PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892708

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892708

Aircraft Heat Exchanger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

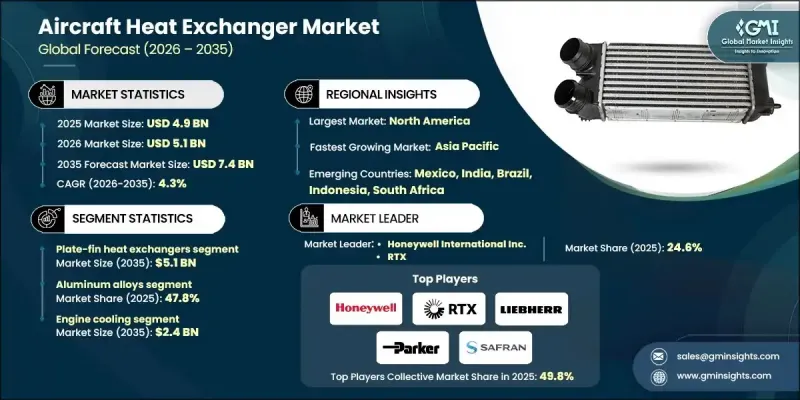

The Global Aircraft Heat Exchanger Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 7.4 billion by 2035.

Market growth is propelled by rising air passenger traffic, increasing focus on fuel efficiency, the emergence of advanced air mobility, and the growing applications of UAVs and military aircraft. Rising passenger demand is creating pressure on airlines to improve aircraft performance, efficiency, and sustainability, which in turn fuels the adoption of heat exchangers. Electric and hydrogen-electric propulsion systems are driving the need for lightweight, high-performance thermal solutions that can manage substantial heat from advanced powertrains. Heat exchangers play a critical role in maintaining optimal operational performance across all aircraft systems, particularly in new-generation electric and hybrid-electric platforms, meeting the expectations of low-emission aviation and sustainable flight initiatives.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $7.4 Billion |

| CAGR | 4.3% |

The plate-fin heat exchangers segment is expected to reach USD 5.1 billion by 2035. Their compact form, high thermal efficiency, and suitability for advanced and lightweight aircraft designs have accelerated adoption. Growth is largely driven by integration with modern engines, UAVs, and electric aircraft, which require efficient heat dissipation within confined spaces.

The aluminum alloys segment held 47.8% share in 2025. Heat exchangers made from aluminum alloys are favored for their superior strength-to-weight ratio, manufacturability, and cost-effectiveness. Airlines increasingly rely on these materials across narrow-body, wide-body, and UAV platforms to reduce weight and enhance fuel efficiency. Manufacturers are expected to focus on high-strength, thermally conductive aluminum grades to support next-generation aircraft designs.

U.S. Aircraft Heat Exchanger Market generated USD 1.6 billion in 2025. Growth in this region is driven by fleet modernization, expanding commercial and regional air traffic, and rising adoption of hybrid-electric and UAV platforms. Companies are concentrating on modular, thermally optimized heat exchangers for next-generation aircraft while investing in technology to support UAVs and regional aviation expansion.

Key players operating in the Global Aircraft Heat Exchanger Market include 3D Systems, Inc., AMETEK Inc., Boyd Corporation, Conflux Technology, Essex Industries, Inc., ETP Thermal Dynamics, Honeywell International Inc., HS-Nauka, JAMCO Corporation, Liebherr Group, and Meggitt PLC. Companies in the Global Aircraft Heat Exchanger Market strengthen their position by focusing on research and development to design high-efficiency, lightweight, and thermally optimized solutions for next-generation aircraft. They are investing in advanced manufacturing techniques such as 3D printing to produce complex geometries with enhanced heat transfer efficiency. Strategic collaborations with aviation OEMs and defense contractors expand market reach and support co-development of electric and hybrid propulsion systems. Firms also emphasize modular product designs for faster integration and cost-effective maintenance, while targeting regional markets with growing air traffic and UAV adoption to secure long-term contracts and boost market presence globally.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Heat exchanger type trends

- 2.2.2 Material type trends

- 2.2.3 Cooling medium trends

- 2.2.4 Application trends

- 2.2.5 Aircraft type trends

- 2.2.6 End use trends

- 2.2.7 Regional trends

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising air passenger traffic

- 3.2.1.2 Rising demand for fuel efficiency

- 3.2.1.3 Growth of advanced air mobility & electrified propulsion

- 3.2.1.4 Modular & integrated thermal management architectures

- 3.2.1.5 Rise of UAVs & military aircraft applications

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing complexity and certification requirements

- 3.2.2.2 Weight and space constraints in aircraft design

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of additive manufacturing for complex heat exchanger geometries

- 3.2.3.2 Integration of smart and embedded sensors for real-time thermal monitoring

- 3.2.3.3 Expansion in UAV, MALE/HALE, and defense platforms requiring advanced cooling

- 3.2.3.4 Development of next-generation lightweight materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Supply chain resilience

- 3.11 Geopolitical analysis

- 3.12 Workforce analysis

- 3.13 Digital transformation

- 3.14 Mergers, acquisitions, and strategic partnerships landscape

- 3.15 Risk assessment and management

- 3.16 Major contract awards (2022-2025)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Heat Exchanger Type, 2022 - 2035 (USD Million & Units)

- 5.1 Key trends

- 5.2 Plate-fin heat exchangers

- 5.3 Tube-fin heat exchangers

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million & Units)

- 6.1 Key trends

- 6.2 Aluminum alloys

- 6.3 Stainless steel

- 6.4 Titanium

- 6.5 Copper

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Cooling Medium, 2022 - 2035 (USD Million & Units)

- 7.1 Key trends

- 7.2 Air-to-air

- 7.3 Air-to-liquid

- 7.4 Liquid-to-liquid

- 7.5 Liquid-to-air

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million & Units)

- 8.1 Key trends

- 8.2 Engine cooling

- 8.3 Cabin heating & cooling (ECS)

- 8.4 Avionics cooling

- 8.5 Hydraulic cooling

- 8.6 Fuel heating & cooling

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million & Units)

- 9.1 Key trends

- 9.2 Commercial aircraft

- 9.2.1 Narrow-body aircraft

- 9.2.2 Wide-body aircraft

- 9.2.3 Regional jets

- 9.3 Military aircraft

- 9.3.1 Fighter jets

- 9.3.2 Transport aircraft

- 9.4 Business aviation

- 9.5 General aviation

- 9.6 Helicopters & rotorcraft

Chapter 10 Market Estimates and Forecast, By End Use, 2022 - 2035 (USD Million & Units)

- 10.1 Key trends

- 10.2 OEM (Line-Fit)

- 10.3 Aftermarket (MRO)

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global Key Players

- 12.1.1 Honeywell International Inc.

- 12.1.2 RTX

- 12.1.3 Liebherr Group

- 12.1.4 Parker Hannifin Corp

- 12.2 Regional Key Players

- 12.2.1 North America

- 12.2.1.1 3D Systems, Inc

- 12.2.1.2 AMETEK Inc.

- 12.2.1.3 Boyd Corporation

- 12.2.2 Europe

- 12.2.2.1 Safran S.A

- 12.2.2.2 Meggitt PLC

- 12.2.2.3 Triumph Group

- 12.2.3 APAC

- 12.2.3.1 JAMCO Corporation

- 12.2.3.2 HS-Nauka

- 12.2.3.3 TAT Technologies Ltd

- 12.2.1 North America

- 12.3 Niche Players / Disruptors

- 12.3.1 Conflux Technology

- 12.3.2 Essex Industries, Inc.

- 12.3.3 ETP Thermal Dynamics

- 12.3.4 THERMOVAC AEROSPACE

- 12.3.5 Wall Colmonoy