emerging technology integration & convergence

- 3.7.6 Market penetration scenarios & adoption curves

- 3.7.7 Disruptive technology threats & market impact

- 3.7.8 Long-term market opportunities & strategic vision

- 3.7.9 Technology transfer & commercialization pathways

- 3.7.10 Innovation ecosystem & collaboration networks

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.12 Best case scenarios

- 3.13 Government & public sector e-procurement focus

- 3.13.1 Government & public sector e-procurement focus

- 3.13.2 Global e-procurement reform initiatives

- 3.13.3 India gem (government e-marketplace)

- 3.13.4 France E-procurement & e-invoicing reforms

- 3.13.5 European union e-procurement initiatives

- 3.13.6 U.S. federal E-procurement modernization

- 3.13.7 Asia pacific E-government procurement

- 3.13.8 Latin America & emerging markets

- 3.13.9 Ongoing major public procurement projects

- 3.13.10 Public sector digitalization roadmaps & investment

- 3.14 Emerging delivery models & architectural evolution

- 3.14.1 Software-as-a-service (SAAS) Evolution

- 3.14.2 Platform-as-a-service (PAAS) for Procurement

- 3.14.3 Managed procurement services (MPS)

- 3.14.4 API-first & headless procurement architecture

- 3.14.5 Procurement marketplace evolution

- 3.14.6 Embedded procurement & procurement-as-a-service

- 3.14.7 Modular & composable procurement suites

- 3.15 Supply Chain & Delivery Model Analysis

- 3.15.1 SaaS subscription models

- 3.15.2 Implementation & professional services

- 3.15.3 Managed services & BPO integration

- 3.15.4 Partner ecosystem & channel strategy

- 3.15.5 Direct vs indirect sales models

- 3.15.6 Customer success & retention strategies

- 3.16 User Adoption & Change Management

- 3.16.1 User adoption rates & challenges

- 3.16.2 Change management best practices

- 3.16.3 Training & enablement requirements

- 3.16.4 Casual buyer vs power user experience

- 3.16.5 Mobile adoption & field procurement

- 3.16.6 Gamification & user engagement strategies

- 3.16.7 Executive sponsorship & stakeholder alignment

- 3.17 Buyer Journey & Decision-Making Process

- 3.17.1 Procurement software evaluation criteria

- 3.17.2 RFP & vendor selection process

- 3.17.3 Proof-of-concept & pilot programs

- 3.17.4 Stakeholder alignment & consensus building

- 3.17.5 Build vs buy vs partner decisions

- 3.17.6 Vendor evaluation scorecards & frameworks

- 3.17.7 Contract negotiation & commercial terms

- 3.18 Procurement maturity models & digital transformation roadmaps

- 3.18.1 Procurement maturity assessment frameworks

- 3.18.2 Digital procurement transformation stages

- 3.18.3 Roadmap development & prioritization

- 3.18.4 Quick wins vs strategic initiatives

- 3.18.5 Capability building & organizational readiness

- 3.18.6 Transformation KPIS & success metrics

- 3.19 Security, Compliance & Risk Management

- 3.19.1 Cybersecurity threats & mitigation strategies

- 3.19.2 Data security & encryption standards

- 3.19.3 Access control & identity management

- 3.19.4 Audit trails & compliance reporting

- 3.19.5 Vendor risk management & third-party security

- 3.19.6 Disaster recovery & business continuity planning

- 3.19.7 Zero trust architecture for procurement

- 3.19.8 Supply chain cyber risk management

- 3.20 Performance Benchmarks & SLAs

- 3.20.1 System uptime & availability standards

- 3.20.2 Response time & performance metrics

- 3.20.3 Support & service level agreements

- 3.20.4 Vendor performance scorecards

- 3.20.5 Industry benchmark comparisons

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Software Module, 2021 - 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Spend analysis

- 5.3 E-sourcing

- 5.4 E-procurement

- 5.5 Contract management

- 5.6 Supplier management

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Organization Size, 2021 - 2034 ($ Bn)

- 6.1 Key trends

- 6.2 Large Enterprises

- 6.3 SME

Chapter 7 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($ Bn)

- 7.1 Key trends

- 7.2 SaaS & cloud-based deployment

- 7.3 Hybrid

- 7.4 On-premises

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($ Bn)

- 8.1 Key trends

- 8.2 BFSI

- 8.3 Government & public sector

- 8.4 Manufacturing

- 8.5 Healthcare & life sciences

- 8.6 Retail & consumer goods

- 8.7 Telecommunications

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Belgium

- 9.3.7 Netherlands

- 9.3.8 Sweden

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 Singapore

- 9.4.6 South Korea

- 9.4.7 Vietnam

- 9.4.8 Indonesia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Global Player

- 10.1.1 Basware

- 10.1.2 Coupa Software

- 10.1.3 GEP

- 10.1.4 Ivalua

- 10.1.5 JAGGAER

- 10.1.6 Oracle

- 10.1.7 SAP Ariba

- 10.1.8 Tradeshift

- 10.1.9 Workday

- 10.1.10 Zycus

- 10.2 Regional Player

- 10.2.1 Anvil

- 10.2.2 Beroe

- 10.2.3 Cirtuo

- 10.2.4 Esker

- 10.2.5 Planergy

- 10.2.6 Proactis

- 10.2.7 Sievo

- 10.2.8 SpendHQ

- 10.2.9 Synertrade

- 10.2.10 Zip

- 10.3 Emerging Players

- 10.3.1 Corcentric

- 10.3.2 Kodiak Hub

- 10.3.3 Medius

- 10.3.4 Raindrop

- 10.3.5 ZHENYUN