PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959625

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959625

Electric Distribution Utility Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

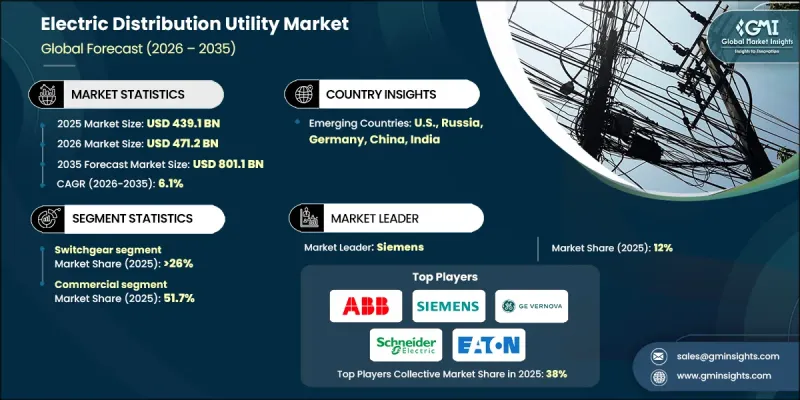

The Global Electric Distribution Utility Market was valued at USD 439.1 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 801.1 billion by 2035.

Growth is supported by increasing capital allocation toward modernizing distribution networks through digitalization, automation, and real-time system visibility. Utilities are strengthening their networks to improve operational efficiency, service reliability, and data-driven planning across distribution assets. Rising electrification across transportation, residential, commercial, and industrial applications is placing higher load requirements at the distribution level, while ongoing infrastructure development across urban and semi-urban regions continues to elevate electricity consumption. Utilities are responding by reinforcing and expanding networks to handle higher capacity requirements and ensure stable power delivery. Changing climate patterns and the need to replace aging electrical components are further accelerating investment in resilient and automated grid technologies. These efforts focus on improving grid stability, reducing outage duration, and enhancing service quality through advanced protection systems, intelligent distribution equipment, and upgraded cabling solutions. The broader transition toward digitally enabled, flexible, and intelligent distribution infrastructure remains a central growth driver for the market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $439.1 Billion |

| Forecast Value | $801.1 Billion |

| CAGR | 6.1% |

The switchgear segment held 26% share in 2025 and is expected to grow at a CAGR of 7% through 2035. Demand is driven by widespread adoption of advanced grid solutions that enhance efficiency across power generation, distribution, and consumption. Large-scale refurbishment of aging infrastructure and continuous expansion of distribution networks across developed and emerging economies are further strengthening the outlook for switchgear deployment.

The industrial end-use segment is projected to grow at a CAGR of 6% by 2035. Expansion of industrial facilities requiring high reliability and power quality is supporting increased demand for distribution infrastructure. Favorable government policies, rising adoption of advanced manufacturing practices, and growing investment in tailored substations and feeder systems are positively influencing market dynamics.

Europe Electric Distribution Utility Market is expected to reach USD 162 billion by 2035. Strong focus on grid modernization, renewable energy integration, and long-term decarbonization goals is driving significant investment in distribution infrastructure. Network expansion, adoption of intelligent grid technologies, and development of advanced industrial capacity continue to strengthen regional growth prospects.

Key companies operating in the Global Electric Distribution Utility Market include Siemens, Schneider Electric, ABB, Hitachi Energy, GE Vernova, Mitsubishi Electric Corporation, Eaton, Enel, Iberdrola, Engie, National Grid, Duke Energy, Southern Company, Siemens Energy, Fuji Electric, Kansai Electric Power, China Yangtze Power, ACWA Power, Lucy Group, Orecco Electric, Coil Innovation, and SGC. Companies in the Electric Distribution Utility Market are reinforcing their market position through large-scale investment in digital grid technologies and infrastructure modernization. Utilities and technology providers focus on automation, advanced analytics, and intelligent equipment to improve reliability and operational efficiency. Strategic partnerships with technology firms help accelerate the deployment of smart distribution solutions. Firms are expanding grid capacity and upgrading legacy assets to support rising electricity demand and the integration of decentralized energy sources. Emphasis on resilience planning, predictive maintenance, and cybersecurity strengthens long-term network performance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research approach

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Component trends

- 2.4 End use trends

- 2.5 Voltage trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Emerging opportunities & trends

- 3.7.1 Digital transformation with IoT technologies

- 3.7.2 Emerging market penetration

- 3.8 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.3.1 Key partnerships & collaborations

- 4.3.2 Major M&A activities

- 4.3.3 Product innovations & launches

- 4.3.4 Market expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Strategic dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Component, 2022 - 2035, (USD Million)

- 5.1 Key trends

- 5.2 Distribution substations

- 5.3 Distribution transformers

- 5.4 Switchgear

- 5.5 Distribution lines and poles

- 5.6 AMI smart meters

- 5.7 Others

Chapter 6 Market Size and Forecast, By End Use, 2022 - 2035, (USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Voltage, 2022 - 2035, (USD Million)

- 7.1 Key trends

- 7.2 Low voltage

- 7.3 Medium voltage

- 7.3.1 Behind the fence

- 7.3.2 Outside the fence

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035, (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 France

- 8.3.3 Russia

- 8.3.4 UK

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 South Korea

- 8.4.4 India

- 8.4.5 Australia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 UAE

- 8.5.3 Egypt

- 8.5.4 South Africa

- 8.6 Latin America

- 8.6.1 Brazil

- 8.6.2 Argentina

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 ACWA Power

- 9.3 China Yangtze Power

- 9.4 Coil Innovation

- 9.5 Duke Energy

- 9.6 Eaton

- 9.7 Enel

- 9.8 Engie

- 9.9 Fuji Electric

- 9.10 GE Vernova

- 9.11 Hitachi Energy

- 9.12 Iberdrola

- 9.13 Kansai Electric Power

- 9.14 Lucy Group

- 9.15 Mitsubishi Electric Corporation

- 9.16 National Grid

- 9.17 Orecco Electric

- 9.18 Schneider Electric

- 9.19 SGC

- 9.20 Siemens

- 9.21 Siemens Energy

- 9.22 Southern Company