PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936575

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936575

Europe Electric Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

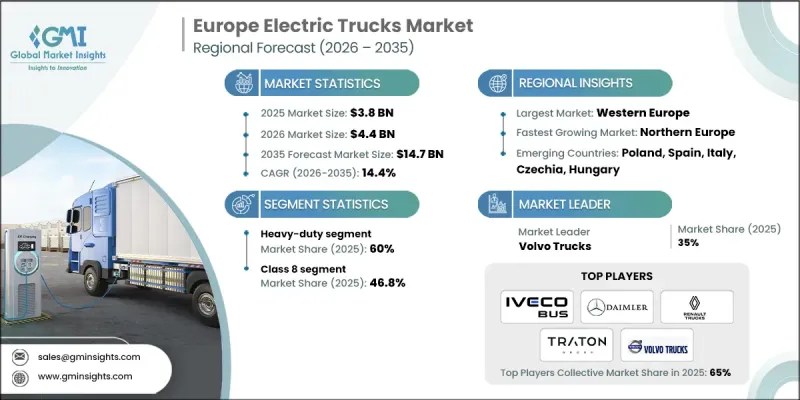

Europe Electric Trucks Market was valued at USD 3.8 billion in 2025 and is estimated to grow at a CAGR of 14.4% to reach USD 14.7 billion by 2035.

The market is undergoing a major transition driven by tightening environmental regulations, improving battery performance, and the rapid expansion of high-capacity charging networks across the region. Fleet operators are increasingly drawn to electric trucks due to significantly lower energy consumption and reduced maintenance requirements compared to diesel-powered vehicles. Operating expenses for electric trucks are estimated to be around 30% lower than those of diesel trucks for comparable workloads, while electric drivetrains deliver substantially higher energy efficiency for the same transport output. Despite these advantages, adoption has been constrained by high upfront vehicle costs, which remain two to three times higher than diesel alternatives. To address this challenge, Europe is witnessing growing acceptance of flexible financing structures, leasing models, and total cost of ownership-based procurement strategies that are improving affordability and accelerating deployment.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.8 Billion |

| Forecast Value | $14.7 Billion |

| CAGR | 14.4% |

The heavy-duty segment accounted for 60% share in 2025 and is expected to grow at a CAGR of 13.5% through 2035. Advancements in battery density and the parallel development of charging and refueling ecosystems are strengthening the viability of heavy electric trucks. With increasingly stringent carbon emission limits and strong sustainability commitments from freight and logistics operators, battery-powered and fuel cell-based heavy-duty trucks are becoming central to Europe's future freight transport framework, positioning this segment for significant technological transformation.

The class 8 vehicles segment represented 46.8% share in 2025 and is forecast to grow at a CAGR of 13% from 2026 to 2035. Higher adoption across logistics, industrial transport, and construction sectors is being driven by regulatory mandates targeting zero-emission freight movement. Battery electric trucks have gained strong acceptance in heavy-duty applications, while fuel cell electric models are gradually gaining traction for long-distance operations where extended range and reduced downtime are critical considerations.

Germany Electric Trucks Market held a 35.5% share in 2025 and is projected to grow at a CAGR of 14.8% between 2026 and 2035. Market leadership is supported by ambitious climate objectives, strong industrial logistics demand, and favorable national policies that reduce adoption barriers. Incentives such as purchase support, tax advantages, and accelerated cost recovery have strengthened fleet electrification across major logistics corridors and industrial regions.

Key companies operating in the Europe Electric Trucks Market include Volvo Trucks, Daimler Truck, Scania AB, MAN Truck, Iveco, Renault Trucks, DAF Trucks, Tatra, Sisu Auto, and BelAZ. Companies in the Europe electric trucks market are strengthening their competitive position through accelerated electrification strategies, platform innovation, and strategic partnerships. Leading manufacturers are investing heavily in battery development, powertrain efficiency, and modular vehicle architectures to support multiple use cases. Firms are expanding service networks and forming collaborations to improve operational reliability for fleet customers. Many players are also offering flexible financing, leasing, and pay-per-use models to address high upfront costs. Strategic alliances with logistics providers and infrastructure developers, along with localized manufacturing and supply chain optimization, are enabling companies to improve scalability, meet regulatory requirements, and secure long-term market presence across Europe.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Class

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Body

- 2.2.6 End Use

- 2.2.7 Battery capacity

- 2.2.8 Range capacity

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid electrification of commercial fleets

- 3.2.1.2 Stringent CO2 emission regulations for heavy-duty vehicles

- 3.2.1.3 Expansion of zero-emission zones and green freight corridors

- 3.2.1.4 Declining battery costs and improving total cost of ownership (TCO)

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront vehicle costs

- 3.2.2.2 Charging infrastructure constraints for heavy-duty fleets

- 3.2.2.3 Range and payload limitations in long-haul applications

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of dedicated fleet charging infrastructure

- 3.2.3.2 Expansion of transport-as-a-service and leasing models

- 3.2.3.3 Hydrogen fuel-cell trucks for long-haul transport

- 3.2.3.4 Public procurement and municipal fleet electrification

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Western Europe

- 3.4.1.1 EU Alternative Fuels Infrastructure Regulation (AFIR)

- 3.4.1.2 Eurovignette Toll Exemption Extension

- 3.4.1.3 Zero Emission / Low Emission Zones

- 3.4.2 Eastern Europe

- 3.4.2.1 EU AFIR Charger Deployment Targets

- 3.4.2.2 National EV Charging Network Tenders

- 3.4.2.3 EU CO2 Emissions Standards for HDVs

- 3.4.3 Northern Europe

- 3.4.3.1 AFIR Infrastructure Mandates

- 3.4.3.2 National Subsidies & Tax Exemptions for EV Trucks

- 3.4.3.3 Low Emission / Zero-Emission Zones

- 3.4.4 Southern Europe

- 3.4.4.1 AFIR Charging Corridor Requirements

- 3.4.4.2 Diesel Truck Entry Bans

- 3.4.4.3 Regional Incentives & Funding for EV Trucks

- 3.4.1 Western Europe

- 3.5 PESTEL analysis

- 3.6 Technology and Innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Production statistics

- 3.8.1 Production hubs

- 3.8.2 Consumption hubs

- 3.8.3 Export and import

- 3.9 Pricing Analysis

- 3.9.1 By region

- 3.9.2 By Product

- 3.10 Cost analysis & total cost of ownership (TCO)

- 3.10.1 CapEx & OpEx comparison (Diesel vs Electric)

- 3.10.2 Purchase incentives & subsidies

- 3.10.3 Battery replacement costs

- 3.10.4 Maintenance & operational savings

- 3.11 Sustainability and environmental impact analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook & opportunities

- 3.13 Investment & funding landscape

- 3.13.1 Public funding programs

- 3.13.2 Private investments & partnerships

- 3.13.3 Venture capital in e-truck startups

- 3.14 Fleet adoption & usage patterns

- 3.14.1 Fleet size & deployment

- 3.14.2 Urban vs long-haul usage

- 3.14.3 Fleet electrification roadmap

- 3.14.4 Total fleet cost savings

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Western Europe

- 4.2.2 Eastern Europe

- 4.2.3 Northern Europe

- 4.2.4 Southern Europe

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Class, 2022 - 2035 ($Bn, Unit)

- 5.1 Key trends

- 5.2 Class 2

- 5.3 Class 3

- 5.4 Class 4

- 5.5 Class 5

- 5.6 Class 6

- 5.7 Class 7

- 5.8 Class 8

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Unit)

- 6.1 Key trends

- 6.2 Light duty

- 6.3 Medium duty

- 6.4 Heavy duty

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Unit)

- 7.1 Key trends

- 7.2 BEV

- 7.3 PHEV

- 7.4 HEV

- 7.5 FCEV

Chapter 8 Market Estimates & Forecast, By Body, 2022 - 2035 ($Bn, Unit)

- 8.1 Key trends

- 8.2 Pickup

- 8.3 Box / cargo

- 8.4 Flatbed

- 8.5 Dump

- 8.6 Refrigerated

- 8.7 Tanker

- 8.8 Concrete mixer

- 8.9 Refuse

- 8.10 Tow truck

- 8.11 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn, Unit)

- 9.1 Key trends

- 9.2 Construction

- 9.3 Logistics & transportation

- 9.4 Mining

- 9.5 Oil & gas

- 9.6 Municipal services

- 9.7 Agriculture

- 9.8 Defense

- 9.9 Retail & e-commerce

Chapter 10 Market Estimates & Forecast, By Battery Capacity, 2022 - 2035 ($Bn, Unit)

- 10.1 Key trends

- 10.2 Below 100 kWh

- 10.3 100-300 kWh

- 10.4 Above 300 kWh

Chapter 11 Market Estimates & Forecast, By Range Capacity, 2022 - 2035 ($Bn, Unit)

- 11.1 Key trends

- 11.2 Short range (Up to 150 miles)

- 11.3 Medium range (150 to 250 miles)

- 11.4 Long range (Over Range 250 miles)

Chapter 12 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

- 12.1 Key trends

- 12.2 Western Europe

- 12.2.1 Germany

- 12.2.2 Austria

- 12.2.3 France

- 12.2.4 Switzerland

- 12.2.5 Belgium

- 12.2.6 Luxembourg

- 12.2.7 Netherlands

- 12.2.8 Portugal

- 12.3 Eastern Europe

- 12.3.1 Poland

- 12.3.2 Romania

- 12.3.3 Czechia

- 12.3.4 Slovenia

- 12.3.5 Hungary

- 12.3.6 Bulgaria

- 12.3.7 Slovakia

- 12.3.8 Croatia

- 12.4 Northern Europe

- 12.4.1 UK

- 12.4.2 Denmark

- 12.4.3 Sweden

- 12.4.4 Finland

- 12.4.5 Norway

- 12.5 Southern Europe

- 12.5.1 Italy

- 12.5.2 Spain

- 12.5.3 Greece

- 12.5.4 Bosnia and Herzegovina

- 12.5.5 Albania

Chapter 13 Company Profiles

- 13.1 Global Players

- 13.1.1 BelAZ

- 13.1.2 BYD

- 13.1.3 Daimler Truck

- 13.1.4 Ford

- 13.1.5 Foton

- 13.1.6 Fuso

- 13.1.7 Hyundai Motor Group

- 13.1.8 Isuzu

- 13.1.9 Nikola Corporation

- 13.1.10 Tesla

- 13.1.11 Volvo Trucks

- 13.2 Regional Players

- 13.2.1 DAF Trucks

- 13.2.2 Einride

- 13.2.3 Iveco

- 13.2.4 MAN Truck

- 13.2.5 Quantron AG

- 13.2.6 Renault Trucks

- 13.2.7 Scania AB

- 13.2.8 Sisu Auto

- 13.2.9 TATA

- 13.2.10 Tatra

- 13.3 Emerging Players

- 13.3.1 BEDEO

- 13.3.2 E-Trucks Europe BE

- 13.3.3 Quantron AG

- 13.3.4 SuperPanther

- 13.3.5 Tevva Motors

- 13.3.6 Windrose Technology