PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998662

PUBLISHER: Global Market Insights Inc. | PRODUCT CODE: 1998662

Connected Vehicle and V2X Digital Twin Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

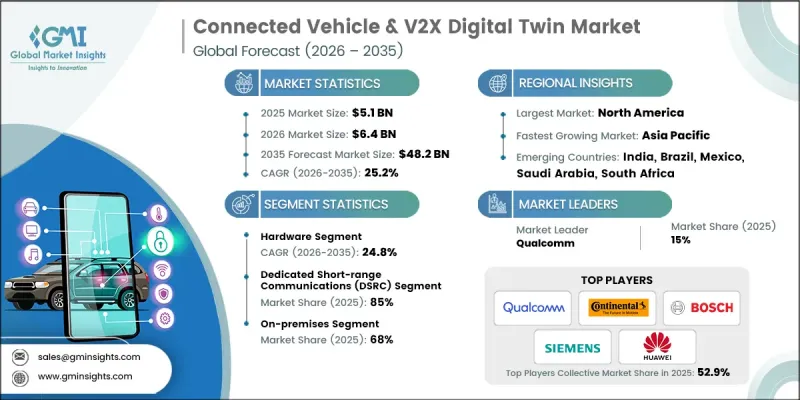

The Global Connected Vehicle & V2X Digital Twin Market was valued at USD 5.1 billion in 2025 and is estimated to grow at a CAGR of 25.2% to reach USD 48.2 billion by 2035.

The rapid expansion reflects the growing reliance on advanced digital simulation platforms capable of replicating real-time behavior, communication patterns, and network responses of connected and autonomous vehicles. As transportation ecosystems become increasingly data-driven, digital twin technology is emerging as a foundational tool for testing vehicle interactions across diverse traffic conditions and infrastructure environments. Automakers and technology developers are prioritizing real-time virtual modeling to improve operational efficiency, safety validation, and cooperative mobility frameworks. The convergence of Vehicle-to-Everything (V2X) communication, Cellular V2X (C-V2X), and next-generation wireless connectivity accelerate deployment across urban mobility networks. Low-latency processing powered by edge computing and AI-driven analytics enables predictive insights, helping stakeholders enhance vehicle performance and system-wide safety. Additionally, tightening global safety and emissions regulations are compelling Original Equipment Manufacturers (OEMs) to deploy digital twin simulations to validate compliance scenarios before commercial vehicle production. As intelligent transportation systems evolve, the connected vehicle & V2X digital twin market is positioned as a critical enabler of scalable, data-centric mobility infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $5.1 Billion |

| Forecast Value | $48.2 Billion |

| CAGR | 25.2% |

The hardware segment held a 61% share in 2025 and is projected to register a CAGR of 24.8% from 2026 through 2035. Advanced components such as edge-optimized sensors, integrated 5G and C-V2X communication modules, and high-accuracy Global Navigation Satellite System (GNSS) devices collectively deliver continuous data streams that power digital twin environments. Edge computing frameworks reduce latency and enhance automated driving safety by enabling dynamic modeling between vehicles and surrounding infrastructure. AI-enabled digital twin platforms further strengthen predictive analytics, real-time simulation accuracy, and multi-vehicle coordination. Cloud-native architectures and microservices-based ecosystems support scalable integration with over-the-air (OTA) software updates and cross-platform interoperability, improving fleet performance modeling, operational decision-making, and safety management.

The Dedicated Short-Range Communications (DSRC) segment accounted for 85% share in 2025 and is anticipated to grow at a CAGR of 25.5% from 2026 to 2035. DSRC technology supports rapid data exchange between vehicles and roadside systems within defined geographic zones, enhancing situational awareness and road safety. Operating within reserved Intelligent Transportation Systems (ITS) spectrum bands, DSRC ensures dependable localized connectivity, supplying digital twin models with consistent real-world traffic inputs. This capability strengthens the accuracy of safety simulations, congestion forecasting, and urban traffic optimization within densely populated regions.

North America Connected Vehicle & V2X Digital Twin Market generated USD 2.1 billion in 2025 and continues to hold a leading position globally. Regional dominance is supported by early adoption of V2X frameworks, sustained research and development funding, and proactive deployment of intelligent transportation infrastructure. Government-backed smart mobility initiatives and regulatory alignment further accelerate digital twin integration across metropolitan areas. These programs leverage connected vehicle ecosystems to improve traffic flow management, strengthen safety oversight, and monitor environmental performance metrics.

Key companies shaping the Global Connected Vehicle & V2X Digital Twin Market include Qualcomm, NXP Semiconductors, Robert Bosch, Intel, Huawei, Microsoft, NVIDIA, Siemens, Continental, and Samsung Electronics. Companies operating in the Connected Vehicle & V2X Digital Twin Market are strengthening their competitive positions through continuous technology innovation, ecosystem partnerships, and infrastructure expansion. Market participants are investing in AI-enhanced simulation platforms, edge-computing capabilities, and integrated 5G connectivity solutions to deliver low-latency, high-precision digital twin environments. Strategic collaborations with automotive OEMs, telecom providers, and smart city authorities enable seamless deployment of interoperable V2X systems. Firms are also prioritizing cloud-native architectures and modular software frameworks to support scalability and recurring revenue models through OTA updates and analytics services.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.3 GMI AI policy & data integrity commitment

- 1.4 Research trail & confidence scoring

- 1.4.1 Research trail components

- 1.4.2 Scoring components

- 1.5 Data collection

- 1.5.1 Partial list of primary sources

- 1.6 Data mining sources

- 1.6.1 Paid sources

- 1.7 Base estimates and calculations

- 1.7.1 Base year calculation

- 1.8 Forecast model

- 1.9 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 V2X communication type

- 2.2.4 Connected technology

- 2.2.5 Deployment mode

- 2.2.6 Vehicle

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth of connected & autonomous vehicles

- 3.2.1.2 Smart city & intelligent transport initiatives

- 3.2.1.3 AI/ML + 5G + edge computing integration

- 3.2.1.4 Regulatory pressure on safety & emissions

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Implementation & Infrastructure Costs

- 3.2.2.2 Data Security, Privacy & Interoperability Challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion in emerging regions & smart mobility projects

- 3.2.3.2 Integration with autonomous driving & fleet management

- 3.2.3.3 Sustainable & resilient urban mobility solutions

- 3.2.3.4 New Use Cases from Blockchain, Edge-AI & IoT Integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.2 Society of Automotive Engineers (SAE International)

- 3.4.2 Europe

- 3.4.2.1 European Commission - Directorate-General for Mobility & Transport (EC DG MOVE)

- 3.4.2.2 European Telecommunications Standards Institute (ETSI)

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (MIIT - China)

- 3.4.3.2 Japan Automotive Research Institute (JARI)

- 3.4.4 Latin America

- 3.4.4.1 National Land Transport Agency (ANTT - Brazil)

- 3.4.4.2 Secretariat of Communications and Transportation (SCT - Mexico)

- 3.4.5 Middle East & Africa

- 3.4.5.1 Roads and Transport Authority (RTA - UAE)

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO - Saudi Arabia)

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis (Driven by Primary Research)

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Impact of Artificial Intelligence (AI)

- 3.12.1 AI-Driven Disruption of Existing Business Models

- 3.12.2 GenAI Use Cases & Adoption Roadmap by Segment

- 3.12.3 Risks, Limitations & Regulatory Considerations

- 3.13 Standards, interoperability & certification framework

- 3.13.1 Global V2X standards landscape

- 3.13.2 Digital twin standards & protocols

- 3.13.3 Interoperability testing & validation

- 3.13.4 Certification & compliance programs

- 3.14 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.14.1 Base Case - key macro & industry variables driving CAGR

- 3.14.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.14.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Edge computing devices

- 5.2.2 Sensors & RSUs

- 5.2.3 On-board vehicle computing units

- 5.3 Software

- 5.3.1 Digital twin platforms

- 5.3.2 Simulation & modeling engines

- 5.3.3 Analytics & AI software

- 5.4 Services

- 5.4.1 Integration & deployment

- 5.4.2 Managed analytics services

- 5.4.3 Consulting & customization

Chapter 6 Market Estimates & Forecast, By V2X Communication type, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Vehicle-to-vehicle (V2V)

- 6.3 Vehicle-to-pedestrian (V2P)

- 6.4 Vehicle-to-network (V2N)

- 6.5 Vehicle-to-grid (V2G)

- 6.6 Vehicle-to-home (V2H)

Chapter 7 Market Estimates & Forecast, By Connected technology, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Dedicated short range communications (DSRC)

- 7.3 Cellular V2X (C-V2X)

Chapter 8 Market Estimates & Forecast, By Deployment mode, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 Cloud

- 8.3 On-Premises

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Passenger cars

- 9.2.1 Hatchback

- 9.2.2 SUV

- 9.2.3 Sedan

- 9.3 Commercial vehicles

- 9.3.1 LCV

- 9.3.2 MCV

- 9.3.3 HCV

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Poland

- 10.3.9 Romania

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global companies

- 11.1.1 Continental

- 11.1.2 Huawei

- 11.1.3 Intel

- 11.1.4 Microsoft

- 11.1.5 NVIDIA

- 11.1.6 NXP Semiconductors

- 11.1.7 Qualcomm

- 11.1.8 Robert Bosch

- 11.1.9 Samsung Electronics

- 11.1.10 Siemens

- 11.2 Regional players

- 11.2.1 Aptiv

- 11.2.2 Autotalks

- 11.2.3 Cohda Wireless

- 11.2.4 Denso

- 11.2.5 Kapsch TrafficCom

- 11.3 Emerging players

- 11.3.1 Altair Engineering

- 11.3.2 LG Electronics

- 11.3.3 PTC

- 11.3.4 Savari

- 11.3.5 Tata Consultancy Services