PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982297

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982297

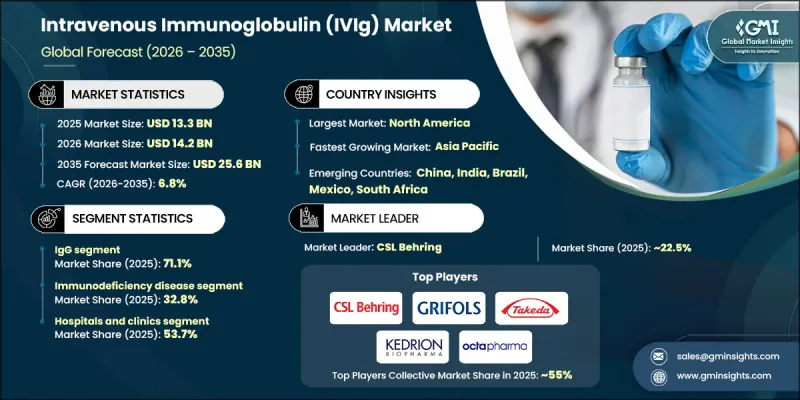

Intravenous Immunoglobulin (IVIg) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

The Global Intravenous Immunoglobulin (IVIg) Market was valued at USD 13.3 billion in 2025 and is estimated to grow at a CAGR of 6.8% to reach USD 25.6 billion by 2035.

The market is propelled by the rising incidence of both primary and secondary immunodeficiency disorders worldwide. IVIg products are sterile, concentrated antibody formulations derived from pooled human plasma, administered via intravenous infusion to provide passive immunity. They support the immune system by supplying ready-made antibodies that neutralize harmful pathogens and regulate immune responses. The therapeutic applications of IVIg have expanded beyond primary immunodeficiencies, increasingly addressing autoimmune and neurological disorders such as chronic inflammatory demyelinating polyneuropathy, Guillain-Barre syndrome, and myasthenia gravis. To meet global demand, leading manufacturers are rapidly expanding plasma collection centers, investing in advanced plasmapheresis equipment, and adopting regional plasma sourcing strategies. Increasing clinical adoption, combined with steady supply chain investments, is shaping a robust growth trajectory for the Intravenous Immunoglobulin (IVIg) Market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.3 Billion |

| Forecast Value | $25.6 Billion |

| CAGR | 6.8% |

The IgG segment held a 71.1% share in 2025, driven by its broad clinical acceptance and key role in immune defense. IgG is the most prevalent immunoglobulin in circulation, making it the preferred choice for treating both primary and secondary immunodeficiencies. Its demand spans multiple specialties, including neurology, hematology, and internal medicine, reinforced by well-established regulatory and manufacturing standards.

The immunodeficiency disease segment accounted for 32.8% share in 2025 and is expected to grow at a CAGR of 6.9% during 2026-2035. This segment encompasses primary immunodeficiencies, secondary immunodeficiencies, hypogammaglobulinemia, and specific antibody deficiencies. Lifelong and chronic in nature, these conditions require frequent IVIg infusions, ensuring sustained market demand.

North America Intravenous Immunoglobulin (IVIg) Market held 52.5% share in 2025, supported by advanced healthcare infrastructure, high prevalence of autoimmune and immunodeficiency disorders, robust reimbursement systems, and an established plasma collection network. The presence of leading pharmaceutical companies, ongoing clinical research, and early adoption of innovative treatment protocols further strengthen market maturity in the region.

Key players in the Global Intravenous Immunoglobulin (IVIg) Market include Baxter International, CSL Behring, Octapharma AG, Grifols SA, Pfizer, Takeda Pharmaceutical Company, ADMA Biologics, Biotest, China Biologics Products, Omrix Biopharmaceuticals (Johnson & Johnson), LFB Biotechnologies, Kedrion Biopharma, Intas Pharmaceuticals, and Shanghai RAAS Blood Products. To strengthen the Intravenous Immunoglobulin (IVIg) Market position, companies are focusing on expanding plasma collection and fractionation capacities, investing in state-of-the-art plasmapheresis equipment, and developing regional sourcing strategies to ensure a stable supply of raw materials. They are also diversifying their product portfolios to target autoimmune and neurological disorders, while optimizing manufacturing processes to reduce costs and enhance efficiency. Strategic partnerships with hospitals, specialty clinics, and healthcare networks expand distribution channels.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research approach

- 1.3 Quality commitments

- 1.3.1 GMI AI policy and data integrity commitment

- 1.3.1.1 Source consistency protocol

- 1.3.1 GMI AI policy and data integrity commitment

- 1.4 Research trail and confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.6.1.1 Sources, by region

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Revenue share analysis

- 1.7.2 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

- 1.9.1 Source attribution framework

- 1.9.2 Quality assurance metrics

- 1.9.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of immunodeficiency disorders

- 3.2.1.2 Increasing geriatric population

- 3.2.1.3 Growing advances in plasma collection, fractionation, and purification technologies

- 3.2.1.4 Rising clinical applications of IVIg in neurological and autoimmune disorders

- 3.2.1.5 Increasing healthcare expenditure for immunoglobulins

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of IVIg therapy

- 3.2.2.2 Potential adverse effects and allergic reactions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of recombinant immunoglobulins

- 3.2.3.2 Rising demand in emerging economies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Future market trends

- 3.8 Pipeline analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022 - 2035 ($ Mn)

- 5.1 Key trends

- 5.2 IgG

- 5.3 IgA

- 5.4 IgM

- 5.5 IgD

- 5.6 IgE

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

- 6.1 Key trends

- 6.2 Immunodeficiency diseases

- 6.2.1 Primary immunodeficiencies

- 6.2.2 Secondary immunodeficiencies

- 6.2.3 Hypogammaglobulinemia

- 6.2.4 Specific antibody deficiency

- 6.3 Chronic Inflammatory demyelinating polyneuropathy (CIDP)

- 6.4 Myasthenia gravis

- 6.5 Multifocal motor neuropathy

- 6.6 Idiopathic thrombocytopenic purpura (ITP)

- 6.7 Inflammatory myopathies

- 6.8 Guillain-Barre syndrome

- 6.9 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Homecare settings

- 7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 ADMA Biologics

- 9.2 Baxter International

- 9.3 Biotest

- 9.4 CSL Behring

- 9.5 China Biologics Products

- 9.6 Grifols SA

- 9.7 Intas Pharmaceuticals

- 9.8 Kedrion Biopharma

- 9.9 LFB Biotechnologies

- 9.10 Omrix Biopharmaceuticals (Johnson & Johnson)

- 9.11 Octapharma AG

- 9.12 Pfizer

- 9.13 Shanghai RAAS Blood Products

- 9.14 Takeda Pharmaceutical Company