PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928903

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928903

Animal Feed Alternative Protein Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

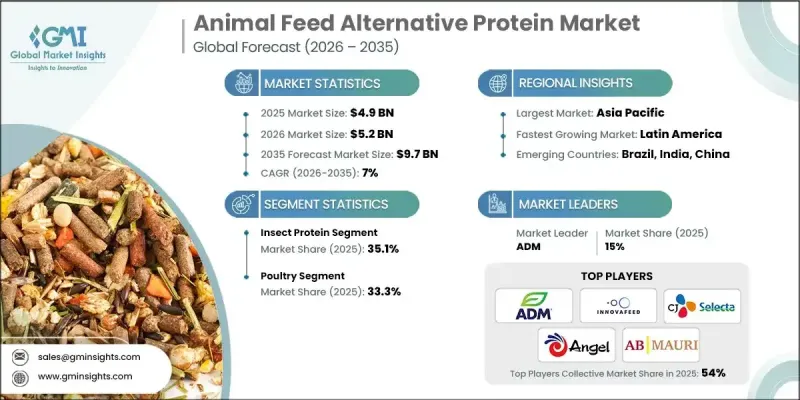

The Global Animal Feed Alternative Protein Market was valued at USD 4.9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 9.7 billion by 2035.

Market growth is driven by sustainability demands that reshaped protein sourcing strategies across feed supply chains. Environmental pressures related to emissions and land utilization associated with traditional livestock production are acknowledged as major drivers encouraging integrators, manufacturers, and retailers to reassess protein inputs. Alternative feed proteins are positioned as lower-impact solutions because they rely on side-stream resources and deliver higher protein yields per hectare, while supporting long-term supply resilience. The discussion emphasizes that sustainability goals, regulatory momentum, and innovation collectively accelerated diversification away from conventional feed proteins during this timeframe, laying the foundation for broader commercial adoption across multiple animal production systems worldwide.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $4.9 Billion |

| Forecast Value | $9.7 Billion |

| CAGR | 7% |

Market adoption is further explained through the lens of food security and cost volatility. Rising feed expenses between 2021 and 2023, driven by supply disruptions and geopolitical uncertainty, increased pressure on producers to manage risk. Alternative proteins are portrayed as stabilizing inputs that enabled trials across major animal production categories. Performance outcomes from insect-derived meals, fermented plant proteins, and microbial-based ingredients are described as comparable to traditional imported protein meals, while also reducing dependency on external supply chains. Scientific research focused on digestion, gut functionality, and reduced antibiotic reliance strengthened confidence that alternative feed proteins can support animal health, welfare outcomes, and premium product positioning.

The insect protein segment held 35.1% share in 2025 and is projected to grow at a CAGR of 6.8% from 2026 to 2035. The market description highlights a clear transition away from reliance on single protein sources toward diversified ingredient portfolios. Large-scale feed manufacturers are described as blending insect-based inputs with microbial, algal, fungal, yeast-derived, and processed soy proteins. This combined approach is positioned to balance cost management, sustainability messaging, nutritional consistency, amino acid optimization, and additional functional benefits related to gut health and feed efficiency.

The poultry segment held 33.3% share in 2025, with a CAGR of 6.8% through 2035. Strategic investment is described as concentrated in high-margin animal sectors where premium feed formulations can justify higher ingredient costs. Collaborative development between producers and feed formulators is highlighted as a method for creating balanced diets that integrate alternative proteins while supporting claims related to sustainability, reduced reliance on conventional marine proteins, and novel feed inputs within both animal nutrition and companion animal markets.

North America Animal Feed Alternative Protein Market reached USD 1.19 billion in 2024. Growth in the region is attributed to vertically integrated producers seeking supply security and environmental alignment. Strong demand from poultry, specialty feed, and pet nutrition segments continues to support the adoption of fermented, yeast-based, and single-cell proteins. The United States is identified as the dominant national market, supported by advanced fermentation infrastructure, retailer-led sustainability commitments, and consistent demand for antibiotic-free and premium-positioned feed solutions that partially replace conventional soymeal.

The competitive landscape includes ADM, Calysta Inc, Angel Yeast, Innova Feed, CJ Selecta, Hamlet Protein A/S, Titan Biotech Ltd, CHS Inc, E.I. Du Pont De Nemours And Company, Agriprotein GmbH, Deep Branch Biotechnology, AB Mauri, and Crescent Biotech, all of which are actively shaping the development and commercialization of alternative feed protein solutions across global markets. Companies operating in the animal feed alternative protein market are described as strengthening their positions through capacity expansion, technology investment, and strategic partnerships. Many players are focusing on scaling fermentation and insect production systems to improve cost competitiveness and supply reliability. Portfolio diversification is emphasized as firms integrate multiple protein formats to meet varying nutritional and regulatory requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Livestock

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Volatile soymeal prices and supply disruptions

- 3.2.1.2 Rising meat and aquaculture demand in Asia

- 3.2.1.3 Sustainability, deforestation and emissions concerns

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Higher cost and limited large scale supply

- 3.2.2.2 Regulatory approvals and safety perception issues

- 3.2.3 Market opportunities

- 3.2.3.1 Upcycling agri food side streams into feed protein

- 3.2.3.2 Premium, antibiotic free and functional meat labels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Insect Protein

- 5.3 Soy Protein Isolates

- 5.4 Soy Protein Concentrates

- 5.5 Fermented Soy Protein

- 5.6 Duckweed Protein

- 5.7 Single Cell Protein

- 5.7.1 Algae Protein

- 5.7.2 Grain Protein

- 5.7.3 Fungal Protein

- 5.7.4 Yeast Protein

- 5.8 Hamlet Protein

Chapter 6 Market Estimates and Forecast, By Livestock, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Poultry

- 6.2.1 Broiler

- 6.2.2 Layer

- 6.2.3 Turkey

- 6.2.4 Others

- 6.3 Swine

- 6.3.1 Starter

- 6.3.2 Grower

- 6.3.3 Sow

- 6.3.4 Cattle

- 6.4 Dairy

- 6.4.1 Calf

- 6.4.2 Others

- 6.5 Aquaculture

- 6.5.1 Salmon

- 6.5.2 Trout’s

- 6.5.3 Shrimps

- 6.5.4 Carp

- 6.5.5 Others

- 6.6 Pet Food

- 6.7 Equine

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 ADM

- 8.2 CJ Selecta

- 8.3 Calysta Inc

- 8.4 CHS Inc

- 8.5 Hamlet Protein A/S

- 8.6 Titan Biotech Ltd

- 8.7 E.I. Du Pont De Nemours And Company

- 8.8 Deep Branch Biotechnology

- 8.9 Agriprotein GmbH

- 8.10 Innova Feed

- 8.11 Angel Yeast

- 8.12 AB Mauri

- 8.13 Crescent Biotech