PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928923

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1928923

Barite Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

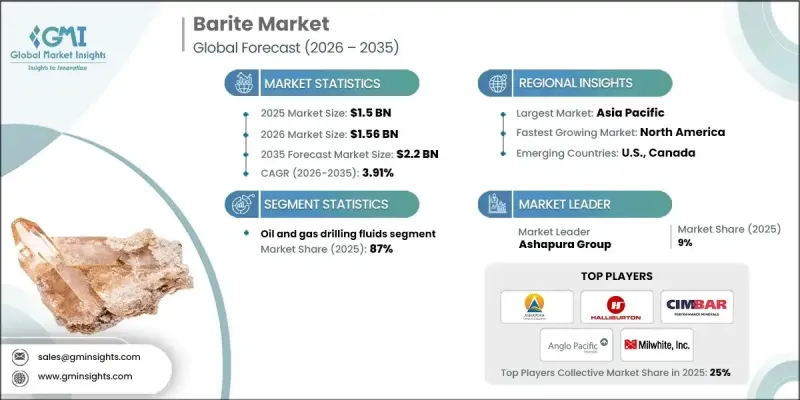

The Global Barite Market was valued at USD 1.5 billion in 2025 and is estimated to grow at a CAGR of 3.91% to reach USD 2.2 billion by 2035.

Market growth is supported by rising infrastructure development and construction activity across developing regions, which is broadening the scope of barite consumption beyond its conventional uses. Increasing investments in large-scale infrastructure and industrial projects across the Asia Pacific, Latin America, and the Middle East are contributing to higher demand for barite-based materials used in high-density construction solutions and specialized industrial applications. At the same time, environmental compliance requirements and sustainability goals are reshaping mining and processing practices within the industry. Regulatory frameworks in the United States impose strict operational standards on barite producers, including wastewater management, discharge control, and process optimization. Despite diversification into non-energy sectors, the oil and gas industry continues to be the primary driver of demand, accounting for the majority of global barite usage. The mineral's naturally high density makes it essential for maintaining pressure balance, enhancing operational safety, and supporting efficiency during drilling activities. These combined factors continue to influence supply strategies, pricing dynamics, and long-term investment decisions across the global barite market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 3.91% |

Barite grades are segmented based on specific gravity standards, with API Grade 4.1 emerging as the most widely used specification in drilling fluid applications since its introduction in 2010. API Grade 4.2 remains a higher-purity option with a minimum density of 4.20 g/mL, while sub-API grades are utilized where compliance with API specifications is not required. Specialty high-density barite is reserved for applications that demand maximum material weight and performance.

The oil & gas drilling fluids segment accounted for 87% share in 2025. In these applications, barite acts as a weighting material that increases fluid density to manage subsurface pressure, support wellbore stability, reduce operational risk, and assist in the removal of drilling debris during extraction activities.

Asia Pacific Barite Market held a 45.1% share in 2025, supported by strong regional production and consumption. China remains the largest global producer while also maintaining substantial domestic demand, with output reaching nearly 2.1 million metric tons in 2024. India continues to strengthen its role as a key supplier, with production volumes increasing to approximately 2.6 million metric tons during the same year.

Key companies active in the Global Barite Market include Halliburton, Ashapura Group, SCR-Sibelco, CIMBAR Performance Minerals, Deutsche Baryt Industrie, Milwhite, Spectrum Chemical Manufacturing, Excalibar Minerals, Anglo Pacific Minerals, Barium & Chemicals, Albar Industrial Minerals, Mil-Spec Industries, New Riverside Ochre, and International Earth Products. Companies operating in the Global Barite Market are adopting a range of strategies to reinforce their market position and expand global reach. These include capacity expansion initiatives, modernization of mining and processing facilities, and investment in environmentally compliant production methods. Firms are prioritizing long-term supply agreements with end-use industries, particularly in energy and infrastructure sectors, to ensure demand stability. Strategic acquisitions, partnerships, and geographic diversification are also being pursued to strengthen distribution networks. Additionally, companies are focusing on quality optimization, cost control, and regulatory compliance to maintain competitiveness while meeting evolving industry standards and sustainability expectations.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Specific gravity grade

- 2.2.2 Form

- 2.2.3 Application

- 2.2.4 End Use industry

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By form

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Barite Market, By Specific Gravity Grade, 2022-2035 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 API grade 4.2

- 5.3 API grade 4.1

- 5.4 Sub-API grade (3.9-4.0 sg)

- 5.5 Others

Chapter 6 Barite Market, By Form, 2022-2035 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Lumps

- 6.3 Powder

Chapter 7 Barite Market, By Application, 2022-2035 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Oil & gas drilling fluids

- 7.3 Barium chemicals

- 7.4 Paints & coatings

- 7.5 Rubber & plastics

- 7.6 Pharmaceuticals

- 7.7 Glass & ceramics

- 7.8 Radiation shielding

- 7.9 Friction products

- 7.10 Others

Chapter 8 Barite Market, By End Use Industry, 2022-2035 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Oil & gas industry

- 8.3 Construction industry

- 8.4 Healthcare industry

- 8.5 Automotive industry

- 8.6 Chemical manufacturing

- 8.7 Paints & coatings manufacturing

- 8.8 Others

Chapter 9 Market Size and Forecast, By Region, 2022-2035 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Spectrum Chemical Manufacturing

- 10.2 Deutsche Baryt Industrie

- 10.3 Halliburton

- 10.4 New Riverside Ochre

- 10.5 Albar Industrial Minerals

- 10.6 Excalibar Minerals

- 10.7 Anglo Pacific Minerals

- 10.8 SCR-Sibelco

- 10.9 Ashapura Group

- 10.10 Barium & Chemicals

- 10.11 CIMBAR Performance Minerals

- 10.12 Milwhite

- 10.13 Mil-Spec Industries

- 10.14 International Earth Products