PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959291

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959291

Performance-on-Demand Subscription Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

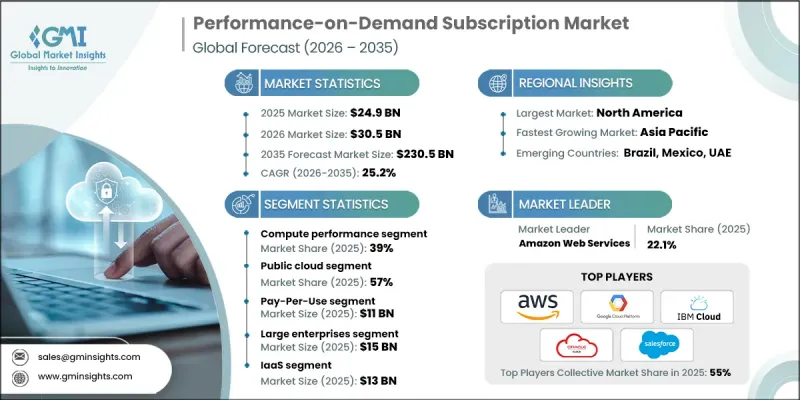

The Global Performance-on-Demand Subscription Market was valued at USD 24.9 billion in 2025 and is estimated to grow at a CAGR of 25.2% to reach USD 230.5 billion by 2035.

Market growth is fueled by the accelerating shift toward cloud-native architectures, the growing preference among enterprises for consumption-based IT models, and the increasing need to optimize performance in real-time while maintaining cost discipline. Organizations across industries are under mounting pressure to enhance operational flexibility, control infrastructure spending, improve application responsiveness, and comply with evolving security and regulatory standards. As a result, performance-based subscription frameworks that align resource utilization with actual workload demand are gaining widespread traction. Enterprises are moving away from fixed-capacity infrastructure toward scalable, usage-driven environments that support dynamic provisioning and measurable performance outcomes. This transition is particularly strong in hybrid and multi-cloud ecosystems, where businesses require continuous visibility into compute, storage, networking, and application efficiency. The performance-on-demand subscription market is therefore positioned for substantial expansion as digital transformation initiatives intensify globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $24.9 Billion |

| Forecast Value | $230.5 Billion |

| CAGR | 25.2% |

Rapid technological innovation is reshaping the performance-on-demand subscription landscape. Advancements in artificial intelligence and machine learning are enabling predictive resource allocation, automated workload balancing, and real-time infrastructure analytics. Modern observability tools and orchestration platforms are enhancing visibility across distributed IT systems, while edge-to-cloud connectivity is improving response times and operational resilience. Serverless computing frameworks and modular subscription models are further transforming traditional infrastructure strategies by allowing organizations to scale resources instantly without heavy capital expenditure. Industry participants are increasingly focused on interoperable, cloud-centric subscription ecosystems that provide granular control over performance metrics and spending patterns. These developments are redefining enterprise IT strategies by enabling more agile, efficient, and data-driven infrastructure management across global enterprises, SMEs, and specialized industry environments.

The compute performance segment accounted for 39% share in 2025 and is anticipated to grow at a CAGR of 25.3% from 2026 to 2035. This segment maintains a leading position because compute resources form the backbone of digital workloads across cloud, hybrid, and multi-cloud environments. Organizations rely on scalable compute services to manage fluctuating processing requirements, support advanced analytics, and maintain consistent application responsiveness. The ability to dynamically allocate virtualized and containerized resources ensures operational continuity while minimizing latency and resource underutilization, reinforcing the segment's dominance.

The public cloud segment held 57% share in 2025 and is forecast to grow at a CAGR of 25.7% through 2035. Public cloud platforms remain the preferred deployment model due to their scalability, operational flexibility, and cost optimization advantages across geographically distributed enterprises. Businesses favor public cloud environments for centralized performance monitoring, intelligent workload optimization, predictive analytics capabilities, and remote system accessibility. The capacity to scale compute, storage, networking, and application services in real time while integrating seamlessly with existing IT systems continues to drive widespread adoption and market leadership.

United States Performance-on-Demand Subscription Market accounted for 83% share, generating nearly USD 8 billion in 2025, owing to its mature cloud infrastructure, advanced digital ecosystem, and rapid integration of AI-powered performance management solutions. The region benefits from early deployment of predictive workload analytics, automated resource provisioning, and high-speed connectivity frameworks that support efficient and secure IT operations. Strong enterprise technology adoption and continuous investment in cloud innovation further solidify North America's dominant position within the performance-on-demand subscription market.

Major companies operating in the Global Performance-on-Demand Subscription Market include Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP), IBM Cloud, Oracle Cloud, Alibaba Cloud, Salesforce, Siemens, Dassault Systemes, and PTC. Companies in the Performance-on-Demand Subscription Market are strengthening their competitive advantage through continuous platform innovation, AI-driven automation, and ecosystem expansion strategies. Providers are investing heavily in advanced analytics, intelligent workload orchestration, and predictive performance modeling to enhance service differentiation. Strategic partnerships and multi-cloud integrations enable broader market reach and seamless interoperability across enterprise environments. Many vendors are adopting flexible pricing models aligned with usage metrics to attract cost-conscious organizations. In addition, companies emphasize cybersecurity enhancements, compliance certifications, and edge integration capabilities to address complex regulatory and operational demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Services

- 2.2.3 Subscription Model

- 2.2.4 Deployment Mode

- 2.2.5 Cloud Service Model

- 2.2.6 Organization Size

- 2.2.7 Vertical

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Adoption of Cloud & Hybrid IT Environments

- 3.2.1.2 Growing Need for Cost Optimization & IT Spend Transparency

- 3.2.1.3 Expansion of Data-Intensive & AI-Driven Workloads

- 3.2.1.4 Advancements in Automation & Observability Technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cost Predictability Challenges

- 3.2.2.2 Security, Compliance & Vendor Lock-In Risks

- 3.2.3 Market opportunities

- 3.2.3.1 Growing Adoption of AI-Driven Performance Optimization Platforms

- 3.2.3.2 Expansion in Emerging Markets & SME Segment

- 3.2.3.3 Edge-to-Cloud Integration

- 3.2.3.4 Industry-Specific Customization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.: NHTSA & FCC Guidelines

- 3.4.1.2 Canada: Canada & ISED Guidelines

- 3.4.2 Europe

- 3.4.2.1 Germany: Federal Ministry of Transport & Digital Infrastructure

- 3.4.2.2 France: Ministry for the Ecological Transition

- 3.4.2.3 UK: Department for Transport

- 3.4.2.4 Italy: Ministry of Infrastructure & Transport

- 3.4.3 Asia Pacific

- 3.4.3.1 China: Ministry of Industry and Information Technology

- 3.4.3.2 Japan: Ministry of Land, Infrastructure, Transport and Tourism

- 3.4.3.3 South Korea: Ministry of Land, Infrastructure and Transport

- 3.4.3.4 India: Ministry of Road Transport & Highways

- 3.4.4 Latin America

- 3.4.4.1 Brazil: National Transport Agency

- 3.4.4.2 Mexico: Secretariat of Communications and Transportation (SCT)

- 3.4.5 Middle East and Africa

- 3.4.5.1 UAE: Ministry of Industry and Advanced Technology

- 3.4.5.2 Saudi Arabia: Saudi Standards, Metrology and Quality Organization

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Use case scenarios

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Service, 2022 - 2035 ($ Bn)

- 5.1 Key trends

- 5.2 Compute Performance

- 5.3 Storage & Throughput

- 5.4 Network Performance

- 5.5 Database/Analytics Performance

- 5.6 Security Performance Services

Chapter 6 Market Estimates & Forecast, By Subscription Model, 2022 - 2035 ($ Bn)

- 6.1 Key trends

- 6.2 Pay-Per-Use

- 6.3 Tiered Performance

- 6.4 Dynamic Scaling

- 6.5 Hybrid Packages

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($ Bn)

- 7.1 Key trends

- 7.2 Public Cloud

- 7.3 Private Cloud

- 7.4 Hybrid Cloud

Chapter 8 Market Estimates & Forecast, By Cloud Service Model, 2022 - 2035 ($ Bn)

- 8.1 Key trends

- 8.2 IaaS

- 8.3 PaaS

- 8.4 SaaS

- 8.5 FaaS

Chapter 9 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($ Bn)

- 9.1 Key trends

- 9.2 Large Enterprises

- 9.3 SMEs

Chapter 10 Market Estimates & Forecast, By Vertical, 2022 - 2035 ($ Bn)

- 10.1 Key trends

- 10.2 BFSI

- 10.3 Healthcare

- 10.4 Retail & E-commerce

- 10.5 Telecom

- 10.6 IT & Software Services

- 10.7 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($ Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Belgium

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 Singapore

- 11.4.6 South Korea

- 11.4.7 Vietnam

- 11.4.8 Indonesia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 UAE

- 11.6.2 South Africa

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Global Player

- 12.1.1 Alibaba Cloud

- 12.1.2 Amazon Web Services (AWS)

- 12.1.3 Dassault Systemes

- 12.1.4 Google Cloud Platform (GCP)

- 12.1.5 IBM Cloud

- 12.1.6 Microsoft Azure

- 12.1.7 Oracle Cloud

- 12.1.8 PTC

- 12.1.9 Salesforce

- 12.1.10 Siemens

- 12.2 Regional Player

- 12.2.1 ANSYS

- 12.2.2 Baidu Cloud

- 12.2.3 EZ Crusher

- 12.2.4 Hexagon

- 12.2.5 Huawei Cloud

- 12.2.6 Keestrack

- 12.2.7 NEC

- 12.2.8 OverBuilt

- 12.2.9 SAP

- 12.2.10 Tata Consultancy Services

- 12.3 Emerging Players

- 12.3.1 CloudSigma

- 12.3.2 Cohesity

- 12.3.3 DigitalOcean

- 12.3.4 Nutanix

- 12.3.5 OutSystems