PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959271

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959271

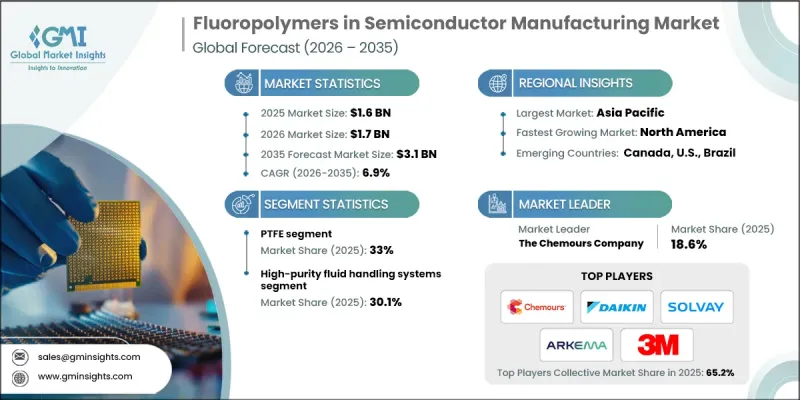

Fluoropolymers in Semiconductor Manufacturing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Fluoropolymers in Semiconductor Manufacturing Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 6.9% to reach USD 3.1 billion by 2035.

The semiconductor industry relies heavily on fluoropolymers due to their exceptional chemical resistance, thermal stability, and electrical insulation properties, which are critical for advanced device fabrication. Increasing demand for smaller, faster, and more efficient semiconductors has intensified the need for materials that can endure extreme processing environments. Asia-Pacific currently dominates the market, driven by the extensive semiconductor manufacturing capacities of China, South Korea, and Taiwan, supported by ongoing investments in fabrication infrastructure. The growing adoption of technologies such as 5G, artificial intelligence, and the Internet of Things is further increasing the requirement for advanced semiconductor components. North America is also witnessing rapid growth as manufacturers implement EUV and high-NA lithography technologies, which demand high-performance fluoropolymer materials capable of providing chemical protection and reliable performance at nanometer scales, ensuring enhanced yield and device efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.1 Billion |

| CAGR | 6.9% |

The PTFE (Polytetrafluoroethylene) segment held 33% share in 2025 and is expected to grow at a CAGR of 7.6% through 2035. Semiconductor manufacturers prefer PTFE because of its unmatched chemical resistance, high-temperature tolerance, and excellent dielectric properties. PTFE plays a crucial role in insulating layers, gaskets, and sealing applications, protecting semiconductor devices from harsh processing conditions while maintaining consistent performance across critical applications.

The high-purity fluid handling systems segment accounted for 30.1% share in 2025. These systems are essential in semiconductor production, where ultra-clean and precise environments are necessary to fabricate defect-free chips. Fluoropolymer-based fluid handling systems ensure high purity, precise measurement, and chemical resistance, which are critical for smaller node semiconductor technology and high-performance chip manufacturing.

North America Fluoropolymers in Semiconductor Manufacturing Market is expected to grow at a CAGR of 7.8% between 2026 and 2035. Market expansion is driven by the adoption of next-generation production tools that rely on advanced fluoropolymer materials to enhance thermal protection, contamination control, and process efficiency. Semiconductor fabrication facilities are increasingly miniaturizing chip designs, requiring materials that maintain chemical and thermal performance under extreme conditions, ultimately improving yield and overall device reliability.

Key players operating in the Global Fluoropolymers in Semiconductor Manufacturing Market include 3M Company, Arkema S.A., Daikin Industries, Ltd, Holscot Advanced Polymers Ltd, Pexco LLC, Parker Hannifin Corporation, Saint-Gobain, Solvay S.A., and The Chemours Company. Companies in the fluoropolymers in semiconductor manufacturing market are strengthening their position through innovation and strategic collaborations. Many are investing in research and development to create next-generation fluoropolymer materials with enhanced chemical, thermal, and electrical properties to meet the demands of advanced semiconductor nodes. Firms are expanding production capacities to support growing global semiconductor fabrication, particularly in high-demand regions such as Asia-Pacific and North America. Partnerships with semiconductor equipment manufacturers and strategic alliances with chip makers help integrate fluoropolymer solutions into critical fabrication processes.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Fluoropolymer type

- 2.2.3 Application

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Aggressive fab capacity expansion

- 3.2.1.2 EUV & high-NA lithography adoption

- 3.2.1.3 Advanced packaging proliferation

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 PFAS regulatory restrictions & compliance costs

- 3.2.2.2 Long material qualification cycles

- 3.2.3 Market opportunities

- 3.2.3.1 China foundational node capacity expansion

- 3.2.3.2 Advanced packaging material innovation

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By Fluoropolymer type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Fluoropolymer Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 PTFE

- 5.3 PFA

- 5.4 FEP

- 5.5 PVDF

- 5.6 ETFE

- 5.7 PCTFE

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 High-purity fluid handling systems

- 6.2.1 Bulk chemical distribution

- 6.2.2 Chemical storage & transport

- 6.2.3 Filtration systems

- 6.2.4 Others

- 6.3 Chemical delivery systems

- 6.3.1 Automated dispensing systems

- 6.3.2 Mix & blend systems

- 6.3.3 Others

- 6.4 Wafer handling & transport

- 6.4.1 Wafer carriers & cassettes

- 6.4.2 Direct wafer contact components

- 6.4.3 Robotic handling fixtures

- 6.4.4 Others

- 6.5 Wet processing equipment

- 6.6 Plasma processing components

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 The Chemours Company

- 8.2 Daikin Industries, Ltd

- 8.3 Solvay S.A.

- 8.4 Arkema S.A.

- 8.5 3M Company

- 8.6 Saint-Gobain

- 8.7 Parker Hannifin Corporation

- 8.8 Pexco LLC

- 8.9 Holscot Advanced Polymers Ltd