PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982385

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1982385

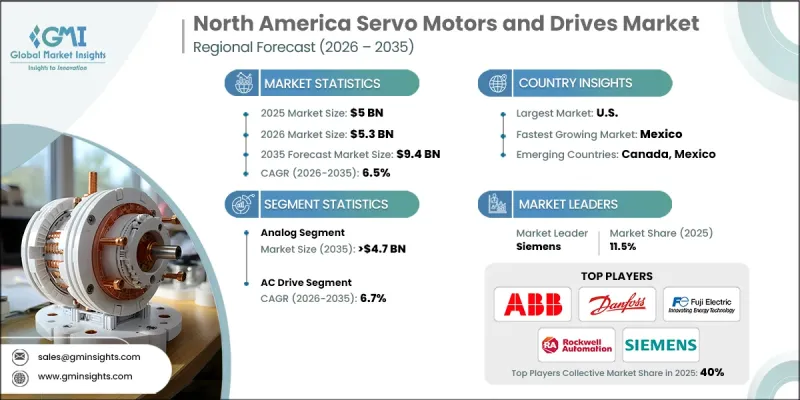

North America Servo Motors and Drives Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

North America Servo Motors and Drives Market was valued at USD 5 billion in 2025 and is estimated to grow at CAGR of 6.5% to reach USD 9.4 billion by 2035.

Growth across the North America servo motors and drives market is fueled by the accelerating shift toward energy-efficient motion control systems in industrial environments. Manufacturers are increasingly integrating advanced servo technologies to enhance productivity, minimize downtime, and improve overall operational accuracy. Continuous investment in modern manufacturing facilities and processing infrastructure is further strengthening product demand across the region. The rapid expansion of robotics, automated material handling systems, and precision-driven production lines is reinforcing the need for reliable servo motors and drives capable of delivering consistent torque and precise speed control under varying load conditions. Rising capital expenditure across energy-intensive industries is also creating new deployment opportunities. As companies focus on improving production efficiency, reducing turnaround time, and maintaining high-quality standards, the adoption of advanced automation platforms continues to rise. Ongoing innovation in servo system architecture, including enhanced position control and optimized torque management, is reshaping the competitive landscape and supporting sustained regional growth.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5 Billion |

| Forecast Value | $9.4 Billion |

| CAGR | 6.5% |

Industrial enterprises are prioritizing production optimization strategies that emphasize automation, digitalization, and improved process consistency. The North America servo motors and drives industry is evolving in response to rapid technological advancements and increased demand for energy-efficient automation solutions. Continuous improvements in servo performance capabilities are enabling finer control over motion parameters, strengthening their role in high-precision industrial applications.

Based on category, the analog segment is anticipated to reach USD 4.7 billion by 2035. Demand for analog servo motors and drives remains strong due to their straightforward configuration, seamless system compatibility, and reliable performance in a wide range of industrial settings. Expanding manufacturing operations, higher investment in automation technologies, and growing emphasis on energy optimization are contributing to new growth avenues within this segment.

The AC drive segment is expected to witness a CAGR of 6.7% through 2035. AC servo systems are gaining traction because of their ability to manage high current loads, deliver elevated torque output, support faster operating speeds, and maintain lower noise levels. Advancements in motor engineering and supportive regulatory initiatives aimed at improving industrial efficiency are further accelerating adoption. Increasing demand for high-performance automation systems across multiple industries continues to reinforce growth within this segment.

U.S. Servo Motors and Drives Market reached USD 3.7 billion in 2025, accounting for 74% share. Market expansion in the United States is supported by widespread implementation of smart manufacturing practices, rapid automation deployment, and strong focus on sustainability initiatives. Rising consumer demand across key production sectors and efforts to enhance domestic manufacturing output are further driving product adoption nationwide.

Key companies operating in the North America Servo Motors and Drives Market include Rockwell Automation, Siemens, ABB, Mitsubishi Electric, Yaskawa Electric, Schneider Electric, Bosch Rexroth, Nidec, Panasonic, Hitachi, Delta Electronics, Fuji Electric, Kollmorgen, Danfoss, Festo, KEB Automation, Allied Motion, Advanced Motion Controls, Allient, Baumuller, Ingenia Cat, and E-Circuit Motors. Companies in the North America Servo Motors and Drives Market are reinforcing their competitive standing through innovation, strategic collaborations, and portfolio expansion. Industry leaders are investing heavily in research and development to enhance precision control, improve energy efficiency, and integrate smart diagnostics into servo platforms. Partnerships with robotics manufacturers and system integrators are strengthening ecosystem integration and expanding application reach. Many firms are focusing on modular and scalable product architectures to address diverse industrial requirements. Geographic expansion, localized manufacturing, and enhanced after-sales support services are further improving customer engagement. Additionally, companies are leveraging digital technologies, including predictive maintenance and IoT-enabled monitoring, to deliver value-added solutions and secure long-term customer relationships in an increasingly competitive automation landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Quality commitment

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.1.1 Sources, by country

- 1.5.1 Paid Sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

- 1.9 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.2 Business trends

- 2.3 Category trends

- 2.4 Drive trends

- 2.5 Application trends

- 2.6 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability & sourcing analysis

- 3.1.2 Key factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Price trend analysis (USD/Unit)

- 3.7.1 By drive

- 3.7.2 By country

- 3.8 Emerging opportunities & trends

- 3.8.1 Digital transformation with IoT technologies

- 3.8.2 Emerging market penetration

- 3.9 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, by country, 2025

- 4.2.1 U.S.

- 4.2.2 Canada

- 4.2.3 Mexico

- 4.3 Competitive positioning matrix

- 4.4 Key developments

- 4.4.1 Mergers & acquisitions

- 4.4.2 Partnerships & collaborations

- 4.4.3 New product launches

- 4.4.4 Expansion plans and funding

Chapter 5 Market Size and Forecast, By Category, 2022 - 2035 (USD Million, '000 Units)

- 5.1 Key trends

- 5.2 Digital

- 5.3 Analog

Chapter 6 Market Size and Forecast, By Drive, 2022 - 2035 (USD Million, '000 Units)

- 6.1 Key trends

- 6.2 AC Drive

- 6.3 DC Drive

Chapter 7 Market Size and Forecast, By Application, 2022 - 2035 (USD Million, '000 Units)

- 7.1 Key trends

- 7.2 Oil & gas

- 7.3 Metal cutting & forming

- 7.4 Material handling equipment

- 7.5 Packaging and labeling machinery

- 7.6 Robotics

- 7.7 Medical robotics

- 7.8 Rubber & plastics machinery

- 7.9 Warehousing

- 7.10 Automation

- 7.11 Extreme environment applications

- 7.12 Semiconductor machinery

- 7.13 AGV

- 7.14 Electronics

- 7.15 Others

Chapter 8 Market Size and Forecast, By Country, 2022 - 2035 (USD Million, '000 Units)

- 8.1 Key trends

- 8.2 U.S.

- 8.3 Canada

- 8.4 Mexico

Chapter 9 Company Profiles

- 9.1 ABB

- 9.2 Advanced Motion Controls

- 9.3 Allied Motion

- 9.4 Allient

- 9.5 Baumuller

- 9.6 Bosch Rexroth

- 9.7 Danfoss

- 9.8 Delta Electronics

- 9.9 E-Circuit Motors

- 9.10 Festo

- 9.11 Fuji Electric

- 9.12 Hitachi

- 9.13 Ingenia Cat

- 9.14 KEB Automation

- 9.15 Kollmorgen

- 9.16 Mitsubishi Electric

- 9.17 Nidec

- 9.18 Panasonic

- 9.19 Rockwell Automation

- 9.20 Schneider Electric

- 9.21 Siemens

- 9.22 Yaskawa Electric