PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982376

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982376

Thermal Imaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

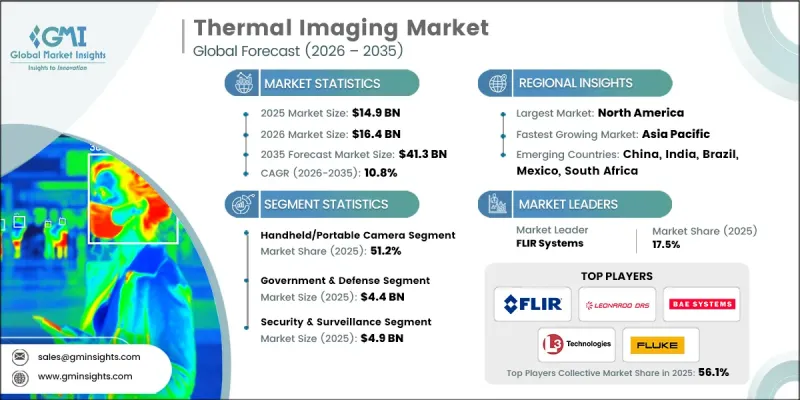

The Global Thermal Imaging Market was valued at USD 14.9 billion in 2025 and is estimated to grow at a CAGR of 10.8% to reach USD 41.3 billion by 2035.

Thermal imaging technology works by detecting infrared radiation emitted by objects and converting these heat signatures into visible images using specialized cameras. The system can operate without visible light, making it ideal for defense operations, border security, industrial inspections, and medical diagnostics in total darkness, fog, or smoke. The rising adoption of these systems across defense and industrial sectors, driven by modernization programs and increasing security demands, is fueling market expansion. Continuous technological advancements, government funding for public safety, and growing industrial automation are further accelerating the deployment of thermal imaging solutions. The market benefits from its applications in threat detection, surveillance, emergency response, and operational efficiency across diverse sectors.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $14.9 Billion |

| Forecast Value | $41.3 Billion |

| CAGR | 10.8% |

The handheld and portable thermal cameras segment held a 51.2% share in 2025. Their portability and ease of deployment make them essential for electrical inspections, HVAC maintenance, firefighting, and rapid emergency response. Modern uncooled sensors offer 640x512 resolution with 20mK sensitivity in compact packages under 500g, enabling quick, non-contact detection of hotspots in industrial, public safety, and building assessments.

The government and defense segment generated USD 4.4 billion in 2025, fueled by rising defense budgets, UAV and drone integrations requiring compact infrared systems, and border security initiatives. Advanced cooled MWIR and LWIR systems enable long-range targeting through darkness and adverse weather, while AI-based analytics support autonomous threat identification. Manufacturers focus on developing ruggedized, compact cores with AI edge analytics optimized for aerial platforms and tactical deployment.

U.S. Thermal Imaging Market was valued at USD 3.8 billion in 2025, driven by defense modernization, public safety funding, and industrial automation adoption. Military applications emphasize cooled and mid-wave infrared technologies for precise targeting and surveillance. Civilian use extends to utility monitoring, automotive safety, and healthcare screening. Stable government funding and organized procurement processes support sustained market expansion, while domestic manufacturing provides advantages in system integration and supply chain continuity.

Leading players in the Global Thermal Imaging Market include Raytheon, Seek Thermal, ULIS (Sofradir subsidiary), Draeger Safety Inc., Thermoteknix Systems, Palmer Wahl Instrumentation Group, 3M Scott, American Technologies Network (ATN) Corp., Bae Systems Imaging Solutions, Opgal Optronic Industries Limited, FLIR Systems, L3 Technologies, Axis Communications, Xenics NV, Tonbo Imaging, Leonardo DRS, Magnity Electronics, COX, Fluke Corporation (Fortive subsidiary), General Starlight Company Inc. (GSCI), Dali Technology, Avon Protection Systems Inc., and Wuhan Guide Infrared Co., Ltd. Companies in the Global Thermal Imaging Market are adopting strategies to strengthen their market position and expand global presence. They are investing heavily in research and development to enhance sensitivity, image resolution, and AI-driven analytics. Strategic partnerships, mergers, and acquisitions help penetrate new regional markets and broaden product offerings. Many firms focus on developing portable and ruggedized solutions for defense and industrial applications while enhancing manufacturing capabilities to improve supply chain efficiency.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry snapshot

- 2.2 Key market trends

- 2.2.1 Product trends

- 2.2.2 Technology trends

- 2.2.3 Application trends

- 2.2.4 End-user industry trends

- 2.2.5 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Billion)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising Defense Modernization Programs

- 3.2.1.2 Border Security & Maritime Surveillance Expansion

- 3.2.1.3 Counter-Drone & UAV Threat Detection

- 3.2.1.4 Night Vision Integration in Autonomous Systems

- 3.2.1.5 Public Safety & First Responder Demand

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Cost of Cooled MWIR/LWIR Sensors

- 3.2.2.2 SWaP-C Constraints in Portable Applications

- 3.2.3 Market opportunities

- 3.2.3.1 AI-Enhanced Thermal Analytics Proliferation

- 3.2.3.2 Hyperspectral & Multi-Spectral Fusion

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2022-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price forecast (2026-2035)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.2 Market Concentration Analysis

- 4.2.1 By Region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Thermal Imaging Market Estimates & Forecast, By Product, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Handheld/Portable camera

- 5.3 Fixed/Mounted Core

- 5.4 Scopes & Vision Googles

Chapter 6 Thermal Imaging Market Estimates & Forecast, By Technology, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Cooled

- 6.3 Uncooled

Chapter 7 Market Estimates and Forecast, By Application , 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Detection & measurement

- 7.3 Monitoring & inspection

- 7.4 Personal vision systems

- 7.5 Search & rescue

- 7.6 Security & surveillance

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End-Use Industry, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Commercial

- 8.4 Government & Defense

- 8.5 Healthcare & Life Sciences

- 8.6 Industrial

- 8.7 Residential

- 8.8 Others

Chapter 9 Thermal Imaging Market Estimates & Forecast, By Region, 2022 - 2035 (USD Million)

- 9.1 Key trends, by region

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.3.7 Rest of Europe

- 9.4 Asia-Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia-Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 3M Scott

- 10.2 Allied Vision

- 10.3 American Technologies Network (ATN) Corp.

- 10.4 Avon Protection Systems Inc.

- 10.5 Axis Communications

- 10.6 Bae Systems Imaging Solutions

- 10.7 COX

- 10.8 Dali Technology

- 10.9 Draeger Safety Inc.

- 10.10 FLIR Systems

- 10.11 Fluke Corporation (Fortive subsidiary)

- 10.12 General Starlight Company Inc. (GSCI)

- 10.13 L3 Technologies

- 10.14 Leonardo DRS

- 10.15 Magnity Electronics

- 10.16 Opgal Optronic Industries Limited

- 10.17 Palmer Wahl Instrumentation Group

- 10.18 Raytheon

- 10.19 Seek Thermal

- 10.20 Testo SE

- 10.21 Thermoteknix Systems

- 10.22 Tonbo Imaging

- 10.23 ULIS (Sofradir subsidiary)

- 10.24 Wuhan Guide Infrared Co., Ltd.

- 10.25 Xenics NV