PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982258

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982258

Asia Pacific Single Stage Centrifugal Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

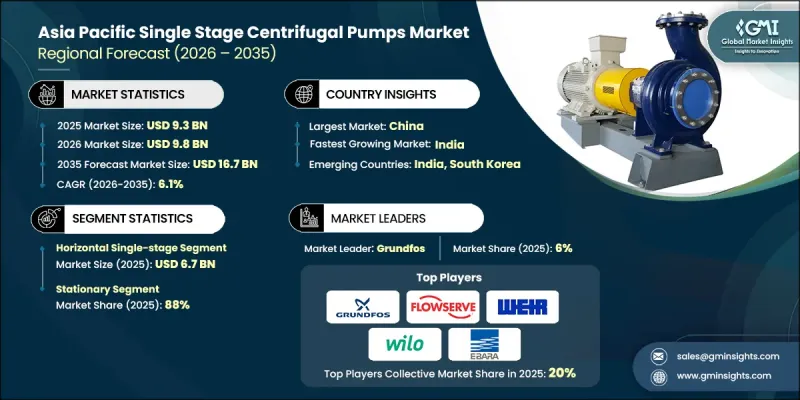

Asia Pacific Single Stage Centrifugal Pumps Market was valued at USD 9.3 billion in 2025 and is estimated to grow at a CAGR of 6.1% to reach USD 16.7 billion by 2035.

Growth in the Asia Pacific single-stage centrifugal pumps industry is being fueled by accelerating industrialization, rapid urban expansion, and continuous investment in essential infrastructure. As economies across the region modernize their water management networks and industrial facilities, demand for dependable liquid transfer solutions continues to climb. Expanding development across manufacturing, utilities, and energy sectors is reinforcing the need for efficient and durable pumping systems. At the same time, operators are prioritizing equipment that balances operational simplicity with long-term reliability. Rising awareness of energy consumption is also influencing procurement decisions, encouraging the adoption of pumps designed to deliver consistent performance while controlling operating costs. Manufacturers are responding by refining product engineering, enhancing durability, and integrating practical performance features without adding unnecessary complexity. This evolving landscape positions single-stage centrifugal pumps as a critical component in supporting infrastructure upgrades, industrial productivity, and sustainable resource management throughout the region.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $9.3 Billion |

| Forecast Value | $16.7 Billion |

| CAGR | 6.1% |

In 2025, the horizontal single-stage pumps accounted for USD 6.7 billion. Their widespread adoption is linked to straightforward configuration, simplified alignment, and ease of servicing. These pumps are engineered for stable installation, offer convenient access to internal components, and support efficient maintenance practices, making them highly suitable for continuous-duty operations across diverse facilities.

The stationary segment held 88% share in 2025. Fixed-installation pumps remain the preferred choice for operations requiring consistent, uninterrupted performance over extended periods. Their robust construction, structural strength, and operational dependability make them ideal for permanent setups where reliability and endurance are essential.

China Single Stage Centrifugal Pumps Market held 35% share, generating USD 3.3 billion in 2025. The region overall continues to present strong growth potential, supported by expanding industrial bases, infrastructure modernization, and sustained investment momentum. Emerging economies such as China and India are contributing significantly to regional demand, driven by ongoing development initiatives and increasing capacity expansion across multiple sectors.

Key companies operating in the Asia Pacific Single Stage Centrifugal Pumps Market include Andritz AG, Ebara Corporation, Flowserve Corporation, Grundfos, ITT Inc., Kirloskar Brothers Limited, KSB Group, Pentair PLC, Shakti Pumps (India) Ltd., SPX Flow, Inc., Sulzer Ltd., Torishima Pump Manufacturing Co., Ltd., Weir Group PLC, Wilo SE, and Xylem Inc. Companies in the Asia Pacific Single Stage Centrifugal Pumps Market are strengthening their competitive position through product innovation, regional expansion, and strategic collaborations. Manufacturers are investing in research and development to improve hydraulic efficiency, reduce lifecycle costs, and enhance equipment durability. Many players are expanding local manufacturing capabilities to shorten delivery timelines and improve after-sales service responsiveness. Partnerships with engineering firms and infrastructure developers are helping companies secure large-scale supply contracts. Businesses are also focusing on digital monitoring solutions and performance optimization technologies to differentiate their offerings.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Design

- 2.2.3 Type

- 2.2.4 Operation

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of water and wastewater infrastructure across apac

- 3.2.1.2 Industrial growth and modernization

- 3.2.1.3 Rising preference for energy-efficient and easy-to-operate equipment

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competition from low-cost local manufacturers

- 3.2.2.2 Variations in infrastructure maturity across countries

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of smart and automated pump systems

- 3.2.3.2 Expansion of agriculture and irrigation projects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By product type

- 3.9 Regulatory landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Design, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Horizontal centrifugal pump

- 5.3 Vertical centrifugal pump

Chapter 6 Market Estimates & Forecast, By Type, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Portable

- 6.3 Stationary

Chapter 7 Market Estimates & Forecast, By Operation, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Electric-driven pump

- 7.3 Engine-driven pump

Chapter 8 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Firefighting application

- 8.4 Building & construction

- 8.5 Oil & gas

- 8.6 General industries

- 8.7 Water & wastewater treatment

- 8.8 Chemicals

- 8.9 Power generation

- 8.10 Others (agriculture etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Asia Pacific

- 10.2.1 China

- 10.2.2 Japan

- 10.2.3 India

- 10.2.4 South Korea

- 10.2.5 Australia

- 10.2.6 Malaysia

- 10.2.7 Indonesia

Chapter 11 Company Profiles

- 11.1 Andritz AG

- 11.2 Ebara Corporation

- 11.3 Flowserve Corporation

- 11.4 Grundfos

- 11.5 ITT Inc.

- 11.6 Kirloskar Brothers Limited

- 11.7 KSB Group

- 11.8 Pentair PLC

- 11.9 Shakti Pumps (India) Ltd.

- 11.10 SPX Flow, Inc.

- 11.11 Sulzer Ltd.

- 11.12 Torishima Pump Manufacturing Co., Ltd.

- 11.13 Weir Group PLC

- 11.14 Wilo SE

- 11.15 Xylem Inc.