PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892788

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1892788

Marine Sealants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

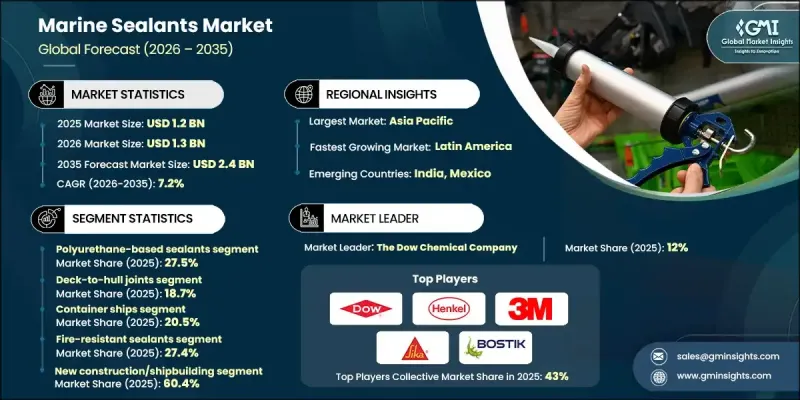

The Global Marine Sealants Market was valued at USD 1.2 billion in 2025 and is estimated to grow at a CAGR of 7.2% to reach USD 2.4 billion by 2035.

Marine sealants have evolved from being a niche product to becoming a crucial component in modern maritime operations. Their importance now extends beyond basic sealing to enhancing vessel integrity, corrosion protection, and long-term structural performance. Sustainability has become a major driver in the industry, as eco-friendly and low-emission sealants are increasingly favored in shipbuilding, maintenance, and retrofitting processes. The market is further fueled by technological advancements, including hybrid polymer formulations and low volatile organic compound (VOC) systems, which meet stringent environmental standards while delivering superior performance in harsh marine environments. Regional priorities and the strength of local maritime industries strongly influence growth patterns in this market, as innovation aligns with regulatory requirements and decarbonization goals worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.2 Billion |

| Forecast Value | $2.4 Billion |

| CAGR | 7.2% |

The polyurethane-based sealants segment held a 27.5% share in 2025 and is expected to grow at a CAGR of 6.8% through 2035. Their high flexibility and excellent adhesion under dynamic loads make them essential for hull joints and deck structures. Silicone-based sealants, known for UV and saltwater resistance, are preferred for exterior applications in challenging marine conditions. Polysulfide sealants remain in demand for their exceptional chemical and fuel resistance under harsh operational conditions.

The deck-to-hull joints segment held 18.7% share in 2025 and is expected to grow at a CAGR of 6.9% by 2035. Sealants in this application must withstand dynamic stresses from constant motion, while above-waterline applications demand UV and weather resistance, and below-waterline sealing requires advanced adhesion and water impermeability for long-term performance.

North America Marine Sealants Market accounted for a 15.4% share in 2025, driven by shipbuilding activities, recreational boating growth, and investments in offshore infrastructure. The region benefits from advanced manufacturing, robust safety regulations, and a focus on sustainability, creating opportunities for high-performance marine sealant technologies.

Key players operating in the Global Marine Sealants Market include Sika AG, 3M Company, Henkel AG & Co. KGaA, The Dow Chemical Company, PPG Industries, Inc., The Sherwin-Williams Company, Trelleborg AB, Berger Maritiem, Chugoku Marine Paints, Ltd., Jotun A/S, Hempel A/S, Feynlab, Sea-Shield, ITW Performance Polymers, Bostik (Arkema Group), Wacker Chemie AG, Momentive Performance Materials, and Evonik Industries AG. Companies in the Global Marine Sealants Market are employing several strategies to strengthen their market position. They are investing in research and development to create eco-friendly formulations with improved adhesion, UV resistance, and chemical durability. Strategic partnerships with shipbuilders, maintenance providers, and offshore operators expand market reach and ensure adoption of high-performance products. Firms are also focusing on regional expansion, particularly in emerging maritime markets, and optimizing distribution channels for faster product delivery.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Chemistry Type

- 2.2.3 Application

- 2.2.4 Vessel/Structure Type

- 2.2.5 Performance Characteristics

- 2.2.6 End use

- 2.3 TAM Analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid offshore wind energy expansion

- 3.2.1.2 Stringent IMO fire safety regulations

- 3.2.1.3 Global fleet expansion & modernization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced smart sealants

- 3.2.2.2 Skilled application requirements

- 3.2.3 Market opportunities

- 3.2.3.1 Self-healing & smart sealant technologies

- 3.2.3.2 Offshore wind foundation sealing specialization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Chemistry type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Chemistry Type, 2022-2035 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyurethane-based sealants

- 5.3 Silicone-based sealants (polysiloxanes)

- 5.4 Polysulfide-based sealants

- 5.5 Hybrid/modified silane polymers (ms polymers/stp)

- 5.6 Epoxy-based sealants

- 5.7 Butyl-based sealants

- 5.8 Acrylic-based sealants

- 5.9 Nano-hybrid smart sealants

- 5.10 Bio-based/sustainable formulations

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Deck-to-hull joints

- 6.3 Above waterline sealing

- 6.4 Below waterline sealing

- 6.5 Window & porthole bonding/direct glazing

- 6.6 Structural bonding & assembly

- 6.7 Offshore wind foundation sealing

- 6.7.1 Monopile grout seals

- 6.7.2 Pre-piled jacket sealing

- 6.7.3 Post-piled jacket sealing

- 6.7.4 Skirt seals (non-grouted monopiles)

- 6.7.5 Flange seals (VW, VT types)

- 6.7.6 Airtight platform seals (CS-111/114, CS-80/70)

- 6.7.7 Nacelle & turbine component sealing

- 6.8 Firestop & fire-resistant sealing

- 6.9 Ballast tank coating & sealing

- 6.10 Acoustic sealing

- 6.11 Anti-fouling applications

- 6.11.1 Biocidal anti-fouling

- 6.11.2 Biocide-free anti-fouling

Chapter 7 Market Estimates and Forecast, By Vessel/Structure Type, 2022-2035 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Container ships

- 7.3 Bulk carriers

- 7.3.1 Capesize (≥100,000 dwt)

- 7.3.2 Panamax (65,000-99,999 dwt)

- 7.3.3 Handymax (40,000-64,999 dwt)

- 7.3.4 Handysize (10,000-39,999 dwt)

- 7.4 Oil & chemical tankers

- 7.4.1 ULCC & VLCC (Ultra/Very Large Crude Carriers)

- 7.4.2 Suezmax Tankers

- 7.4.3 Aframax/LR2 Tankers

- 7.4.4 Panamax/LR1 Tankers

- 7.4.5 MR & Handy Tankers

- 7.4.6 Chemical Tankers (Specialized Sealing Requirements)

- 7.5 Offshore wind turbines & structures

- 7.6 Passenger vessels

- 7.7 Liquefied gas carriers

- 7.8 Naval & defense vessels

- 7.9 Offshore oil & gas structures

- 7.10 General cargo & multi-purpose ships

- 7.11 Small craft & recreational vessels

- 7.12 Fishing vessels

Chapter 8 Market Estimates and Forecast, By Performance Characteristics, 2022-2035 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Fire-resistant sealants

- 8.3 Anti-corrosion sealants

- 8.4 Uv-resistant sealants

- 8.5 Anti-fouling sealants

- 8.6 High-movement capability sealants

- 8.7 Self-healing sealants

Chapter 9 Market Estimates and Forecast, By End Use, 2022-2035 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 New construction/shipbuilding

- 9.3 Repair & maintenance

- 9.4 Retrofit & modernization

- 9.5 Offshore installation & construction

Chapter 10 Market Estimates and Forecast, By Region, 2022-2035 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Sika AG

- 11.2 3M Company

- 11.3 Henkel AG & Co. KGaA

- 11.4 The Dow Chemical Company

- 11.5 PPG Industries, Inc.

- 11.6 The Sherwin-Williams Company

- 11.7 Trelleborg AB

- 11.8 Berger Maritiem

- 11.9 Chugoku Marine Paints, Ltd.

- 11.10 Jotun A/S

- 11.11 Hempel A/S

- 11.12 Feynlab

- 11.13 Sea-Shield

- 11.14 ITW Performance Polymers

- 11.15 Bostik (Arkema Group)

- 11.16 Wacker Chemie AG

- 11.17 Momentive Performance Materials

- 11.18 Evonik Industries AG