PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959553

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959553

Aerostructures Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

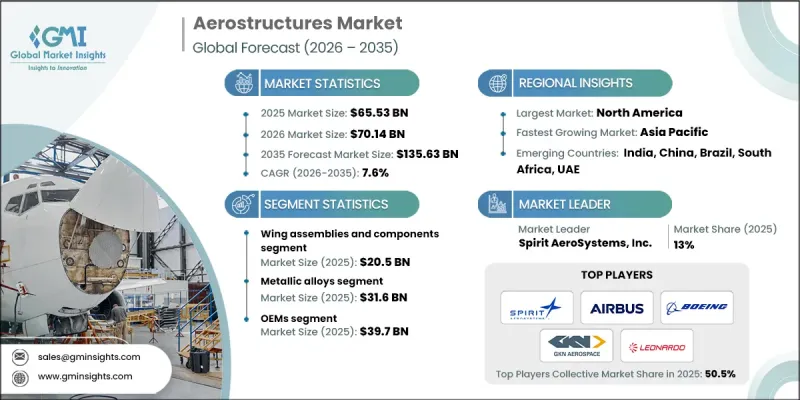

The Global Aerostructures Market was valued at USD 65.53 billion in 2025 and is estimated to grow at a CAGR of 7.6% to reach USD 135.63 billion by 2035.

The market is witnessing sustained expansion driven by rising commercial aircraft production, increasing demand for lightweight and fuel-efficient airframes, and steady growth in global passenger air traffic. Growing defense procurement programs and fleet modernization initiatives are further reinforcing demand for advanced structural components. As airlines expand capacity and replace aging aircraft, original equipment manufacturers require a higher volume of structural assemblies to meet delivery schedules. Long-term passenger traffic growth, supported by expanding middle-class populations, urbanization trends, and improved global connectivity, continues to strengthen aircraft order backlogs. In parallel, maintenance, repair, and overhaul activities are contributing to structural retrofits and upgrades. Technological advancements in materials engineering and precision manufacturing are also reshaping the aerostructures landscape, enabling stronger, lighter, and more efficient airframe components.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $65.53 Billion |

| Forecast Value | $135.63 Billion |

| CAGR | 7.6% |

As passenger volumes rise, airlines are prioritizing next-generation aircraft platforms designed for fuel efficiency and operational optimization. This shift directly increases demand for advanced aerostructures that reduce overall aircraft weight while maintaining structural integrity. The sustained expansion of global air travel provides long-term visibility for manufacturers supplying fuselage sections, empennage systems, and integrated structural modules. Strong order pipelines for commercial jets and military aircraft create stable revenue opportunities for structural component suppliers.

The wing assemblies and components segment reached USD 20.5 billion in 2025. Growing aircraft production rates and modernization programs are accelerating demand for aerodynamically optimized and structurally advanced wing systems. Manufacturers are increasingly focusing on composite integration and automated assembly technologies to enhance performance, precision, and manufacturing efficiency. Investments in advanced fabrication processes are critical to meeting rising production targets while ensuring compliance with safety and durability standards.

The metallic alloys segment accounted for USD 31.6 billion in 2025, maintaining dominance due to its superior fatigue resistance and structural reliability. Metallic materials remain widely utilized in fuselage frames, load-bearing sections, and tail structures across commercial and defense aircraft platforms. Defense programs continue to specify alloy-based components because of their durability and proven certification history under demanding operational conditions. To remain competitive, manufacturers are strengthening alloy processing capabilities and enhancing quality assurance frameworks to meet stringent aerospace requirements.

North America Aerostructures Market held a 42.7% share in 2025, establishing itself as the leading regional market. The region benefits from strong commercial aircraft manufacturing output, substantial defense spending, and a mature aerospace supply chain ecosystem. The presence of major original equipment manufacturers and tier suppliers supports high-value structural production. Regulatory support, sustainability initiatives, and continued investment in advanced manufacturing technologies contribute to increased production efficiency and innovation capacity.

Key players operating in the Global Aerostructures Market include Airbus SE, Spirit AeroSystems, Inc., Boeing Company, GKN Aerospace, Safran S.A., Leonardo S.p.A., Collins Aerospace (RTX Corp.), Mitsubishi Heavy Industries Ltd., Triumph Group, Inc., Stelia Aerospace, Bombardier Inc., Kawasaki Heavy Industries Ltd., RUAG Group, Sonaca Group, and Magellan Aerospace. Companies in the aerostructures market are reinforcing their competitive advantage through automation, material innovation, and strategic partnerships. Leading manufacturers are investing in advanced composite technologies, robotic assembly systems, and digital engineering tools to improve production speed and structural precision. Long-term supply agreements with aircraft OEMs enhance revenue visibility and strengthen collaboration across the value chain. Firms are expanding global manufacturing footprints to optimize costs and reduce supply chain disruptions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Component type trends

- 2.2.2 Material type trends

- 2.2.3 Aircraft type trends

- 2.2.4 End user trends

- 2.2.5 Manufacturing process trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing commercial aircraft production rates

- 3.2.1.2 Rising demand for fuel-efficient and lightweight aircraft structures

- 3.2.1.3 Expansion of global air passenger traffic

- 3.2.1.4 Growth in defense and military aircraft procurement

- 3.2.1.5 Expansion of MRO and aircraft fleet modernization activities

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High manufacturing and material costs

- 3.2.2.2 Supply chain disruptions and capacity constraints

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

- 3.12 Workforce Analysis

- 3.13 Digital Transformation

- 3.14 Mergers, Acquisitions, and Strategic Partnerships Landscape

- 3.15 Risk Assessment and Management

- 3.16 Major Contract Awards (2022 - 2025)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Component Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Fuselage Sections

- 5.3 Wing Assemblies and Components

- 5.4 Empennage (Tail Assemblies)

- 5.5 Flight Control Surfaces

- 5.6 Nacelles and Pylons

- 5.7 Doors, Access Panels and Fairings

Chapter 6 Market Estimates and Forecast, By Material Type, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Composite Materials

- 6.3 Metallic Alloys

- 6.4 Hybrid and Advanced Materials

Chapter 7 Market Estimates and Forecast, By Aircraft Type, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 Commercial Aviation

- 7.3 Military Aviation

- 7.4 Business and General Aviation

- 7.5 Rotorcraft (Helicopters)

- 7.6 Unmanned Aerial Vehicles (UAVs)

- 7.7 Advanced Air Mobility (AAM) / eVTOL

Chapter 8 Market Estimates and Forecast, By Manufacturing Process, 2022 - 2035 (USD Million)

- 8.1 Key Trends

- 8.2 Traditional Manufacturing

- 8.3 Advanced Manufacturing

Chapter 9 Market Estimates and Forecast, By End Users, 2022 - 2035 (USD Million)

- 9.1 Key Trends

- 9.2 OEMs

- 9.3 Aftermarket / MRO

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Spirit AeroSystems, Inc.

- 11.1.2 Airbus SE

- 11.1.3 Boeing Company

- 11.1.4 Safran S.A.

- 11.1.5 Collins Aerospace (RTX Corp.)

- 11.1.6 Leonardo S.p.A.

- 11.1.7 GKN Aerospace

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 Triumph Group, Inc.

- 11.2.1.2 Bombardier Inc.

- 11.2.1.3 Magellan Aerospace

- 11.2.2 Europe

- 11.2.2.1 Stelia Aerospace

- 11.2.2.2 RUAG Group

- 11.2.3 Asia Pacific

- 11.2.3.1 Mitsubishi Heavy Industries Ltd.

- 11.2.3.2 Kawasaki Heavy Industries Ltd.

- 11.2.1 North America

- 11.3 Niche / Disruptors

- 11.3.1 Sonaca Group