PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982364

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982364

Hypercharger Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

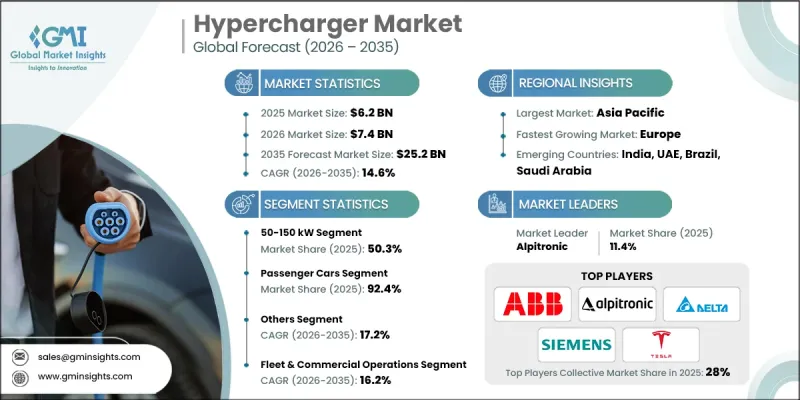

The Global Hypercharger Market was valued at USD 6.2 billion in 2025 and is estimated to grow at a CAGR of 14.6% to reach USD 25.2 billion by 2035.

Accelerating sustainability initiatives and zero-emission transportation targets worldwide are significantly increasing electric vehicle adoption, which in turn is driving demand for high-power charging infrastructure. As automotive manufacturers continue shifting their portfolios toward electrified models, the need for faster and more efficient charging solutions has become increasingly critical. Charging network operators are prioritizing ultra-fast technologies that reduce charging times and improve overall convenience, thereby addressing one of the primary barriers to EV adoption. Infrastructure expansion across developed and emerging markets is strengthening public confidence in long-distance electric mobility. Governments are playing a central role by supporting deployment through policy frameworks, funding programs, and emission-reduction mandates. Investments across North America, Europe, and Asia are accelerating the installation of high-capacity charging corridors and urban hubs, ensuring broader accessibility to advanced charging systems. These coordinated efforts between public authorities and private industry participants are positioning hyperchargers as essential components of the evolving global electric mobility ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.2 Billion |

| Forecast Value | $25.2 Billion |

| CAGR | 14.6% |

High-power DC charging systems significantly reduce vehicle downtime compared to conventional alternatives. Certain EV platforms can replenish battery capacity to 80% within approximately 15 to 30 minutes when connected to 350 kW chargers. By contrast, lower-tier charging solutions require substantially longer durations to achieve similar levels. Industry leaders such as ABB, Tesla, and IONITY have introduced advanced fast-charging technologies designed to support both urban commuting and extended highway travel. Public-sector backing continues to accelerate infrastructure deployment through coordinated funding mechanisms and regulatory support focused on high-capacity charging networks.

The 50-150 kW segment held 50.3% share, generating USD 3.1 billion in 2025. This power range remains widely adopted due to its broad vehicle compatibility and comparatively lower installation costs than ultra-high-capacity systems. Chargers within this category typically deliver a meaningful driving range within a single hour, making them well-suited for locations where vehicles remain parked for moderate durations. Their cost-performance balance has solidified their role as a foundational tier within the overall hypercharger landscape.

The passenger vehicles segment accounted for 92.4% share in 2025 and is expected to reach USD 22.6 billion by 2035. This dominance reflects the reality that private vehicles represent the majority of charging sessions and revenue generation. While a substantial portion of charging activity occurs in residential and workplace environments, public fast-charging networks are essential for long-distance travel and for drivers without access to private charging infrastructure. Corridor-based infrastructure planning and urban charging hubs continue to expand to meet rising demand.

U.S. Hypercharger Market reached USD 987.9 million in 2025, supported by comprehensive federal and state-level initiatives aimed at improving charging accessibility and reducing transportation emissions. Government-backed infrastructure programs are funding the expansion of high-power charging stations along strategic transportation routes to facilitate nationwide connectivity. These efforts prioritize interoperability, standardized deployment, and widespread access to fast-charging solutions, helping to alleviate range anxiety and encourage broader EV adoption.

Major companies operating in the Global Hypercharger Market include Siemens, Schneider Electric, Delta Electronics, Alpitronic, Eaton, EVgo Services, Tritium, and Kempower. These companies compete through technological innovation, network expansion, and strategic collaborations with automakers and infrastructure developers. Companies in the Hypercharger Market are strengthening their competitive position by investing in next-generation high-power charging systems, expanding modular and scalable infrastructure solutions, and forming partnerships with automotive OEMs and utility providers. Many firms are focusing on improving charger uptime, enhancing software integration, and enabling smart-grid compatibility to optimize energy management. Geographic expansion into high-growth EV markets, combined with participation in government-funded infrastructure programs, is accelerating deployment. Businesses are also prioritizing interoperability standards and user-friendly digital platforms to improve customer experience.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Power Output

- 2.2.3 Vehicle

- 2.2.4 Connector

- 2.2.5 Application

- 2.2.6 Charging Location

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Accelerating global electric vehicle (EV) adoption

- 3.2.1.2 Growing demand for reduced charging time and high-power infrastructure

- 3.2.1.3 Government incentives and national EV infrastructure programs

- 3.2.1.4 Expansion of highway and corridor-based fast charging networks

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Grid capacity constraints and power distribution limitations

- 3.2.2.2 High capital expenditure for installation and grid upgrades

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with renewable energy and energy storage systems

- 3.2.3.2 Expansion in emerging EV markets

- 3.2.3.3 Public-private partnerships for infrastructure expansion

- 3.2.3.4 Increasing electrification of commercial and fleet vehicles

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 SAE J3400

- 3.4.1.2 J1772

- 3.4.1.3 NEVI Program Requirements

- 3.4.2 Europe

- 3.4.2.1 EU TEN-T Regulations

- 3.4.2.2 CCS Mandates

- 3.4.3 Asia Pacific

- 3.4.3.1 CHAdeMO 3.0

- 3.4.3.2 GB/T

- 3.4.3.3 Regional Incentives

- 3.4.4 Latin America

- 3.4.4.1 Brazil ANEEL EV Charging Regulatory Framework

- 3.4.4.2 Mexico EVSE Deployment Initiatives

- 3.4.5 Middle East & Africa

- 3.4.5.1 UAE National Electric Vehicle Policy

- 3.4.5.2 Dubai/Abu Dhabi EV Charging Network Regulations

- 3.4.1 North America

- 3.5 Investment & Funding Analysis

- 3.5.1 Public infrastructure investments (NEVI, EU Funding Programs)

- 3.5.2 Private equity & venture capital trends

- 3.5.3 OEM & energy company strategic investments

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 High Power DC Charging (350 kW+ Deployments)

- 3.8.1.2 Modular Power Architecture

- 3.8.1.3 Liquid-Cooled Charging Cables

- 3.8.1.4 Dynamic Load Management

- 3.8.2 Emerging technologies

- 3.8.2.1 Megawatt-Class Charging (MCS for Heavy Duty)

- 3.8.2.2 Vehicle-to-Grid (V2G) Integration

- 3.8.2.3 AI-Enabled Charging Optimization

- 3.8.2.4 Renewable-Integrated Charging Sites

- 3.8.1 Current technological trends

- 3.9 Pricing analysis (Driven by Primary Research)

- 3.9.1 Historical price trend analysis

- 3.9.2 Pricing strategy by player type (Premium / Value / Cost-plus)

- 3.10 Trade data analysis (Driven by Primary Research)

- 3.10.1 Import/export volume & value trends

- 3.10.2 Key trade corridors & tariff impact

- 3.11 Patent landscape (Driven by Primary Research)

- 3.12 Sustainability and environmental impact

- 3.12.1 Environmental impact assessment

- 3.12.2 Social impact & community benefits

- 3.12.3 Governance & corporate responsibility

- 3.12.4 Sustainable finance & investment trends

- 3.13 Impact of AI on the hypercharger market

- 3.13.1 AI-driven disruption of existing business models

- 3.13.2 GenAI use cases & adoption roadmap by segment

- 3.13.3 Risks, limitations & regulatory considerations

- 3.14 Integration of Renewable Energy

- 3.14.1 On site solar photovoltaic (PV) coupled with hyperchargers

- 3.14.2 Energy storage systems (ESS) with charging infrastructure

- 3.14.3 Microgrid architectures for remote charging hubs

- 3.14.4 Vehicle-to-grid (V2G) with renewable integration

- 3.14.5 Shared solar charging hubs for multi-use sites

- 3.15 Rapid expansion of ultra-fast charging networks

- 3.15.1 Highway corridor deployment strategies

- 3.15.2 Commercial and fleet-oriented ultra-fast hubs

- 3.15.3 Public-private partnerships (PPPs) and investment models

- 3.15.4 Technological standardization and interoperability

- 3.16 Case studies

- 3.17 Future outlook & opportunities

- 3.18 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.18.1 Base Case - key macro & industry variables driving CAGR

- 3.18.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.18.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Power Output, 2022 - 2035 ($Mn, Thousand Units)

- 5.1 Key trends

- 5.2 50-150 kW

- 5.3 150-350 kW

- 5.4 Above 350kW

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Thousand Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 LCV

- 6.3.2 MCV

- 6.3.3 HCV

Chapter 7 Market Estimates & Forecast, By Connector, 2022 - 2035 ($Mn, Thousand Units)

- 7.1 Key trends

- 7.2 CCS (Combined Charging System)

- 7.3 CHAdeMO

- 7.4 GB/T

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn, Thousand Units)

- 8.1 Key trends

- 8.2 Public charging hubs

- 8.2.1 Highway corridors

- 8.2.2 Urban charging plazas

- 8.3 Fleet & commercial operations

- 8.4 Retail & convenience

- 8.4.1 Shopping centers & outlets

- 8.4.2 Service stations

Chapter 9 Market Estimates & Forecast, By Charging Location, 2022 - 2035 ($Mn, Thousand Units)

- 9.1 Key trends

- 9.2 Urban

- 9.3 Sub-Urban / highway corridors

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Russia

- 10.3.8 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.4.10 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 ABB

- 11.1.2 Tesla

- 11.1.3 Siemens

- 11.1.4 ChargePoint

- 11.1.5 Tritium

- 11.1.6 Schneider Electric

- 11.1.7 Eaton

- 11.1.8 Blink Charging

- 11.1.9 Delta Electronics

- 11.1.10 Kempower

- 11.2 Regional players

- 11.2.1 EVgo Services

- 11.2.2 Electrify America

- 11.2.3 Alpitronic

- 11.2.4 StarCharge

- 11.2.5 Enel X Way

- 11.2.6 EVBox

- 11.3 Emerging players

- 11.3.1 Wallbox

- 11.3.2 ADS-TEC Energy

- 11.3.3 Compleo Charging

- 11.3.4 Allego