PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959590

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959590

Smart HVAC Controls Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

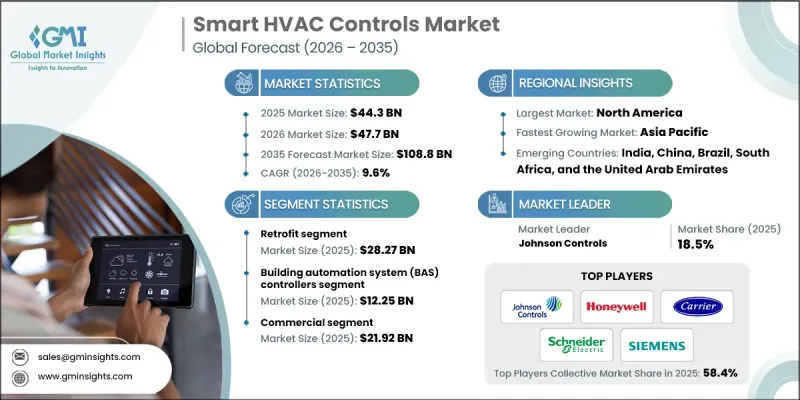

The Global Smart HVAC Controls Market was valued at USD 44.3 billion in 2025 and is estimated to grow at a CAGR of 9.6% to reach USD 108.8 billion by 2035.

Market expansion is driven by the rapid penetration of smart buildings and automated homes, heightened emphasis on reducing energy consumption and operating costs, and stricter government policies centered on sustainability and carbon reduction. Continuous progress in IoT connectivity, artificial intelligence, data analytics, and cloud-based HVAC platforms is reshaping how heating and cooling systems are monitored and optimized. Governments worldwide are actively promoting intelligent building solutions as part of broader environmental and economic strategies. Regulatory frameworks increasingly demand improved energy performance in residential, commercial, and industrial buildings, creating sustained demand for smart HVAC controls that enable precise energy management. Policymakers recognize that improving building efficiency plays a vital role in meeting long-term climate objectives, reinforcing the adoption of intelligent HVAC solutions. The market represents an integrated ecosystem of advanced hardware and software that uses sensors, automation, connectivity, and analytics to manage heating, ventilation, and air conditioning systems with higher accuracy, reliability, and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $44.3 Billion |

| Forecast Value | $108.8 Billion |

| CAGR | 9.6% |

The retrofit segment reached USD 28.27 billion in 2025. Retrofitting allows building owners to upgrade existing HVAC infrastructure with intelligent controls without replacing entire systems, delivering quick efficiency gains while minimizing capital expenditure. This approach is particularly attractive for public institutions and commercial property owners working within budgetary and sustainability constraints. Government-backed building renovation initiatives and efficiency upgrade programs continue to stimulate retrofit activity, reinforcing steady demand for smart HVAC control solutions across aging building stock.

The building automation system controllers segment generated USD 12.25 billion in 2025. These controllers serve as the backbone of intelligent HVAC deployments by enabling centralized control, coordinated operation of multiple building systems, and compliance with evolving energy performance standards. Increasing regulatory emphasis on centralized monitoring and reporting of building energy usage is further strengthening adoption. BAS controllers play a crucial role in optimizing operational efficiency while supporting advanced analytics and automation across large and complex facilities.

North America Smart HVAC Controls Market captured a 39.8% share in 2025. The region benefits from mature smart home adoption, widespread commercial automation, and supportive energy efficiency policies. Incentive programs at both the federal and state levels are accelerating upgrades in existing buildings as well as adoption in new construction. Early deployment of connected thermostats, sensors, and data-driven HVAC platforms across residential, commercial, and industrial sectors continues to reinforce regional leadership while supporting sustainability targets and operational efficiency.

Key companies operating in the Global Smart HVAC Controls Market include Carrier Global Corporation, Honeywell International Inc., Siemens AG, Johnson Controls International plc, Schneider Electric SE, Daikin Industries Ltd., Mitsubishi Electric Corporation, Emerson Electric Co., Bosch Thermotechnology, Trane Technologies plc, Lennox International Inc., LG Electronics Inc., Delta Controls Inc., Distech Controls Inc., KMC Controls Inc., Regin Group, Aprilaire, Carel Industries, Ecobee Inc., and Nest Labs under Google LLC. Companies in the Smart HVAC Controls Market focus on strengthening their market position through continuous product innovation, strategic partnerships, and expansion of digital capabilities. Investments in IoT-enabled platforms, AI-driven analytics, and cloud-based control systems allow suppliers to deliver higher energy savings and predictive maintenance features. Firms actively collaborate with construction companies, utilities, and technology providers to integrate HVAC controls into broader smart building ecosystems. Geographic expansion and localized manufacturing help address regional regulatory requirements and reduce costs.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type trends

- 2.2.2 Application trends

- 2.2.3 Deployment trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of smart buildings and home automation

- 3.2.1.2 Increasing focus on energy efficiency and cost optimization

- 3.2.1.3 Government regulations and sustainability mandates

- 3.2.1.4 Advancements in IoT, AI, and cloud-based HVAC technologies

- 3.2.1.5 Expansion of commercial and industrial infrastructure

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 High initial installation and integration costs

- 3.2.2.2 Data security and privacy concerns

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Sustainability Initiatives

- 3.11 Supply Chain Resilience

- 3.12 Geopolitical Analysis

- 3.13 Digital Transformation

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Smart thermostats

- 5.3 Building automation system (BAS) controllers

- 5.4 Sensors (all types combined)

- 5.5 Actuators & valves

- 5.6 Software & services (cloud platforms, analytics)

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Estimates and Forecast, By Deployment, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 New construction

- 7.3 Retrofit

Chapter 8 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 8.1 Key Trends

- 8.2 Commercial offices

- 8.3 Retail

- 8.4 Healthcare

- 8.5 Education

- 8.6 Hospitality

- 8.7 Data centers

- 8.8 Government & public buildings

- 8.9 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Key Players

- 10.1.1 Honeywell International Inc.

- 10.1.2 Johnson Controls International plc

- 10.1.3 Carrier Global Corporation

- 10.1.4 Emerson Electric Co.

- 10.1.5 Daikin Industries Ltd.

- 10.1.6 Mitsubishi Electric Corporation

- 10.1.7 Bosch Thermotechnology (Robert Bosch GmbH)

- 10.1.8 Siemens AG

- 10.1.9 Schneider Electric SE

- 10.2 Regional Key Players

- 10.2.1 North America

- 10.2.1.1 Aprilaire

- 10.2.1.2 Ecobee Inc.

- 10.2.1.3 Delta Controls Inc.

- 10.2.1.4 Nest Labs (Google LLC)

- 10.2.1.5 Lennox International Inc.

- 10.2.1.6 KMC Controls Inc.

- 10.2.2 Europe

- 10.2.2.1 Carel Industries

- 10.2.2.2 Regin Group

- 10.2.2.3 Distech Controls Inc.

- 10.2.3 Asia Pacific

- 10.2.3.1 LG Electronics Inc.

- 10.2.1 North America

- 10.3 Niche / Disruptors

- 10.3.1 Trane Technologies plc