PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982272

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982272

U.S. Ultra-Luxury Home Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

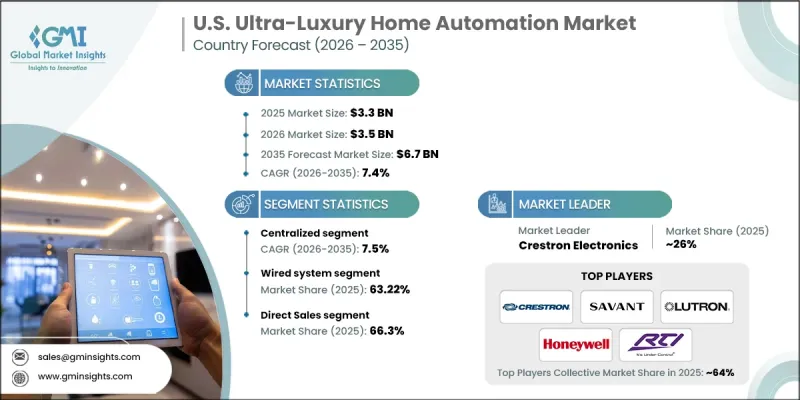

U.S. Ultra-Luxury Home Automation Market was valued at USD 3.3 billion in 2025 and is estimated to grow at a CAGR of 7.4% to reach USD 6.7 billion by 2035.

Growth in ultra-premium residential construction is playing a central role in shaping market demand. The rise in high-value housing developments is generating strong interest in fully integrated, high-performance smart home ecosystems. Developers are increasingly embedding advanced automation infrastructure during the construction phase to meet the sophisticated expectations of affluent buyers. Ultra-luxury residences are designed to deliver elevated living experiences through intelligent control of lighting, climate management, security, and entertainment systems. Because these properties often feature expansive layouts and multiple living zones, integrated automation platforms enable efficient management of complex architectural designs. In a highly competitive luxury real estate landscape, advanced automation serves as a major differentiator, reinforcing exclusivity and long-term property value. As the inventory of premium villas and custom-built estates continues to expand, the adoption of comprehensive home automation installations is rising proportionally, reflecting buyer preference for seamless, technology-driven living environments.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $3.3 Billion |

| Forecast Value | $6.7 Billion |

| CAGR | 7.4% |

The centralized segment generated USD 1.6 billion in 2025 and is expected to grow at a CAGR of 7.5% between 2026 and 2035. Centralized automation systems maintain a leading position in the U.S. ultra-luxury home automation market due to their advanced integration capabilities. Unified control hubs enable synchronized operation of multiple subsystems within large residences, ensuring smooth coordination across distinct zones. High-net-worth homeowners prioritize dependable performance and highly customized automation experiences. Consolidated platforms also minimize compatibility concerns while enhancing overall system efficiency and operational consistency.

The wired system segment accounted for 63.22% share in 2025 and is projected to grow at a CAGR of 6.8% during 2026-2035. Wired infrastructure remains the preferred choice in ultra-luxury properties because of its reliability and consistent connectivity. Structured cabling supports uninterrupted data transmission across architecturally sophisticated homes, enabling advanced automation functions without signal instability. Property owners in this segment value enhanced cybersecurity, reduced interference risks, and superior responsiveness. Seamless compatibility between wired frameworks and centralized control platforms further strengthens system stability and performance.

Key companies operating in the U.S. Ultra-Luxury Home Automation Market include Crestron Electronics, Savant Systems, Lutron Electronics, Honeywell International, Vivint Smart Home, Remote Technologies Inc., Leviton Manufacturing Co., Universal Remote Control, Integrated AV, Heyo Smart, Liaison Technology Group, Smart Systems of Texas, The HomeWorks Group, Digital Interiors, and J.J. Orion. Companies in the U.S. Ultra-Luxury Home Automation Market are reinforcing their competitive positioning through continuous technological innovation and premium service offerings. Leading players are investing in advanced integration platforms that unify lighting, climate, security, and entertainment into highly personalized ecosystems. Strategic collaborations with luxury real estate developers and custom home builders are expanding early-stage system adoption. Firms are also emphasizing bespoke design, white-glove installation services, and long-term maintenance contracts to strengthen client loyalty. Ongoing upgrades in cybersecurity, AI-driven automation, and intuitive user interfaces are enhancing system value propositions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Automation Type

- 2.2.3 Technology Type

- 2.2.4 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 High disposable incomes among affluent homeowners

- 3.2.1.2 Mature luxury real estate sector with smart integration demand

- 3.2.1.3 Rapid technological innovation in smart ecosystems

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High upfront costs and installation complexity

- 3.2.2.2 Data security and privacy concerns

- 3.2.3 Opportunities

- 3.2.3.1 AI and predictive automation integration

- 3.2.3.2 Partnerships with luxury real estate and interior design firms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By country

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Lighting devices

- 5.2.1 In-wall modules/ smart bulbs

- 5.2.2 Smart switches

- 5.2.3 Smart plugs

- 5.2.4 Others (smart dimmer etc.)

- 5.3 Smart security devices

- 5.3.1 Motion/arrival sensor

- 5.3.2 Door/window sensor

- 5.3.3 Alarms

- 5.3.4 Smart wireless bells

- 5.3.5 Smart door locks

- 5.3.6 Others (security cameras etc.)

- 5.4 Entertainment devices

- 5.4.1 Speakers/ audio distribution

- 5.4.2 Video distribution

- 5.4.3 Others (virtual personal assistant etc.)

- 5.5 Protection sensors

- 5.5.1 Flood/fire sensors

- 5.5.2 UV sensors

- 5.5.3 Others (humidity sensors etc.)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Automation Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Distributed

- 6.3 Centralized

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Wired system

- 7.3 Wireless system

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Aurum HomeTech

- 9.3 Control4

- 9.4 Crestron Electronics

- 9.5 Ecobee

- 9.6 Heyo Smart

- 9.7 Honeywell International

- 9.8 Johnson Controls

- 9.9 Legrand

- 9.10 Lutron Electronics

- 9.11 Savant Systems

- 9.12 Schneider Electric

- 9.13 Siemens

- 9.14 Vivint Smart Home