PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959340

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959340

ADAS Subscription Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

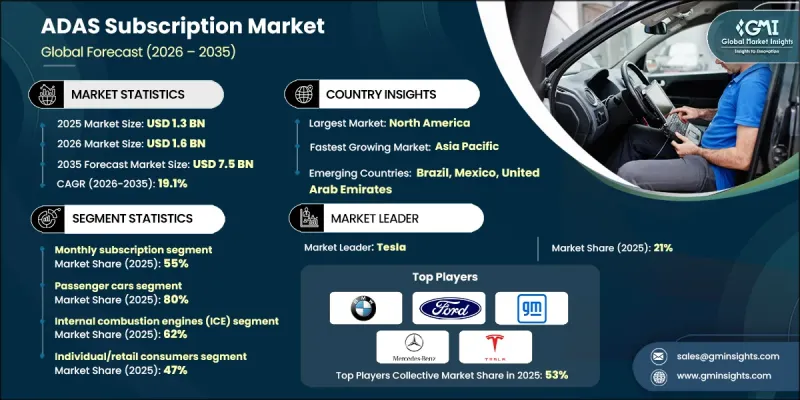

The Global ADAS Subscription Market was valued at USD 1.3 billion in 2025 and is estimated to grow at a CAGR of 19.1% to reach USD 7.5 billion by 2035.

Market growth reflects a structural transformation in the automotive industry, where revenue generation is shifting away from one-time hardware sales toward recurring, software-based monetization. Advanced driver assistance functions are increasingly delivered through subscription-based access rather than permanent activation at purchase. This evolution aligns closely with the rise of software-defined vehicles, where vehicle capabilities are continuously enhanced through over-the-air updates. Automakers are investing heavily in centralized computing and flexible electronic architectures that allow features to be activated, upgraded, or customized post-sale. Regulatory momentum around vehicle safety is further accelerating adoption, as mandated baseline features create opportunities for paid upgrades beyond minimum requirements. Electric vehicles demonstrate higher subscription penetration due to their software-centric platforms and integrated digital ecosystems. Together, consumer demand for advanced safety, regulatory alignment, and digital vehicle strategies is driving sustained expansion of the ADAS subscription market globally.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.3 Billion |

| Forecast Value | $7.5 Billion |

| CAGR | 19.1% |

The market covers paid access to advanced driver assistance functionalities beyond standard regulatory inclusions, offered through recurring payment structures such as monthly plans, annual agreements, and usage-based pricing across passenger and commercial vehicles. Automakers are rapidly transitioning to feature-on-demand models supported by centralized software platforms. Government safety regulations across major regions are increasing the standard installation of ADAS hardware, which in turn enables manufacturers to monetize higher-level features through subscriptions. This regulatory-driven hardware penetration is creating a scalable foundation for software upgrades and recurring revenue streams. Subscription adoption is further supported by the growing preference for flexible ownership models and digital services within the automotive sector.

The monthly subscription plans segment accounted for 55% share in 2025 and is expected to grow at a CAGR of 18.9% from 2026 to 2035. This pricing structure remains dominant due to its flexibility and familiarity among consumers. Monthly plans support ongoing customer interaction and predictable revenue flows for manufacturers while enabling continuous feature enhancements and pricing adjustments. These models also allow automakers to analyze user behavior and engagement patterns to refine offerings. However, retention remains a challenge, with annual churn rates for ADAS subscriptions ranging between 15% and 25%, requiring consistent value delivery and feature differentiation.

The passenger vehicles segment held 80% share in 2025 and is forecast to grow at a CAGR of 18.8%, driven by heightened safety awareness, convenience expectations, and the perceived value of advanced in-vehicle technology. Adoption rates vary significantly across vehicle price categories, with higher penetration in premium models compared to mid-range and entry-level segments. This variation reflects differences in consumer demographics, purchasing power, and the availability of pre-installed ADAS hardware.

United States ADAS Subscription Market generated USD 374 million in 2025 and is expected to grow at a CAGR of 18% from 2026 to 2035. Market leadership is supported by strong regulatory focus on vehicle safety, advanced road infrastructure, and high consumer acceptance of driver assistance technologies. Vehicles equipped with advanced safety systems receive favorable safety assessments, encouraging manufacturers to expand subscription-based feature offerings. Long-distance driving patterns also contribute to demand for enhanced driver assistance capabilities.

Key companies operating in the Global ADAS Subscription Market include Volkswagen, Mercedes-Benz, Ford Motor, General Motors, BMW, Hyundai Motor, Honda Motor, Nissan Motor, Mobileye, and Tesla. Companies in the ADAS subscription market are strengthening their competitive position by investing in software platforms that support scalable, feature-on-demand deployment. Many players are prioritizing centralized vehicle architectures to simplify updates and enable faster rollout of new capabilities. Strategic pricing models, bundled services, and tiered subscription offerings are being used to improve customer retention. Automakers are also focusing on data analytics to understand user behavior and optimize feature design. Partnerships with technology providers, investments in cybersecurity, and continuous enhancement of over-the-air update infrastructure further support long-term market presence and revenue growth.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 Research trail and confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Best estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Subscription Mode

- 2.2.3 Vehicles

- 2.2.4 ADAS Features

- 2.2.5 Autonomy Level

- 2.2.6 Propulsion

- 2.2.7 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for safety & autonomous features

- 3.2.1.2 Shift to software-defined vehicles (SDV)

- 3.2.1.3 OEM revenue diversification & recurring revenue models

- 3.2.1.4 Government mandates for advanced safety systems

- 3.2.1.5 Declining hardware costs & increased software value

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High consumer skepticism & perceived money-grab

- 3.2.2.2 Low market awareness

- 3.2.2.3 High expected pricing concerns

- 3.2.2.4 Cybersecurity & data privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Untapped EV market potential (2x higher adoption rates)

- 3.2.3.2 Emerging markets with leapfrog technology adoption

- 3.2.3.3 Fleet & MaaS provider subscription packages

- 3.2.3.4 Aftermarket subscription services

- 3.2.3.5 AI-powered personalization & usage-based pricing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 US- Federal safety rules & ADAS deployment guidance

- 3.4.1.2 Canada - Safety framework for connected & automated vehicles (CASF)

- 3.4.2 Europe

- 3.4.2.1 Germany- EU ITS & national initiatives

- 3.4.2.2 UK- Post-Brexit ADAS flexibility

- 3.4.2.3 France- National ADAS testing & ITS strategy

- 3.4.2.4 Italy- ITS pilots & smart infrastructure

- 3.4.3 Asia Pacific

- 3.4.3.1 China- MIIT C-V2X mandates & standards

- 3.4.3.2 India- Emerging ADAS & automotive connectivity regulations

- 3.4.3.3 Japan- ITS connect & spectrum policy

- 3.4.3.4 Australia- Technology neutral ITS policies

- 3.4.4 LATAM

- 3.4.4.1 Mexico- NOM vehicle safety standards

- 3.4.4.2 Argentina- National traffic law 24.449

- 3.4.5 MEA

- 3.4.5.1 South Africa- National road traffic act (1996)

- 3.4.5.2 Saudi Arabia- Traffic law & vision 2030 transport initiatives

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Software-defined ADAS architecture

- 3.7.1.2 Over-the-air (OTA) update capabilities

- 3.7.2 Emerging technologies

- 3.7.2.1 Cloud computing & edge processing integration

- 3.7.2.2 AI & machine learning in ADAS subscriptions

- 3.7.1 Current technological trends

- 3.8 Patent analysis

- 3.9 Pricing analysis

- 3.9.1 Monthly vs annual subscription pricing

- 3.9.2 Pay-per-use vs flat-rate models

- 3.9.3 Tiered pricing & feature bundling strategies

- 3.9.4 Regional pricing variations

- 3.10 Use cases & success stories

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Future outlook and opportunities

- 3.12.1 Market evolution scenarios (2025-2035)

- 3.12.2 Emerging subscription models

- 3.12.3 Freemium-to-premium conversion models

- 3.12.4 Disruptive threats & risk mitigation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Subscription Model, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Monthly subscription

- 5.3 Annual subscription

- 5.4 Pay-per-use/on-demand

Chapter 6 Market Estimates & Forecast, By Vehicles, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchbacks

- 6.2.2 SUV

- 6.2.3 Sedan

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles (LCVs)

- 6.3.2 Medium commercial vehicles (MCVs)

- 6.3.3 Heavy commercial vehicles (HCVs)

Chapter 7 Market Estimates & Forecast, By ADAS Features, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Adaptive cruise control (ACC)

- 7.3 Lane keeping/departure systems

- 7.4 Automated parking assist

- 7.5 Collision avoidance systems

- 7.6 Traffic jam assistance

- 7.7 Highway pilot/full self-driving

- 7.8 Blind spot detection

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Autonomy Level, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Level 1 (L1)

- 8.3 Level 2 (L2)

- 8.4 Level 2+ (L2+)

- 8.5 Level 3 (L3)

- 8.6 Level 4 (L4)

Chapter 9 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Internal combustion engine (ICE)

- 9.3 Electric / battery electric vehicles (BEV)

- 9.4 Hybrid electric vehicles (HEV)

- 9.5 Plug-in hybrid electric vehicles (PHEV)

Chapter 10 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 Individual/retail consumers

- 10.3 Fleet operators

- 10.4 Mobility-as-a-service (MaaS) providers

- 10.5 Leasing companies

- 10.6 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Netherlands

- 11.3.8 Sweden

- 11.3.9 Denmark

- 11.3.10 Poland

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Singapore

- 11.4.7 Thailand

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

- 11.6.4 Israel

Chapter 12 Company Profiles

- 12.1 Global Players

- 12.1.1 Audi

- 12.1.2 BMW

- 12.1.3 Ford Motor

- 12.1.4 General Motors

- 12.1.5 Honda Motor

- 12.1.6 Hyundai Motor

- 12.1.7 Mercedes-Benz

- 12.1.8 Nissan Motor

- 12.1.9 Tesla

- 12.1.10 Volkswagen

- 12.2 Regional Players

- 12.2.1 BYD

- 12.2.2 Genesis

- 12.2.3 Li Auto

- 12.2.4 Lucid

- 12.2.5 NIO

- 12.2.6 Polestar Automotive

- 12.2.7 Rivian Automotive

- 12.2.8 Subaru

- 12.2.9 Volvo Cars (Geely)

- 12.2.10 XPENG Motors

- 12.3 Emerging Players & Technology Enablers

- 12.3.1 Mobileye

- 12.3.2 Porsche

- 12.3.3 Sibros Technologies

- 12.3.4 Stellantis

- 12.3.5 Xiaomi