PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959544

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959544

Integrated Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

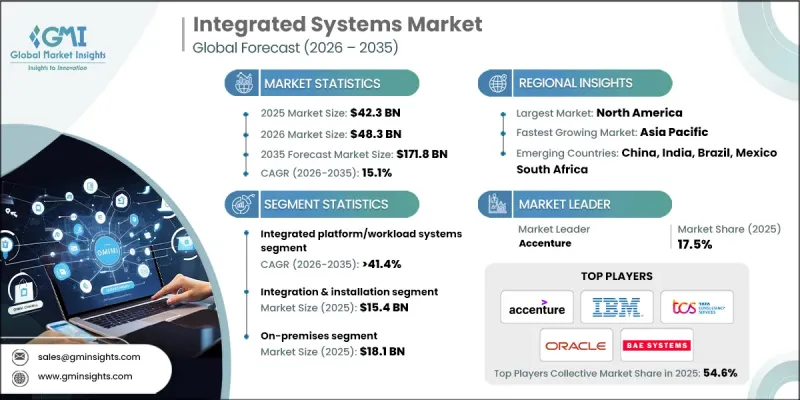

The Global Integrated Systems Market was valued at USD 42.3 billion in 2025 and is estimated to grow at a CAGR of 15.1% to reach USD 171.8 billion by 2035.

Market growth is fueled by the accelerating adoption of integrated solutions across industries seeking to modernize operations, automate complex workflows, and enable seamless interoperability between global systems. Organizations increasingly rely on integrated systems to support large-scale digital transformation initiatives, as these solutions help consolidate fragmented operational structures into unified environments. By connecting IT infrastructure, operational technologies, and data platforms into a single cohesive framework, enterprises improve productivity, reduce process inefficiencies, and gain faster access to actionable insights. Integrated systems reduce reliance on manual processes, enable real-time visibility across departments, and support more informed and timely decision-making. The rising use of AI-driven automation further amplifies demand, as organizations leverage intelligent systems to improve forecasting, predictive maintenance, and operational precision. As enterprises manage growing data volumes and increasingly complex environments, integrated systems play a critical role in enhancing responsiveness, scalability, and overall business agility across manufacturing, services, and enterprise operations.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $42.3 Billion |

| Forecast Value | $171.8 Billion |

| CAGR | 15.1% |

The integrated platform and workload systems segment accounted for a 41.4% share in 2025. This segment leads adoption as organizations favor unified platforms that combine compute, storage, and networking capabilities within a single architecture. These systems simplify workload orchestration, enhance performance consistency, enable real-time processing, and reduce infrastructure complexity. Enterprises increasingly adopt these platforms to streamline IT operations while supporting advanced analytics and digital transformation initiatives across diverse industries.

The on-premises segment generated USD 18.1 billion in 2025 and remained the dominant deployment model. Enterprises continue to prioritize on-premises integrated systems due to their ability to deliver higher levels of control, data security, and customization. These solutions support regulatory compliance, predictable performance, and tailored infrastructure design, making them highly attractive for organizations managing sensitive data and mission-critical operations.

U.S. Integrated Systems Market reached USD 10.7 billion in 2025. Market leadership is supported by sustained investments in advanced IT infrastructure, strong demand for both cloud-based and on-premises solutions, and widespread digital transformation initiatives across sectors. Continuous technological innovation and the presence of major solution providers further reinforce the country's dominant position.

Key companies operating in the Global Integrated Systems Market include IBM Corporation, Accenture, Oracle Corporation, Tata Consultancy Services Limited, Cisco Systems Inc., Hewlett Packard Enterprise, SAP SE, Siemens AG, Fujitsu Limited, Capgemini, Wipro Limited, Infosys Limited, Cognizant, Deloitte Touche Tohmatsu Limited, HCL Technologies, Atos SE, DXC Technology, CGI Inc., Tech Mahindra, NEC Corporation, BAE Systems, Hitachi Ltd. through Vantara, and MDS Systems Integration. Companies in the Integrated Systems Market strengthen their market position through continuous innovation, strategic partnerships, and expansion of end-to-end solution portfolios. Leading players invest heavily in AI-enabled automation, hybrid deployment models, and scalable architectures to address evolving enterprise requirements. Firms focus on industry-specific integrated solutions to meet regulatory, security, and performance needs. Mergers, acquisitions, and collaborations help expand geographic reach and technical expertise.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Service trends

- 2.2.3 Deployment Model trends

- 2.2.4 End-Use trends

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rise in digital transformation initiatives across industries

- 3.2.1.2 Growing adoption of automation, AI, and data analytics

- 3.2.1.3 Increase in cloud computing and hybrid IT environments

- 3.2.1.4 Rising demand for real-time data integration and visibility

- 3.2.1.5 Growing focus on operational efficiency and cost optimization

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial implementation and integration costs

- 3.2.2.2 Complexity of integrating legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of IoT and connected infrastructure

- 3.2.3.2 Growth in smart manufacturing and Industry 4.0 adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Integrated systems Market Estimates & Forecast, By Product, 2022 - 2035 (USD Billion)

- 5.1 Key trends,

- 5.2 Integrated Platform/Workload Systems

- 5.3 Integrated Infrastructure Systems

- 5.4 Other Integrated Systems

Chapter 6 Market Estimates and Forecast, By Service, 2022 - 2035 (USD Billion)

- 6.1 Key trends

- 6.2 Integration & Installation

- 6.3 Consulting

- 6.4 Maintenance & Support

- 6.5 Training

Chapter 7 Integrated systems Market Estimates & Forecast, By Deployment Model, 2022 - 2035 (USD Billion)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

- 7.4 Hybrid

Chapter 8 Integrated systems Market Estimates & Forecast, By End-Use, 2022 - 2035 (USD Billion)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace and Defense

- 8.4 IT and Telecom

- 8.5 BFSI

- 8.6 Healthcare

- 8.7 Oil and Gas

- 8.8 Energy

- 8.9 Manufacturing

- 8.10 Retail

- 8.11 Others

Chapter 9 Integrated systems Market Estimates & Forecast, By Region, 2022 - 2035 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia-Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia-Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Accenture

- 10.2 IBM Corporation

- 10.3 Tata Consultancy Services Limited

- 10.4 Oracle Corporation

- 10.5 BAE Systems

- 10.6 Wipro Limited

- 10.7 Cognizant

- 10.8 Deloitte Touche Tohmatsu Limited

- 10.9 Infosys Limited

- 10.10 MDS Systems Integration (MDS SI)

- 10.11 HCL Technologies

- 10.12 Capgemini

- 10.13 Atos SE

- 10.14 Fujitsu Limited

- 10.15 Cisco Systems, Inc.

- 10.16 Hewlett Packard Enterprise (HPE)

- 10.17 SAP SE

- 10.18 NEC Corporation

- 10.19 Siemens AG

- 10.20 CGI Inc.

- 10.21 DXC Technology

- 10.22 Tech Mahindra

- 10.23 Hitachi, Ltd.(Vantara)