PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936646

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1936646

Waste Heat to Power Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

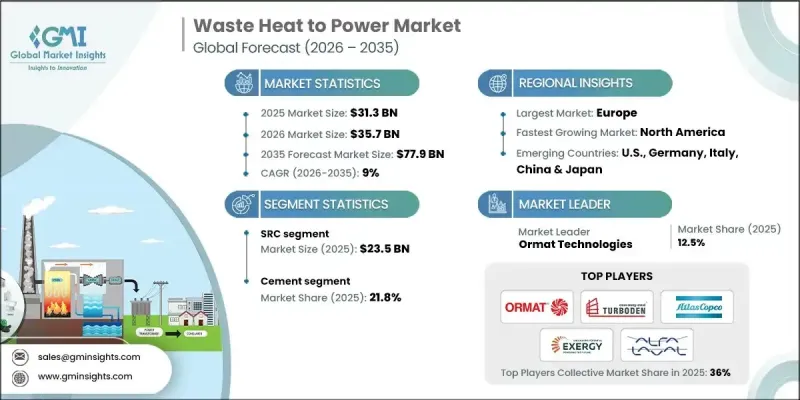

The Global Waste Heat to Power Market was valued at USD 31.3 billion in 2025 and is estimated to grow at a CAGR of 9% to reach USD 77.9 billion by 2035.

The market growth is driven by stricter energy efficiency regulations and the rising need for industrial decarbonization. Heavy industries such as cement, steel, glass, chemicals, and pulp & paper operate with high-temperature processes that generate significant thermal losses. WHP systems capture this otherwise wasted heat and convert it into electricity, helping facilities reduce energy consumption, meet efficiency targets, and comply with internal carbon budgets or ISO 50001-style programs. Energy price volatility makes self-generation particularly valuable, as WHP provides reliable, low-cost power while reducing dependence on the grid and exposure to peak tariffs. Multi-plant deployments create cost synergies, improve power factor, and lower demand charges. Increasing ESG commitments and the drive toward sustainable industrial operations have positioned WHP as a strategic energy management tool for energy- and emissions-intensive industries. Over time, these systems provide measurable cost savings and operational resilience across sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $31.3 Billion |

| Forecast Value | $77.9 Billion |

| CAGR | 9% |

The Steam Rankine Cycle (SRC) segment reached USD 23.5 billion in 2025 and is forecasted to grow at a CAGR of 7.5% through 2035. SRC remains the preferred technology in industries with high-temperature waste heat availability due to its proven turbine performance and familiarity among plant operators. Its compatibility with existing boiler and steam infrastructure makes it ideal for large-scale industrial applications, supporting widespread adoption in cement, steel, petrochemical, and power generation facilities. The long operational history and reliability of SRC systems reinforce confidence in deploying them for continuous industrial processes.

The cement segment held a 21.8% share in 2025 and is expected to grow at a CAGR of 8.5% through 2035. High-temperature processes in cement and refinery operations create consistent waste heat streams suitable for electricity generation. Rising energy costs and decarbonization pressures are encouraging plants to leverage WHP systems to reduce fuel use, electricity purchases, and grid reliance. Regulatory requirements and corporate ESG initiatives further drive the adoption of WHP as a solution to enhance energy efficiency while supporting sustainability goals and operational optimization.

North America Waste Heat to Power Market generated USD 3.3 billion in 2025. Energy-intensive sectors such as petroleum refining, chemicals, steel, food processing, and cement contribute significant thermal losses that can be captured for on-site power generation. The adoption of Organic Rankine Cycle (ORC) systems is growing due to their flexibility in handling diverse temperature profiles and retrofitting capabilities for existing industrial sites. Incentives under clean energy programs, coupled with rising electricity costs and corporate sustainability mandates, are accelerating the deployment of WHP systems as a cost-effective and environmentally responsible solution for distributed power generation.

Key players operating in the Global Waste Heat to Power Market include AC Boiler SpA, ALFA LAVAL, Atlas Copco, Aura GmbH & CO. KG, Climeon, Cochran Ltd., Durr Group, Exergy International Srl, Forbes Marshall, General Electric, IHI Corporation, Mitsubishi Heavy Industries, Ltd., Ormat Technologies, Rentech Boiler System, Siemens Energy, Thermax Ltd, Turboden, and Walchandnagar Industries Limited (WIL). Companies in the waste heat to power market are adopting multiple strategies to strengthen their position and expand market share. These include investing in R&D to enhance efficiency and retrofit capabilities for diverse industrial heat sources. Firms are forming strategic alliances and partnerships with energy service providers and technology companies to expand deployment opportunities and integrate advanced control systems. Companies are also entering new geographic markets and providing turnkey solutions to increase adoption among heavy industrial clients.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Application trends

- 2.1.4 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis of induction heating systems

- 3.8 Emerging opportunities & trends

- 3.9 Investment analysis & future prospects

- 3.10 Sustainability initiatives & industry 4.0 integration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 SRC

- 5.3 ORC

- 5.4 Kalina

Chapter 6 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 Petroleum refining

- 6.3 Cement

- 6.4 Heavy Metal

- 6.5 Chemical

- 6.6 Paper

- 6.7 Food & beverage

- 6.8 Glass

- 6.9 Others

Chapter 7 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 Italy

- 7.3.4 France

- 7.3.5 Belgium

- 7.3.6 Spain

- 7.3.7 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 AC Boiler SpA

- 8.2 ALFA LAVAL

- 8.3 Atlas Copco

- 8.4 Aura GmbH & CO. KG

- 8.5 Climeon

- 8.6 Cochran Ltd.

- 8.7 Durr Group

- 8.8 Exergy International Srl

- 8.9 Forbes Marshall

- 8.10 General Electric

- 8.11 IHI Corporation

- 8.12 Mitsubishi Heavy Industries, Ltd.

- 8.13 Ormat Technologies

- 8.14 Rentech Boiler System

- 8.15 Siemens Energy

- 8.16 Thermax Ltd

- 8.17 Turboden

- 8.18 Walchandnagar Industries Limited (WIL)