PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913326

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1913326

Food Coating Ingredients Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

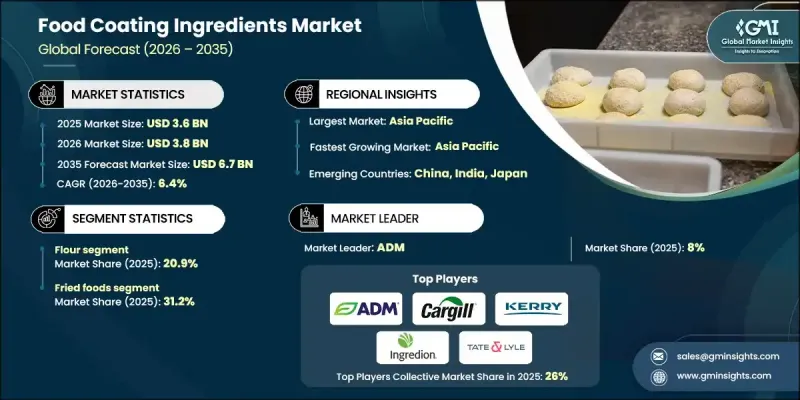

The Global Food Coating Ingredients Market was valued at USD 3.6 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 6.7 billion by 2035.

Food coating ingredients are formulated blends applied to food products to improve visual appeal, mouthfeel, taste consistency, and storage stability. These solutions include batters, crumbs, flours, starches, proteins, spices, and seasoning systems that form functional outer layers across a wide range of foods. Applications span fried items, bakery products, snacks, confectionery, and processed foods, serving large-scale manufacturers as well as foodservice operators. Rising demand for convenience foods, increasing preference for plant-based formulations, and heightened awareness around ingredient transparency are reshaping innovation priorities. Clean-label expectations now influence formulation decisions on a scale, with buyers favoring simple, recognizable ingredients and minimal processing. Younger consumers actively review labels and product composition, prompting suppliers to shift toward natural, non-GMO, organic, and allergen-conscious solutions. Reformulation efforts focus on replacing synthetic components, reducing additives, and extending shelf life through alternative preservation techniques that align with evolving consumer trust and regulatory standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.7 Billion |

| CAGR | 6.4% |

The flour-based coatings segment accounted for 20.9% share in 2025. Flour remains a core input across fried foods, baked goods, and processed categories due to its functional adaptability and cost efficiency. Wheat flour leads usage volumes, while rice, chickpea, and specialty grain flours continue gaining traction as gluten-free consumption rises.

The fried food applications segment held 31.2% share in 2025, supported by the expansion of quick-service dining, frozen meal consumption, and steady global demand for breaded and battered products. Consumption of ready-to-eat foods increased by about 26% over a defined historical period, reinforcing volume growth. Reduced-fat coating systems are increasingly adopted to lower oil absorption while preserving texture and flavor.

North America Food Coating Ingredients Market held 24.1% share in 2025. The region benefits from a strong foodservice presence, a well-established frozen foods sector, and consistent demand for organic and naturally positioned ingredients. Ongoing investments in processing capacity and sustainable manufacturing practices continue to support regional market strength.

Key companies active in the Global Food Coating Ingredients Market include Kerry Taste & Nutrition, Cargill Incorporated, Ingredion Incorporated, Archer Daniels Midland Company, Tate & Lyle PLC, Givaudan SA, Bunge Limited, Dohler Group, Ashland Global Holdings Inc, SensoryEffects, Continental Mills, Inc, Bowman Ingredients, and PGP International. Companies operating in the Global Food Coating Ingredients Market strengthen their competitive position through product innovation, portfolio diversification, and strategic customer alignment. Leading players invest in clean-label research, plant-based formulations, and functional performance improvements to meet evolving consumer and regulatory expectations. Capacity expansion and regional production optimization improve supply reliability and cost efficiency. Firms also emphasize customized solutions for industrial clients, supported by application testing and technical services.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Type, 2022-2035 (USD Billion & Tons)

- 5.1 Key trends

- 5.2 Batter

- 5.3 Breadcrumb

- 5.3.1 Fine

- 5.3.2 Medium

- 5.3.3 Coarse

- 5.4 Flour

- 5.4.1 Wheat

- 5.4.2 Rice

- 5.4.3 Corn

- 5.4.4 Others

- 5.5 Starches

- 5.5.1 Corn

- 5.5.2 Potato

- 5.5.3 Tapioca (cassava)

- 5.5.4 Wheat

- 5.5.5 Rice

- 5.6 Seasonings and Spices

- 5.6.1 Herbs

- 5.6.2 Spices

- 5.6.3 Blends

- 5.6.4 Salt variants

- 5.7 Proteins

- 5.7.1 Animal

- 5.7.2 Plant

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion & Tons)

- 6.1 Key trends

- 6.2 Fried Foods

- 6.2.1 Meat & Poultry

- 6.2.2 Seafood

- 6.2.3 Vegetables

- 6.2.4 Cheese & Dairy

- 6.3 Baked Foods

- 6.3.1 Savory

- 6.3.2 Sweet

- 6.4 Snacks and Appetizers

- 6.5 Processed Foods

- 6.6 Confectionery

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2022-2035 (USD Billion & Tons)

- 7.1 Key trends

- 7.2 Supermarkets/Hypermarket

- 7.3 Retail stores

- 7.4 Online retail

- 7.4.1 E-commerce marketplaces

- 7.4.2 Brand D2C

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Archer Daniels Midland Company (ADM)

- 9.2 Cargill Incorporated

- 9.3 Kerry Group

- 9.4 Ingredion Incorporated

- 9.5 Tate & Lyle PLC

- 9.6 Ashland Global Holdings Inc

- 9.7 PGP International, Inc (A Bunge Limited Company)

- 9.8 Dohler Group

- 9.9 Bowman Ingredients

- 9.10 SensoryEffects (A division of Balchem Corporation)

- 9.11 Bunge Limited

- 9.12 Continental Mills, Inc

- 9.13 Givaudan SA

- 9.14 Kerry Taste & Nutrition