PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959608

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959608

Industrial Machinery Components and Sensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

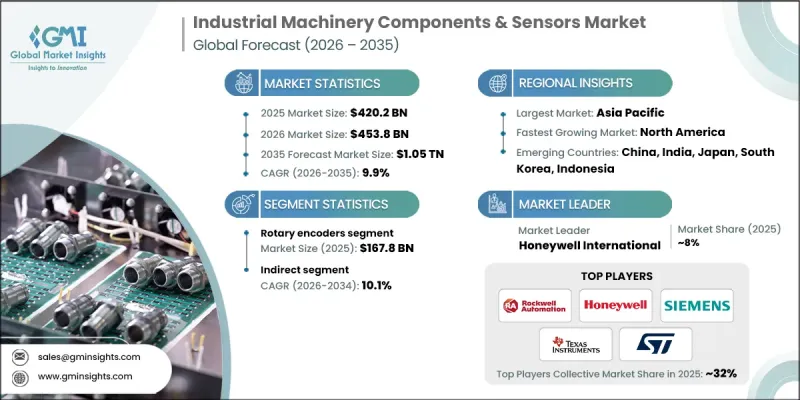

The Global Industrial Machinery Components & Sensors Market was valued at USD 420.2 billion in 2025 and is estimated to grow at a CAGR of 9.9% to reach USD 1.05 trillion by 2035.

Market expansion is propelled by the accelerating adoption of industrial automation and advanced robotics across manufacturing environments. As production facilities prioritize higher throughput, precision, and operational consistency, demand is rising for high-performance components and intelligent sensing systems that enable accurate motion control and real-time performance monitoring. Durable mechanical parts and robust sensors are essential to ensure uninterrupted functionality in automation-intensive settings. Real-time data acquisition supports machine coordination, process optimization, and improved system efficiency. Growing investment in smart factory ecosystems further strengthens the need for interconnected equipment supported by advanced sensing technologies. Industrial operators increasingly rely on automation to minimize manual errors and enhance productivity. In parallel, the growing implementation of predictive maintenance strategies is fueling demand for condition monitoring sensors capable of identifying potential equipment failures before costly downtime occurs, reinforcing long-term market growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $420.2 Billion |

| Forecast Value | $1.05 Trillion |

| CAGR | 9.9% |

The rotary encoders segment generated USD 167.8 billion in 2025 and is forecast to grow at a CAGR of 10.2% between 2026 and 2035. Rotary encoders maintain strong market leadership due to their ability to deliver highly accurate position and speed feedback within automated systems. Their precision enhances motion control efficiency across complex machinery platforms. Consistent demand from robotics, computer-controlled manufacturing equipment, and automated material movement systems continues to support segment expansion. Manufacturers favor rotary encoders for their operational reliability under continuous usage conditions and their compact structure, which simplifies system integration. Ongoing improvements in digital processing capabilities are further elevating resolution accuracy and signal stability, reinforcing their long-term relevance in factory automation.

The automotive segment held 20.54% share in 2025 and is projected to grow at a CAGR of 10.4% through 2035. Vehicle manufacturing relies heavily on automation, driving sustained demand for advanced industrial sensors and precision mechanical components. Motion feedback systems play a vital role in assembly line accuracy and robotic synchronization. The expanding production of electric vehicles is increasing the requirement for advanced sensing technologies and high-performance control solutions. Stringent quality assurance standards across automotive production facilities are further encouraging the adoption of reliable monitoring and feedback mechanisms.

China Industrial Machinery Components & Sensors Market reached USD 55.6 billion in 2025 and is anticipated to grow at a CAGR of 10.4% from 2026 to 2035. Strong manufacturing output and continuous industrial modernization efforts are supporting market expansion. National automation strategies are accelerating the integration of advanced sensor technologies within production infrastructure. High machinery utilization rates create ongoing demand for durable components engineered for long operational life. The development of smart manufacturing ecosystems is increasing the deployment of real-time monitoring systems. Growth in electric mobility and battery production is further strengthening demand for precision sensing and motion control technologies.

Key companies operating in the Global Industrial Machinery Components & Sensors Market include Siemens, Honeywell International, Rockwell Automation, Robert Bosch, Amphenol Corporation, SICK AG, STMicroelectronics, Texas Instruments Incorporated, Denso Corporation, Pepperl+Fuchs, KELLER AG, Merit Sensor Systems, First Sensor, and di-soric GmbH & Co. KG. Companies in the industrial machinery components & sensors market are reinforcing their competitive position through continuous innovation, strategic acquisitions, and expansion of smart automation portfolios. Many industry leaders are investing in advanced sensing technologies, AI-enabled analytics, and IoT-integrated platforms to support predictive maintenance and real-time monitoring. Partnerships with manufacturing OEMs and robotics providers enable deeper system integration and long-term supply agreements. Firms are also strengthening global distribution networks and enhancing customization capabilities to address sector-specific requirements.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component Type

- 2.2.3 End Use Industry

- 2.2.4 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of industrial automation and robotics adoption

- 3.2.1.2 Rising deployment of predictive maintenance solutions

- 3.2.1.3 Implementation of Industry 4.0 and smart manufacturing frameworks

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High integration and installation costs

- 3.2.2.2 Interoperability issues with legacy machinery

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of smart factories and connected ecosystems

- 3.2.3.2 Development of cybersecurity-enabled sensor networks

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Component Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Rotary encoders

- 5.3 Process control sensors

- 5.4 Circuit protection devices

- 5.5 Power and Signal Components

- 5.6 Interface and Control Components

Chapter 6 Market Estimates & Forecast, By End-Use Industry, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Automotive Industry

- 6.3 Electronics and Semiconductor

- 6.4 Food and Beverage

- 6.5 Pharmaceutical and Biotechnology

- 6.6 Energy and Utilities

- 6.7 Aerospace and Defense

- 6.8 Chemical and Process Industries

- 6.9 Mining and Metals

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Direct

- 7.3 Indirect

Chapter 8 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 UAE

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Amphenol Corporation

- 9.2 Denso Corporation

- 9.3 di-soric GmbH & Co. KG

- 9.4 First Sensor

- 9.5 Honeywell International

- 9.6 KELLER AG

- 9.7 Merit Sensor Systems

- 9.8 Pepperl+Fuchs

- 9.9 Robert Bosch

- 9.10 Rockwell Automation

- 9.11 SICK AG

- 9.12 Siemens

- 9.13 STMicroelectronics

- 9.14 Texas Instruments Incorporated