PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959650

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959650

Microprocessor Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

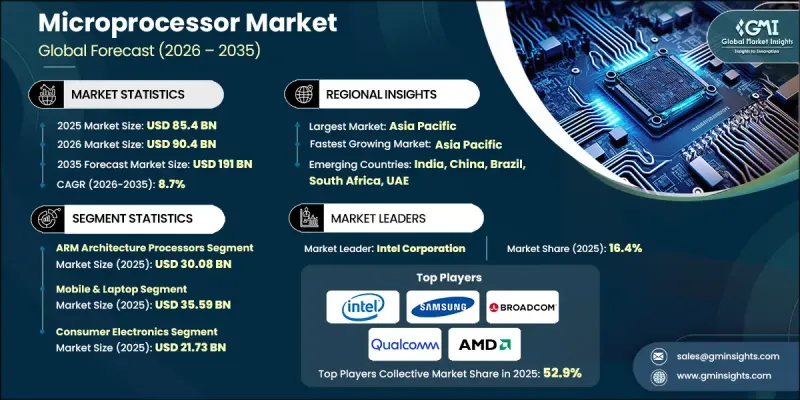

The Global Microprocessor Market was valued at USD 85.4 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 191 billion by 2035.

Market growth is fueled by increasing demand for high-performance computing across diverse industries, alongside the rapid expansion of artificial intelligence, machine learning, and data-driven applications. The continued evolution of automotive electronics and advanced driver assistance technologies is strengthening processor requirements, while the widespread adoption of consumer electronics and connected smart devices is accelerating volume demand. Industrial automation and IoT deployment are also contributing to sustained momentum. Governments worldwide are prioritizing high-performance computing infrastructure to support scientific research, digital transformation, and economic competitiveness. Policy initiatives aimed at strengthening domestic semiconductor ecosystems are further reinforcing growth in consumer electronics and smart device segments. A microprocessor functions as the central processing unit within an electronic system, executing arithmetic, logical, control, and input-output operations by processing instructions. These integrated circuits interpret software and hardware data, enabling computing systems, communication platforms, industrial machinery, automotive systems, and connected technologies to operate efficiently and intelligently.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $85.4 Billion |

| Forecast Value | $191 Billion |

| CAGR | 8.7% |

The ARM architecture processors segment generated USD 30.08 billion in 2025. Strong adoption across mobile devices and energy-efficient electronics has positioned ARM-based processors as a dominant architecture due to their scalability, integration capabilities, and low power consumption. Expanding deployment in automotive electronics, edge computing environments, and industrial IoT systems continues to drive additional demand. Manufacturers are increasingly broadening ARM-based product portfolios to address mobile, IoT, and automotive applications, emphasizing efficiency, integration, and cost optimization.

The mobile and laptop segment reached USD 35.59 billion in 2025. Growing demand for high-performance yet power-efficient processors is being driven by advanced mobile computing requirements and increasingly sophisticated user experiences. The integration of AI-enabled features and graphics-intensive applications is reinforcing the need for processors capable of managing complex workloads while maintaining energy efficiency. Industry participants are focusing on developing processors that balance computational performance, AI acceleration, and graphics capabilities to maintain competitiveness in smartphones and portable computing devices.

North America Microprocessor Market accounted for 22.9% share in 2025. The region continues to serve as a major innovation hub, supported by strong demand from cloud data centers, enterprise computing environments, AI processing workloads, and automotive electrification initiatives. A well-established research and development ecosystem, particularly in the United States, underpins the creation of high-performance and specialized processors. Domestic semiconductor policy initiatives are encouraging localized manufacturing and research investment, enhancing supply chain resilience. The presence of established industry leaders alongside dynamic startup ecosystems further accelerates next-generation processor development and adoption across multiple sectors.

Key companies operating in the Global Microprocessor Market include Advanced Micro Devices, Inc., Analog Devices, Inc., Arm Limited, Broadcom Inc., Seiko Epson Corporation, Intel Corporation, Marvell Technology Group Ltd., Microchip Technology Inc., NXP Semiconductors, Qualcomm Technologies, Inc., Renesas Electronics Corporation, Samsung Electronics Co., Ltd., STMicroelectronics N.V., Texas Instruments Incorporated, Western Design Centre, Infineon Technologies AG, Rockchip Electronics Co., Ltd., IBM Corporation, NVIDIA Corporation, and Nuvoton Technology Corporation. Companies in the Microprocessor Market are strengthening their competitive positioning through continuous innovation, advanced node development, and strategic ecosystem partnerships. Leading players are investing heavily in AI-optimized architectures, heterogeneous computing designs, and energy-efficient chip technologies to meet evolving industry demands. Collaborations with cloud providers, automotive manufacturers, and device OEMs are securing long-term supply relationships. Firms are also expanding fabrication capabilities and leveraging advanced packaging techniques to improve performance and yield. Emphasis on software-hardware integration enhances platform differentiation and customer loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 CPU Architecture Type trends

- 2.2.2 Application trends

- 2.2.3 End-use Industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2026 - 2035 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for high-performance computing across industries

- 3.2.1.2 Proliferation of AI, machine learning, and data-centric applications

- 3.2.1.3 Growth of automotive electronics and advanced driver assistance systems

- 3.2.1.4 Expansion of consumer electronics and smart devices

- 3.2.1.5 Increasing adoption of industrial automation and IoT solutions

- 3.2.2 Pitfalls and challenges

- 3.2.2.1 Supply chain disruptions and geopolitical uncertainties

- 3.2.2.2 High R&D and capital investment requirements

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging Business Models

- 3.9 Compliance Requirements

- 3.10 Supply Chain Resilience

- 3.11 Geopolitical Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Product portfolio comparison

- 4.3.1.1 Product range breadth

- 4.3.1.2 Technology

- 4.3.1.3 Innovation

- 4.3.2 Geographic presence comparison

- 4.3.2.1 Global footprint analysis

- 4.3.2.2 Service network coverage

- 4.3.2.3 Market penetration by region

- 4.3.3 Competitive positioning matrix

- 4.3.3.1 Leaders

- 4.3.3.2 Challengers

- 4.3.3.3 Followers

- 4.3.3.4 Niche players

- 4.3.4 Strategic outlook matrix

- 4.3.1 Product portfolio comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By CPU Architecture Type, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 x86 Architecture Processors

- 5.3 ARM Architecture Processors

- 5.4 RISC-V Architecture Processors

- 5.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Server & Data Center

- 6.3 Desktop & Workstation

- 6.4 Mobile & Laptop

- 6.5 Embedded & IoT

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By End-use Industry, 2022 - 2035 (USD Million)

- 7.1 Key Trends

- 7.2 IT & Cloud Service Providers

- 7.3 Consumer Electronics

- 7.4 Automotive Industry

- 7.5 Industrial & Manufacturing

- 7.6 Telecommunications & Networking

- 7.7 Healthcare & Medical Devices

- 7.8 Aerospace, Defense & Government

- 7.9 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 Intel Corporation

- 9.1.2 Advanced Micro Devices, Inc.

- 9.1.3 NVIDIA Corporation

- 9.1.4 Broadcom Inc.

- 9.1.5 Qualcomm Technologies, Inc.

- 9.1.6 Arm Limited

- 9.1.7 Marvell Technology Group Ltd.

- 9.1.8 Texas Instruments Incorporated

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 Analog Devices, Inc.

- 9.2.1.2 Microchip Technology Inc.

- 9.2.1.3 Western Design Centre

- 9.2.1.4 IBM Corporation

- 9.2.2 Europe

- 9.2.2.1 NXP Semiconductors

- 9.2.2.2 STMicroelectronics N.V.

- 9.2.2.3 Infineon Technologies AG

- 9.2.3 Asia Pacific

- 9.2.3.1 Samsung Electronics Co., Ltd.

- 9.2.3.2 Renesas Electronics Corporation

- 9.2.3.3 Seiko Epson Corporation

- 9.2.1 North America

- 9.3 Niche / Disruptors

- 9.3.1 Rockchip Electronics Co., Ltd.

- 9.3.2 Nuvoton Technology Corporation