PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959314

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959314

Europe Industrial Gearbox Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

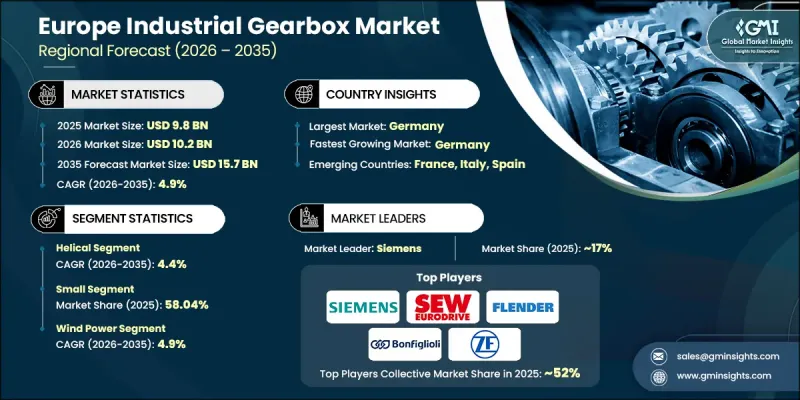

Europe Industrial Gearbox Market was valued at USD 9.8 billion in 2025 and is estimated to grow at a CAGR of 4.9% to reach USD 15.7 billion by 2035.

Growth across the European industrial gearbox industry is being fueled by the rapid shift toward Industry 4.0 and factory automation. As production environments become increasingly digitized, manufacturers are integrating intelligent systems that require highly reliable and performance-driven gearbox solutions. Modern smart factories depend on advanced gear units capable of delivering accurate torque, seamless connectivity, and real-time monitoring compatibility. The need for sensor-enabled gearboxes has intensified as industries prioritize predictive maintenance and operational transparency. In highly automated settings, gearbox reliability directly influences production continuity and synchronized operations. Equipment efficiency and long service life remain central to maintaining competitiveness within Europe's advanced manufacturing ecosystem. Additionally, the transition of the automotive sector toward electric vehicles and evolving mobility solutions continues to create new demand opportunities, further supporting the expansion of the Europe industrial gearbox market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.8 Billion |

| Forecast Value | $15.7 Billion |

| CAGR | 4.9% |

The helical gearbox segment generated USD 3.4 billion in 2025 and is expected to grow at a CAGR of 4.4% from 2026 to 2035. Helical gearboxes maintain a leading position in the European industrial gearbox industry due to their superior power transmission efficiency and smooth mechanical performance. Their angled tooth structure allows quieter operation and consistent load distribution, making them highly suitable for demanding industrial environments. These systems are recognized for managing substantial loads while maintaining stability and minimizing vibration. Their durability and operational lifespan make them a preferred solution for continuous industrial processes requiring dependable torque transfer.

Based on power rating, the small industrial gearbox segment accounted for 58.04% share in 2025 and is forecast to grow at a CAGR of 4.2% through 2035. Small-capacity gearboxes dominate the Europe industrial gearbox market due to their versatility and widespread deployment across manufacturing sectors. Their compact dimensions enable easy installation in machinery where space optimization is essential. With power ratings of up to 500 kW, these gear systems efficiently support ongoing and moderate-duty industrial applications. Increasing regulatory focus on energy-efficient equipment is further accelerating demand for optimized small industrial gearbox solutions across European production facilities.

UK Industrial Gearbox Market reached USD 1.84 billion in 2025 and is projected to grow at a CAGR of 4.9% from 2026 to 2035, maintaining its leading position within Europe. The country benefits from a highly developed manufacturing landscape supported by strong engineering capabilities. Continuous advancements in automotive production stimulate demand for precision-engineered and high-performance gearbox systems. The adoption of Industry 4.0 technologies across German factories is accelerating the integration of intelligent and sensor-compatible transmission solutions. A strong export-oriented industrial base encourages modernization of mechanical systems to meet international quality standards. Additionally, stringent energy efficiency regulations are driving the replacement of outdated gearbox units with technologically advanced alternatives.

Key companies operating in the Europe Industrial Gearbox Market include ABB Ltd, Bonfiglioli Riduttori, Brevini Power Transmission, David Brown Santasalo, Flender GmbH, IG Watteeuw International, Motovario S.p.A., Nord Drivesystems, REDEX, Renold plc, Rossi Group, SEW-EURODRIVE, Siemens, Sumitomo Drive Technologies, and ZF Friedrichshafen. Companies active in the Europe Industrial Gearbox Market are strengthening their market position through product innovation, strategic partnerships, and geographic expansion. Leading manufacturers are investing in research and development to design energy-efficient, sensor-integrated, and application-specific gearbox systems aligned with Industry 4.0 standards. Many players are focusing on customized solutions to address evolving industrial automation requirements. Strategic collaborations with OEMs and automation providers are enhancing product integration capabilities. Firms are also expanding service networks and aftermarket support to build long-term customer relationships. Digital monitoring solutions and predictive maintenance offerings are being incorporated to improve lifecycle value.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Power

- 2.2.4 End Use Industry

- 2.2.5 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Adoption of Industry 4.0 and smart manufacturing technologies

- 3.2.1.2 Automotive sector transformation toward EVs and advanced mobility

- 3.2.1.3 Growth in renewable energy infrastructure

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Stringent environmental and energy efficiency regulations

- 3.2.2.2 Intense price competition from lower-cost regions

- 3.2.3 Opportunities

- 3.2.3.1 Retrofit and modernization of legacy equipment

- 3.2.3.2 Expansion of aftermarket service and predictive maintenance offerings

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Country

- 4.2.1.1 UK

- 4.2.1.2 Germany

- 4.2.1.3 France

- 4.2.1.4 Italy

- 4.2.1.5 Spain

- 4.2.1.6 Rest of Europe

- 4.2.1 By Country

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Helical

- 5.3 Bevel

- 5.4 Worm

- 5.5 Planetary

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Power, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Small (up to 500 kW)

- 6.3 Medium (500 kW to 10 MW)

- 6.4 Large (above 10 MW)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Wind power

- 7.3 Material handling

- 7.4 Construction

- 7.5 Marine

- 7.6 Energy

- 7.7 Transportation

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct

- 8.3 Indirect

Chapter 9 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Europe

- 9.2.1 Germany

- 9.2.2 UK

- 9.2.3 France

- 9.2.4 Italy

- 9.2.5 Spain

Chapter 10 Company Profiles

- 10.1 SEW-EURODRIVE

- 10.2 Flender GmbH

- 10.3 Siemens

- 10.4 ZF Friedrichshafen

- 10.5 Bonfiglioli Riduttori

- 10.6 David Brown Santasalo

- 10.7 Renold plc

- 10.8 Nord Drivesystems

- 10.9 ABB Ltd

- 10.10 Rossi Group

- 10.11 IG Watteeuw International

- 10.12 Motovario S.p.A.

- 10.13 Brevini Power Transmission

- 10.14 Sumitomo Drive Technologies

- 10.15 REDEX