PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019037

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 2019037

North America Single Stage Centrifugal Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

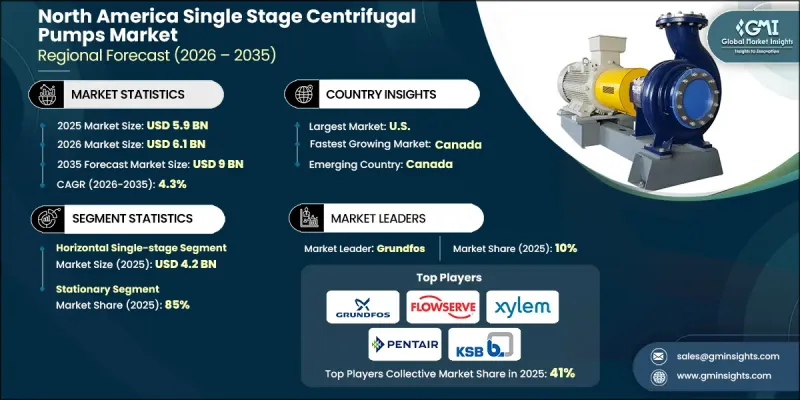

North America Single Stage Centrifugal Pumps Market was valued at USD 5.9 billion in 2025 and is estimated to grow at a CAGR of 4.3% to reach USD 9 billion by 2035.

The North America single stage centrifugal pumps market is shaped by operational shifts across multiple industries, where efficiency, dependability, and simplified system integration remain top priorities. These pumps continue to be widely selected due to their straightforward design, durability, and ease of servicing. Market participants are increasingly focusing on developing solutions that support energy-efficient performance while remaining adaptable to both conventional and digitally enabled environments. As organizations upgrade aging systems, the demand for equipment that delivers consistent output with minimal operational complexity is increasing. The integration of monitoring technologies and the need for uninterrupted performance are further influencing product development, positioning these pumps as essential components in industrial fluid handling systems.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.9 Billion |

| Forecast Value | $9 Billion |

| CAGR | 4.3% |

The North America single stage centrifugal pumps market is also witnessing a growing emphasis on operational continuity and maintenance efficiency. Companies are prioritizing equipment that reduces service interruptions and supports predictive maintenance through digital integration. This trend is encouraging manufacturers to enhance product reliability while incorporating advanced performance features. Additionally, the need for efficient water and fluid management remains a critical factor driving steady demand across the market. Industry participants are seeking solutions that balance long-term durability with cost efficiency, ensuring consistent adoption even during periods of fluctuating industrial activity.

In 2025, the horizontal single stage centrifugal pumps segment reached USD 4.2 billion in revenue. This configuration remains widely preferred due to its practical design and compatibility with a broad range of industrial requirements. The alignment of components along a horizontal axis simplifies installation and reduces operational challenges, contributing to its widespread use. These pumps are recognized for their adaptability across multiple operational environments and their ability to maintain stable performance. Their functional versatility and ease of handling make them a reliable choice for continuous fluid movement applications within the North America single stage centrifugal pumps market.

The stationary segment accounted for 85% share in 2025, reflecting its strong position within the industry. Stationary systems are valued for their structural stability, extended operational life, and seamless integration with large-scale infrastructure. Their design enables them to handle higher capacities and sustained workloads, making them essential for facilities requiring dependable and consistent fluid transfer. Once installed, these systems become a core part of operational processes, reinforcing their importance in long-term industrial applications.

United States Single Stage Centrifugal Pumps Market held a 77% share in 2025 and generated USD 4.6 billion. The country continues to lead due to its well-established industrial ecosystem and ongoing demand for efficient pumping systems across key sectors. Continuous system upgrades are encouraging the adoption of solutions that offer improved performance and easier maintenance without extensive infrastructure changes. A strong distribution network further enhances product accessibility, ensuring timely service and component availability. Regulatory requirements related to operational efficiency and environmental standards are also contributing to consistent replacement and upgrade cycles across facilities.

Major companies operating in the North America Single Stage Centrifugal Pumps Market include Andritz AG, Armstrong Fluid Technology, Cornell Pump Company, Ebara Corporation, Flowserve Corporation, Grundfos, ITT Inc., Kirloskar Brothers Limited, KSB Group, Pentair PLC, SPX Flow, Inc., Sulzer Ltd., Weir Group PLC, Wilo SE, and Xylem Inc. Companies in the North America Single Stage Centrifugal Pumps Market are strengthening their competitive position through innovation, strategic partnerships, and product differentiation. They are investing in research and development to enhance pump efficiency, improve durability, and integrate smart monitoring capabilities. Collaborations with system integrators and industrial operators are enabling broader adoption and smoother deployment of advanced solutions. Market players are also focusing on expanding their distribution networks and after-sales services to improve customer engagement and retention. Additionally, digitalization, including predictive maintenance and remote monitoring, is becoming a key strategy to deliver value-added services. These approaches help companies maintain a strong foothold while addressing evolving customer expectations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Country

- 2.2.2 Design

- 2.2.3 Type

- 2.2.4 Operation

- 2.2.5 End Use Industry

- 2.2.6 Distribution Channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of water and wastewater infrastructure

- 3.2.1.2 Industrial growth and modernization

- 3.2.1.3 Rising preference for energy-efficient and easy-to-operate equipment

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High competition from low-cost local manufacturers

- 3.2.2.2 Variations in infrastructure maturity across countries

- 3.2.3 Opportunities

- 3.2.3.1 Growing adoption of smart and automated pump systems

- 3.2.3.2 Expansion of agriculture and irrigation projects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Major market trends and Disruptions

- 3.5 Future market trends

- 3.6 Risk and mitigation Analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By product type

- 3.9 Regulatory landscape

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Design, 2022-2035 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Horizontal centrifugal pump

- 5.3 Vertical centrifugal pump

Chapter 6 Market Estimates & Forecast, By Type, 2022-2035 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Portable

- 6.3 Stationary

Chapter 7 Market Estimates & Forecast, By Operation, 2022-2035 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Electric-driven pump

- 7.3 Engine-driven pump

Chapter 8 Market Estimates & Forecast, By End Use, 2022-2035 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Mining

- 8.3 Firefighting application

- 8.4 Building & construction

- 8.5 Oil & gas

- 8.6 General industries

- 8.7 Water & wastewater treatment

- 8.8 Chemicals

- 8.9 Power generation

- 8.10 Others (agriculture etc.)

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct

- 9.3 Indirect

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

Chapter 11 Company Profiles

- 11.1 Andritz AG

- 11.2 Armstrong Fluid Technology

- 11.3 Cornell Pump Company

- 11.4 Ebara Corporation

- 11.5 Flowserve Corporation

- 11.6 Grundfos

- 11.7 ITT Inc.

- 11.8 Kirloskar Brothers Limited

- 11.9 KSB Group

- 11.10 Pentair PLC

- 11.11 SPX Flow, Inc.

- 11.12 Sulzer Ltd.

- 11.13 Weir Group PLC

- 11.14 Wilo SE

- 11.15 Xylem Inc.