PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959554

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959554

Modular and Prefabricated Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

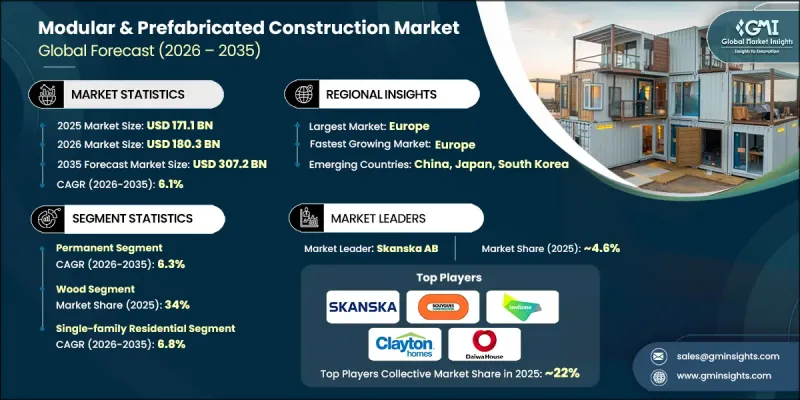

The Global Modular & Prefabricated Construction Market was valued at USD 171.1 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 307.2 billion by 2035.

Accelerating project timelines has become a priority across commercial, residential, and infrastructure sectors, driving demand for modular and prefabricated solutions. Offsite fabrication allows structural components such as walls, floors, and roof systems to be produced simultaneously, enabling quicker project completion. This approach reduces onsite labor requirements, mitigates weather-related delays, and allows owners to utilize properties sooner, ultimately lowering overall construction costs. Standardized modules ensure consistent quality and ease of installation, helping project owners manage budgets and cash flows with greater predictability. Modular construction also supports renovation and expansion projects, allowing upgrades to existing buildings without disrupting daily operations. The efficiency, cost-effectiveness, and flexibility of modular methods are positioning them as a preferred solution in markets seeking faster, high-quality construction outcomes while meeting sustainability and compliance standards.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $171.1 Billion |

| Forecast Value | $307.2 Billion |

| CAGR | 6.1% |

The permanent construction segment generated USD 91.8 billion in 2025 and is expected to grow at a CAGR of 6.3% from 2026 to 2035. Its dominance stems from widespread use in long-term structures such as residential complexes, offices, and institutional facilities. Prefabricated steel, concrete, and engineered timber components enhance durability, structural integrity, and compliance with building regulations while reducing labor and construction time. Rising urbanization, sustainable housing demand, and expansion of commercial infrastructure are fueling adoption.

The wood segment held a 34% share in 2025 and is anticipated to grow at a CAGR of 6.4% from 2026 to 2035. Wood's versatility, sustainability, and aesthetic appeal make it a preferred material for residential, commercial, and institutional projects, supporting rapid assembly and flexible design with lower environmental impact.

Germany Modular & Prefabricated Construction Market reached USD 23.19 billion in 2025, projected to grow at a CAGR of 6.4% through 2035. The market is shaped by strict building codes, energy efficiency regulations, and a shortage of skilled labor, which drive demand for factory-built modules. Prefabrication ensures consistent quality, regulatory compliance, and accelerated project timelines, making it a practical solution for both residential and industrial applications.

Key players in the Global Modular & Prefabricated Construction Market include ACS Group, ATCO Ltd., Bouygues Construction, Boxabl Inc., Clayton Homes, Daiwa House Industry Co., Ltd., Guerdon, LLC, Hickory Group, Kiewit Corporation, Larsen & Toubro Limited, Lendlease Group, Red Sea International Co., Riko Group, Sekisui House, Ltd., and Skanska AB. Companies in the Modular & Prefabricated Construction Market are strengthening their position through strategic investments in offsite manufacturing facilities, standardization of modular components, and adoption of sustainable building materials. Firms are expanding global footprints to access high-demand regions while leveraging digital design and BIM technologies to improve planning and precision. Partnerships with contractors and developers enhance market reach, while R&D initiatives focus on advanced materials, energy-efficient solutions, and rapid assembly techniques.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Burner design

- 2.2.3 Installation

- 2.2.4 Power Range

- 2.2.5 End Use Industry

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for faster project completion and reduced construction timelines

- 3.2.1.2 Expansion of affordable housing and urban infrastructure projects

- 3.2.1.3 Improved quality control through factory-based construction processes

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High upfront investment in manufacturing facilities and logistics

- 3.2.2.2 Design limitations and perception of reduced architectural flexibility

- 3.2.3 Opportunities

- 3.2.3.1 Integration of digital design tools such as BIM and automation

- 3.2.3.2 Growing use of sustainable and low-carbon building materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Permanent

- 5.3 Relocatable

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Steel

- 6.3 Wood

- 6.4 Concrete

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Single family residential

- 7.3 Multi-family residential

- 7.4 Office

- 7.5 Hospitality

- 7.6 Retail

- 7.7 Healthcare

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 ACS Group

- 9.2 ATCO Ltd.

- 9.3 Bouygues Construction

- 9.4 Boxabl Inc.

- 9.5 Clayton Homes

- 9.6 Daiwa House Industry Co., Ltd.

- 9.7 Guerdon, LLC

- 9.8 Hickory Group

- 9.9 Kiewit Corporation

- 9.10 Larsen & Toubro Limited

- 9.11 Lendlease Group

- 9.12 Red Sea International Co.

- 9.13 Riko Group

- 9.14 Sekisui House, Ltd.

- 9.15 Skanska AB