PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959664

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1959664

Medical Tourism Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

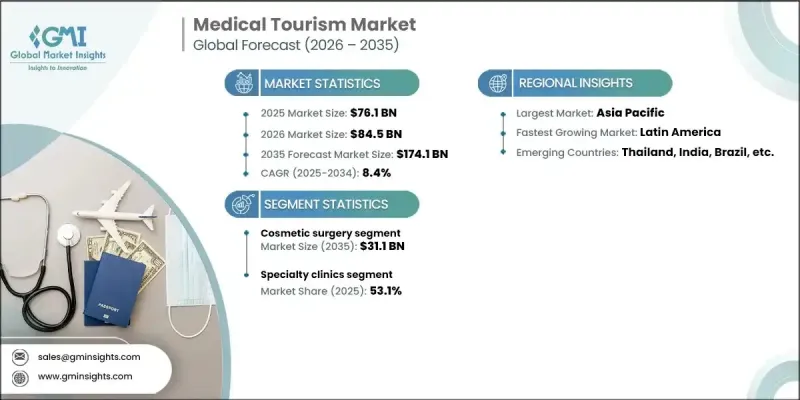

The Global Medical Tourism Market was valued at USD 76.1 billion in 2025 and is estimated to grow at a CAGR of 8.4% to reach USD 174.1 billion by 2035.

The growth is driven by multiple factors, including rising prevalence of chronic diseases, lower treatment costs in developing nations, and increasing compliance with international standards for surgical procedures. Digital pre- and post-treatment care, destination specialization, and bundled service models are making travel for patients less risky, accelerating adoption. High healthcare costs, larger deductibles, and significant out-of-pocket expenses in developed economies continue to push patients to seek care abroad. Telemedicine integration is reducing the need for multiple physical visits while improving continuity between destination specialists and home-based physicians. The post-COVID maturity of telehealth has shifted it from convenience to necessity, with further investments in remote monitoring and secure data sharing expected. Medical tourism spans preventive treatments, elective surgeries, complex procedures, and remote rehabilitation, providing patients with high-quality care at lower costs and reduced wait times.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $76.1 Billion |

| Forecast Value | $174.1 Billion |

| CAGR | 8.4% |

In 2025, the cosmetic surgery segment held a 17.1% share. Global demand for cosmetic procedures remains strong, fueled by procedures such as hair restoration, body contouring, and facial enhancements. Patients are drawn to destinations offering transparent pricing, shorter recovery times, and high perceived value, particularly among self-paying clients. Social media influence and growing awareness of personal appearance continue to drive the popularity of cosmetic surgery, making it a critical component of medical tourism.

The specialty clinics segment accounted for 53.1% share in 2025. These clinics provide focused expertise across therapeutic areas such as fertility, cardiology, oncology, dentistry, orthopedics, and aesthetics. Specialty clinics appeal to medical tourists due to personalized care, shorter wait times, and cost-effective treatment options. Many clinics invest in state-of-the-art technology, minimally invasive procedures, and internationally trained specialists. They offer streamlined processes for international patients, including dedicated coordinators to manage logistics, appointments, and follow-ups, enhancing the overall patient experience.

Asia Pacific Medical Tourism Market reached USD 33.7 billion in 2025, leading in both volume and specialized offerings. Countries in the region, including India, Thailand, Singapore, Malaysia, and South Korea, offer extensive hospital networks, multilingual staff, and destination-specific expertise spanning cardiac, orthopedic, oncology, and aesthetic procedures. Public-private investment in digital health and smart tourism infrastructure has strengthened patient experiences, while telehealth-enabled pre- and post-treatment care programs further enhance accessibility. Accreditation of facilities and integration of wellness services continue to make the region highly attractive for international patients seeking high-quality care at lower costs.

Prominent players in the Global Medical Tourism Market include Bumrungrad International Hospital, Cleveland Clinic, Max Healthcare, St. Luke's Medical Center, Vera Clinic, Fortis Healthcare Limited, Asklepios Kliniken GmbH & Co. KGaA, Raffles Medical Group, Karolinska University Hospital, Apollo Hospitals Group, MANIPAL HEALTH ENTERPRISES PVT LTD, Johns Hopkins Hospital, Mount Elizabeth Hospitals, Mahkota Medical Centre, Shouldice Hospital, Proton Therapy Center, Makati Medical Center, Gleneagles Hospital, Clemenceau Medical Center, and Anadolu Medical Center. Key strategies adopted by companies in the medical tourism market focus on enhancing patient experience, expanding global reach, and maintaining competitive advantages. Providers invest heavily in cutting-edge technology, telemedicine solutions, and digital care platforms to streamline pre- and post-treatment processes. Strategic partnerships with travel agencies, insurance companies, and international facilitators allow for bundled offerings and smoother logistics. Clinics emphasize personalized care, multilingual staff, and international accreditation to build trust. Marketing campaigns highlight affordability, quality, and reduced waiting times, while continuous staff training ensures adherence to global healthcare standards. Expanding specialty services and wellness programs further strengthen market positioning and foster long-term patient loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Application trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Low cost of medical treatment in developing countries

- 3.2.1.2 Growing compliance towards international standards for surgical procedures

- 3.2.1.3 Increasing prevalence of chronic diseases

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Long wait time for certain medical procedures

- 3.2.2.2 Issue with patient follow-up and post-surgery complications

- 3.2.3 Opportunities

- 3.2.3.1 Rise of telemedicine

- 3.2.3.2 Personalized treatment packages

- 3.2.3.3 Growth in cosmetic and elective surgeries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 MEA

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.1.1 AI-powered translation tools

- 3.5.1.2 Digital wellness platforms

- 3.5.1.3 Electronic medical records (EMR) integration

- 3.5.2 Emerging technologies

- 3.5.2.1 Blockchain-based health data security

- 3.5.2.2 AR/VR for medical tourism

- 3.5.1 Current technological trends

- 3.6 Medical coverage scenario

- 3.7 Consumer insights

- 3.8 Number of hospitals by region

- 3.9 Developments and initiatives by country

- 3.10 Demographics of patients/tourists

- 3.11 Investment landscape

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

- 3.15 Future market trends

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 Cosmetic surgery

- 5.2.1 Hair transplant

- 5.2.2 Breast augmentation

- 5.2.3 Other cosmetic surgeries

- 5.3 Cardiovascular surgery

- 5.4 Orthopedic surgery

- 5.4.1 Knee replacement

- 5.4.2 Hip replacement

- 5.4.3 Spinal surgeries

- 5.4.4 Shoulder replacement

- 5.4.5 Ankle replacement

- 5.4.6 Other orthopedic surgeries

- 5.5 Oncology treatment

- 5.5.1 Surgery

- 5.5.2 Radiation therapy

- 5.5.3 Chemotherapy

- 5.5.4 Other therapies

- 5.6 Dental surgery

- 5.6.1 Dental implants

- 5.6.2 Orthodontics

- 5.6.3 Dental cosmetics

- 5.6.4 Dental prosthetics

- 5.6.5 Other dental services

- 5.7 Bariatric surgery

- 5.8 Fertility treatment

- 5.9 Other applications

Chapter 6 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Specialty clinics

- 6.3 Hospitals

- 6.4 Other end use

Chapter 7 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 Spain

- 7.3.4 Poland

- 7.3.5 Turkey

- 7.3.6 Hungary

- 7.3.7 Czech Republic

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Thailand

- 7.4.5 South Korea

- 7.4.6 Singapore

- 7.4.7 Malaysia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Columbia

- 7.5.4 Costa Rica

- 7.6 MEA

- 7.6.1 Saudi Arabia

- 7.6.2 UAE

- 7.6.3 Egypt

Chapter 8 Company Profiles

- 8.1 Anadolu Medical Center

- 8.2 Apollo Hospitals Group

- 8.3 Asklepios Kliniken GmbH & Co. KGaA

- 8.4 Bumrungrad International Hospital

- 8.5 Clemenceau Medical Center

- 8.6 Cleveland Clinic

- 8.7 Fortis Healthcare Limited

- 8.8 Gleneagles Hospital

- 8.9 Johns Hopkins Hospital

- 8.10 Karolinska University Hospital

- 8.11 KPJ Healthcare Berhad

- 8.12 Mahkota Medical Centre

- 8.13 Makati Medical Center

- 8.14 MANIPAL HEALTH ENTERPRISES PVT LTD

- 8.15 Max Healthcare

- 8.16 Mayo Clinic

- 8.17 Mount Elizabeth Hospitals

- 8.18 Narayana Health

- 8.19 Proton Therapy Center

- 8.20 Raffles Medical Group

- 8.21 Samitivej Hospital

- 8.22 Shouldice Hospital

- 8.23 St. Luke's Medical Center

- 8.24 Vera Smile

- 8.25 Vera Clinic