PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959636

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959636

IP Camera Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

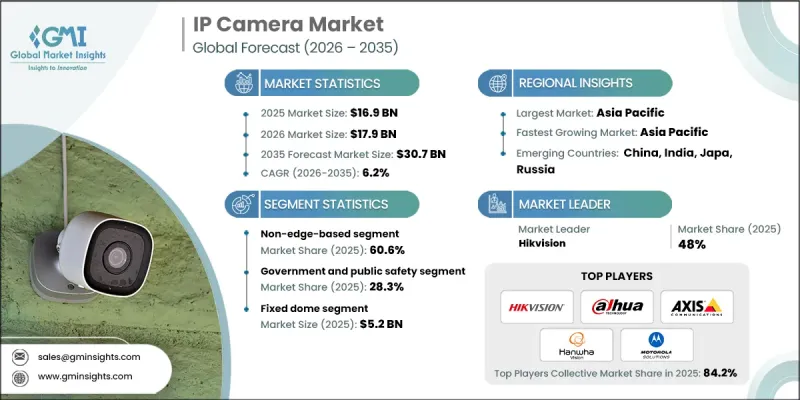

The Global IP Camera Market was valued at USD 16.9 billion in 2025 and is estimated to grow at a CAGR of 6.2% to reach USD 30.7 billion in 2035.

The expansion of the IP camera market is driven by increasing demand for AI-powered video analytics in enterprises, mandatory video surveillance requirements in commercial and transport environments, and the rising adoption of smart home and connected security systems for residential and small business applications. Organizations are increasingly relying on IP cameras to enhance security, improve situational awareness, and enable real-time monitoring. The combination of AI, cloud storage, and edge computing is reshaping surveillance networks, making them more scalable, cost-efficient, and capable of delivering actionable insights. Cloud-based solutions reduce reliance on expensive on-premise infrastructure, while edge-enabled cameras offer localized intelligence, allowing faster decision-making and reducing network congestion. The adoption of AI-driven video analytics is a primary growth factor for the IP camera market. Cloud-based video management systems are increasingly preferred due to their flexibility, lower IT maintenance costs, and scalability. Initiatives such as government-backed programs promoting secure cloud deployment encourage adoption by providing cost-effective, compliant cloud solutions for multi-site surveillance. Edge-based cameras are transforming traditional surveillance architectures by enabling on-device intelligence, reducing latency, and improving real-time response.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $16.9 Billion |

| Forecast Value | $30.7 Billion |

| CAGR | 6.2% |

The non-edge-based systems accounted for 60.6% share in 2025. Centralized systems remain dominant in large-scale government, commercial, and enterprise deployments because they integrate easily with legacy platforms, allow unified monitoring, and meet compliance requirements while being cost-effective for multi-camera networks.

The government and public safety segment held a 28.3% share in 2025. IP cameras play a critical role in city surveillance, border monitoring, law enforcement, and infrastructure protection. Governments are investing heavily in continuous monitoring, incident recording, and real-time intelligence, driving consistent demand for large-scale deployments. Long-term infrastructure projects and stringent public safety regulations support ongoing adoption, ensuring steady growth in this segment.

North America IP Camera Market accounted for 25.1% share in 2025. The region's growth is fueled by investments in critical infrastructure protection, workplace security, and urban safety initiatives. Organizations and governments are increasingly deploying AI-enabled video analytics, cloud-managed surveillance systems, and edge-enabled cameras to improve situational awareness and operational efficiency. The integration of real-time analytics with intelligent video platforms is helping public and private organizations detect threats faster, optimize security operations, and enhance compliance with safety regulations. Strong adoption across transportation, government facilities, retail, and industrial sectors continues to drive the North American market.

Key players in the Global IP Camera Market include Dahua Technology Co., Ltd., Uniview (UNV), Hanwha Vision Co., Ltd., Mobotix AG, Panasonic (i-PRO / Panasonic Security), Hangzhou Hikvision Digital Technology Co., Ltd., Axis Communications AB, IDIS Co., Ltd., Vivotek Inc., Honeywell International Inc., CP Plus, Bosch Security Systems (Bosch GmbH), Motorola Solutions, Inc., and Sony Corporation. Companies in the IP Camera Market strengthen their position through a combination of innovation, strategic partnerships, and regional expansion. They invest heavily in AI and edge computing technologies to enhance analytics, improve performance, and offer scalable cloud-based solutions. Collaborations with government agencies, large enterprises, and system integrators help secure long-term contracts and promote early adoption. Expanding manufacturing and distribution capabilities in emerging markets reduces costs and accelerates delivery. Product differentiation, including high-resolution imaging, cybersecurity enhancements, and integration with smart building platforms, increases competitiveness.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Camera type trends

- 2.2.2 Imaging technology trends

- 2.2.3 Maximum sensor resolution trends

- 2.2.4 Processing architecture trends

- 2.2.5 End-use industry trends

- 2.2.6 Regional trends

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 AI-powered video analytics demand from enterprises and governments

- 3.2.1.2 Mandatory video monitoring regulations in transportation and retail

- 3.2.1.3 Cloud-based video storage reducing on-premise infrastructure costs

- 3.2.1.4 Growing adoption of PoE-enabled network infrastructure

- 3.2.1.5 Expansion of smart homes and connected security ecosystems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Cybersecurity vulnerabilities and frequent IP camera hacking incidents

- 3.2.2.2 High bandwidth and storage costs for high-resolution video

- 3.2.3 Market opportunities

- 3.2.3.1 Edge AI cameras for real-time analytics without cloud dependency

- 3.2.3.2 High-growth demand from emerging Tier-2 and Tier-3 cities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Camera Type, 2022 - 2035

- 5.1 Key trends

- 5.2 Fixed dome

- 5.3 Fixed bullet

- 5.4 Fixed box

- 5.5 Fixed turret

- 5.6 PTZ

- 5.7 Multi-sensor/panoramic

- 5.8 Fisheye

Chapter 6 Market Estimates and Forecast, By Imaging Technology, 2022 - 2035

- 6.1 Key trends

- 6.2 Visible light

- 6.3 Thermal

- 6.4 Bispectral

Chapter 7 Market Estimates and Forecast, By Maximum Sensor Resolution, 2022 - 2035

- 7.1 Key trends

- 7.2 Upto 2MP (including 1080p Full HD)

- 7.3 Above 2MP to 5MP

- 7.4 Above 5MP to 8MP (including 4K Ultra HD)

- 7.5 Above 8MP

Chapter 8 Market Estimates and Forecast, By Processing Architecture, 2022 - 2035

- 8.1 Key trends

- 8.2 Edge

- 8.3 Non-edge

Chapter 9 Market Estimates and Forecast, By End-use Industry, 2022 - 2035

- 9.1 Key trends

- 9.2 Government & public safety

- 9.3 Retail & commercial real estate

- 9.4 Banking & financial services

- 9.5 Transportation & logistics

- 9.6 Healthcare

- 9.7 Education

- 9.8 Industrial & manufacturing

- 9.9 Utilities & energy

- 9.10 Residential

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Hikvision - Hangzhou Hikvision Digital Technology Co., Ltd.

- 11.1.2 Axis Communications AB

- 11.1.3 Dahua Technology Co., Ltd.

- 11.2 Regional key players

- 11.2.1 North America

- 11.2.1.1 Motorola Solutions, Inc.

- 11.2.1.2 Honeywell International Inc.

- 11.2.2 Asia Pacific

- 11.2.2.1 Hanwha Vision Co., Ltd.

- 11.2.2.2 CP Plus

- 11.2.3 Europe

- 11.2.3.1 Bosch Security Systems (Bosch GmbH)

- 11.2.3.2 Mobotix AG

- 11.2.1 North America

- 11.3 Niche Players/Disruptors

- 11.3.1 Vivotek Inc.

- 11.3.2 Uniview (UNV)

- 11.3.3 Sony Corporation

- 11.3.4 Panasonic (i-PRO / Panasonic Security)

- 11.3.5 IDIS Co., Ltd.