PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982323

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982323

Lithium-Ion Battery Recycling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

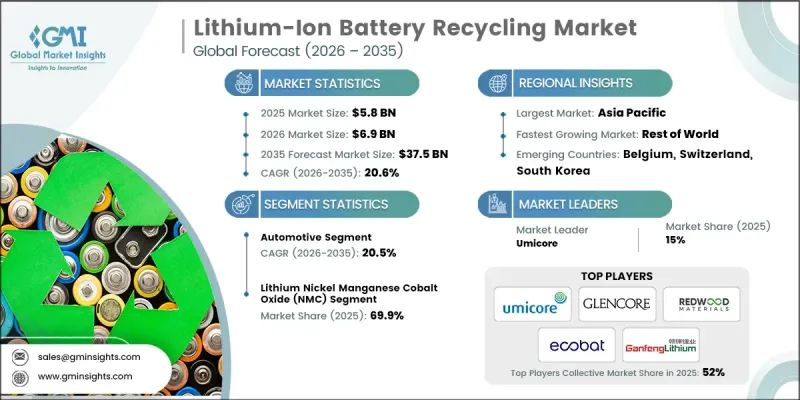

The Global Lithium-Ion Battery Recycling Market was valued at USD 5.8 billion in 2025 and is estimated to grow at a CAGR of 20.6% to reach USD 37.5 billion by 2035.

The industry has rapidly shifted from a specialized environmental service to a central part of the clean energy supply chain worldwide. Over the past few years, hydrometallurgical processes have become the preferred option due to their ability to recover high-value metals such as lithium, cobalt, and nickel with far greater precision than conventional smelting. This transition is further supported by updated regulatory frameworks, including new global rules that reward recyclers achieving high metal recovery efficiencies, encouraging wider adoption of water-based refining technologies. The industry is also experiencing strong momentum in the production and trade of black mass, which serves as an intermediate material for further metal extraction. Smaller recyclers are increasingly participating in this segment by supplying black mass to larger hydrometallurgical refiners. With the growing volume of battery waste generated from electric mobility, energy storage projects, and manufacturing scrap, the market is positioned for accelerated expansion throughout the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.8 Billion |

| Forecast Value | $37.5 Billion |

| CAGR | 20.6% |

The non-automotive segment is projected to grow at a CAGR of 20.9% by 2035. Increasing deployment of energy storage systems (ESS) for grid stabilization, commercial backup power, and integration of renewable energy sources is driving strong demand for batteries, particularly lithium iron phosphate (LFP) chemistries, due to their long cycle life and enhanced safety. As older ESS units reach the end of their operational lifespan, the need for recycling rises to recover valuable materials and free capacity for next-generation technologies, further fueling market growth.

The lithium nickel manganese cobalt oxide (NMC) segment held a 69.9% share in 2025 and is expected to grow at a CAGR of 21% from 2026 to 2035. Strengthening government regulations and policies focused on battery disposal and critical material reuse are supporting the growth of the battery recycling sector. NMC batteries are highly compatible with both pyrometallurgical and hydrometallurgical recycling processes, which are already commercially mature, enabling efficient recovery of metals such as nickel, cobalt, and manganese. Additionally, growing preference for chemistries offering high energy density, long operational life, and stable thermal performance-key requirements for EVs and stationary storage applications is reinforcing the prominence of NMC batteries.

U.S. Lithium-Ion Battery Recycling Market held 86.5% share in 2025 and is expected to generate USD 5.4 billion by 2035. Federal initiatives, including Department of Energy (DOE) grants, tax incentives, and investments under the Bipartisan Infrastructure Law, are accelerating domestic recycling capacities. These programs aim to reduce reliance on imported critical minerals, improve supply chain resilience, and support circular economy objectives, encouraging large-scale recycling projects. The rapid increase in EV adoption is also producing a growing volume of spent lithium-ion batteries, intensifying demand for robust recycling infrastructure.

Major companies active in the Global Lithium-Ion Battery Recycling Market include Redwood Materials, Ganfeng Lithium, Umicore, Glencore, and Attero Recycling. Companies in the Lithium-Ion Battery Recycling Market are implementing multiple strategies to strengthen their presence and expand their competitive advantage. Many are investing heavily in hydrometallurgical capacity to improve recovery rates and reduce environmental impact, while also modernizing facilities with automation and advanced separation technologies. Firms are forging long-term supply agreements with EV manufacturers and battery producers to secure consistent waste streams. Strategic collaborations with government agencies help unlock funding and regulatory support for large-scale recycling initiatives.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Chemistry trends

- 2.4 Process trends

- 2.5 Source trends

- 2.6 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Manufacturing capacity assessment

- 3.1.3 Supply chain resilience & risk factors

- 3.1.4 Distribution network analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Cost structure analysis

- 3.8 Price trend analysis (USD/Tons)

- 3.8.1 By chemistry

- 3.9 Technology trends & disruptions

- 3.9.1 Alkaline vs. rechargeable cannibalization

- 3.9.2 Lithium-ion chemistry evolution

- 3.9.3 Fast-charging & high-drain battery innovations

- 3.9.4 Emerging chemistries outlook

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive landscape, 2026

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2025

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Rest of world

- 4.3 Competitive benchmarking

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Chemistry, 2022 - 2035 (USD Billion & Thousand Tons)

- 5.1 Key trends

- 5.2 Lithium nickel manganese cobalt oxide (NMC)

- 5.3 Lithium iron phosphate (LFP)

- 5.4 Lithium cobalt oxide (LCO)

- 5.5 Others

Chapter 6 Market Size and Forecast, By Process, 2022 - 2035 (USD Billion & Thousand Tons)

- 6.1 Key trends

- 6.2 Pyrometallurgical

- 6.3 Hydrometallurgical

- 6.4 Physical/mechanical

Chapter 7 Market Size and Forecast, By Source, 2022 - 2035 (USD Billion & Thousand Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Non-automotive

Chapter 8 Market Size and Forecast, By Region, 2022 - 2035 (USD Billion & Thousand Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 France

- 8.3.3 Belgium

- 8.3.4 Switzerland

- 8.3.5 Germany

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 South Korea

- 8.4.3 Japan

- 8.5 Rest of World

Chapter 9 Company Profiles

- 9.1 3R Recycler

- 9.2 Accurec Recycling

- 9.3 ACE Green Recycling

- 9.4 American Battery Technology Company

- 9.5 Attero Recycling

- 9.6 Altilium Metals

- 9.7 BatX Energies

- 9.8 Cylib

- 9.9 Cirba Solutions

- 9.10 Ecobat

- 9.11 Eramet

- 9.12 Glencore

- 9.13 Ganfeng Lithium

- 9.14 Lohum Cleantech

- 9.15 Neometals

- 9.16 Recyclus Group

- 9.17 RecycLiCo Battery Material

- 9.18 Redwood Materials

- 9.19 SK TES

- 9.20 Umicore